A buffer-account system that pays you a real salary, smooths $1,800 and $9,000 months into the same number, and stops the panic.

You know the feeling. One month every bill goes out on time and you’ve got money left over. Six weeks later you’re refreshing your bank balance and trying to guess which client will come through first. This is the cash flow problem. It hits most freelancers, and it has nothing to do with whether you’re good at your work.

Remote’s State of Freelance Work 2025 (also referred to as the Contractor Management Report 2025) found that 85% of freelancers have invoices paid late at least some of the time. Just over 21% are paid late, or not at all, more than half the time. They get paid on time less often than they get paid late. One in five. Read that again.

Nobody trains you for the cash flow side of self-employment. Most people don’t even think of freelancing as a business until the money stops working, and by the time they do, they’re already behind.

This guide covers the parts that actually matter. How to forecast 30 to 60 days ahead. How to pay yourself a stable monthly salary even when your income swings between $1,800 and $9,000. Which tools automate the work. And what actually shortens payment delays when clients drag their feet.

What It Costs When You Don’t Manage Cash Flow Properly

Start by looking at the actual cost.

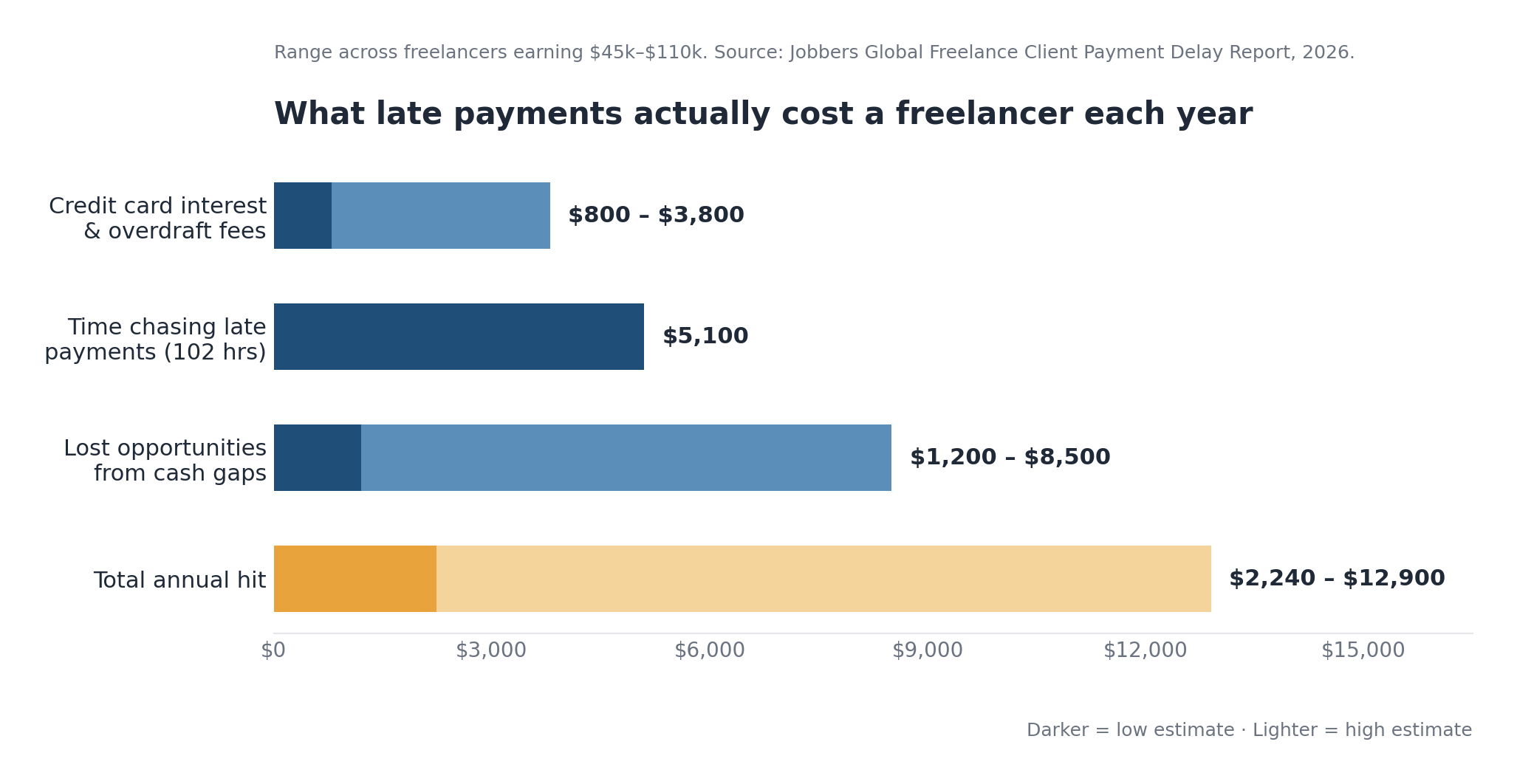

Jobbers’ Global Freelance Client Payment Delay Report (last updated January 2026) pulled together data from Freelancers Union surveys, Harvard Business School research, and Payoneer’s annual reports. The numbers are blunt. Credit card interest and overdraft fees from delayed payments run $800 to $3,800 a year, depending on income level. Chasing late payments swallows around 102 hours annually, worth $5,100 at $50 an hour. Lost opportunities from cash flow constraints add another $1,200 to $8,500. Total annual hit per freelancer: $2,240 to $12,900.

Money you already earned, gone to interest, late fees, and the projects you couldn’t take because you didn’t have the working capital to cover the gap.

A 2025 QuickBooks survey of more than 2,000 freelancers found 56% were owed money from unpaid invoices, averaging $17,500 per business. With no buffer, a $17,500 gap forces the decisions you’ve been trying to avoid. Taking the badly-paid project. Putting next month’s software bill on a credit card. Skipping your quarterly tax payment because the cash isn’t there.

Freelancers lose 8 to 12 hours a month chasing late payments. At $75 an hour, that’s $600 to $900 of unbilled time, every month.

Once your cash flow is under control, you can turn down a badly priced project because you’ve got three weeks of runway. You can spend $300 on a tool that saves five hours a month. You can see what’s coming before it lands.

Why Clients Pay Late (And Why It’s Systemic)

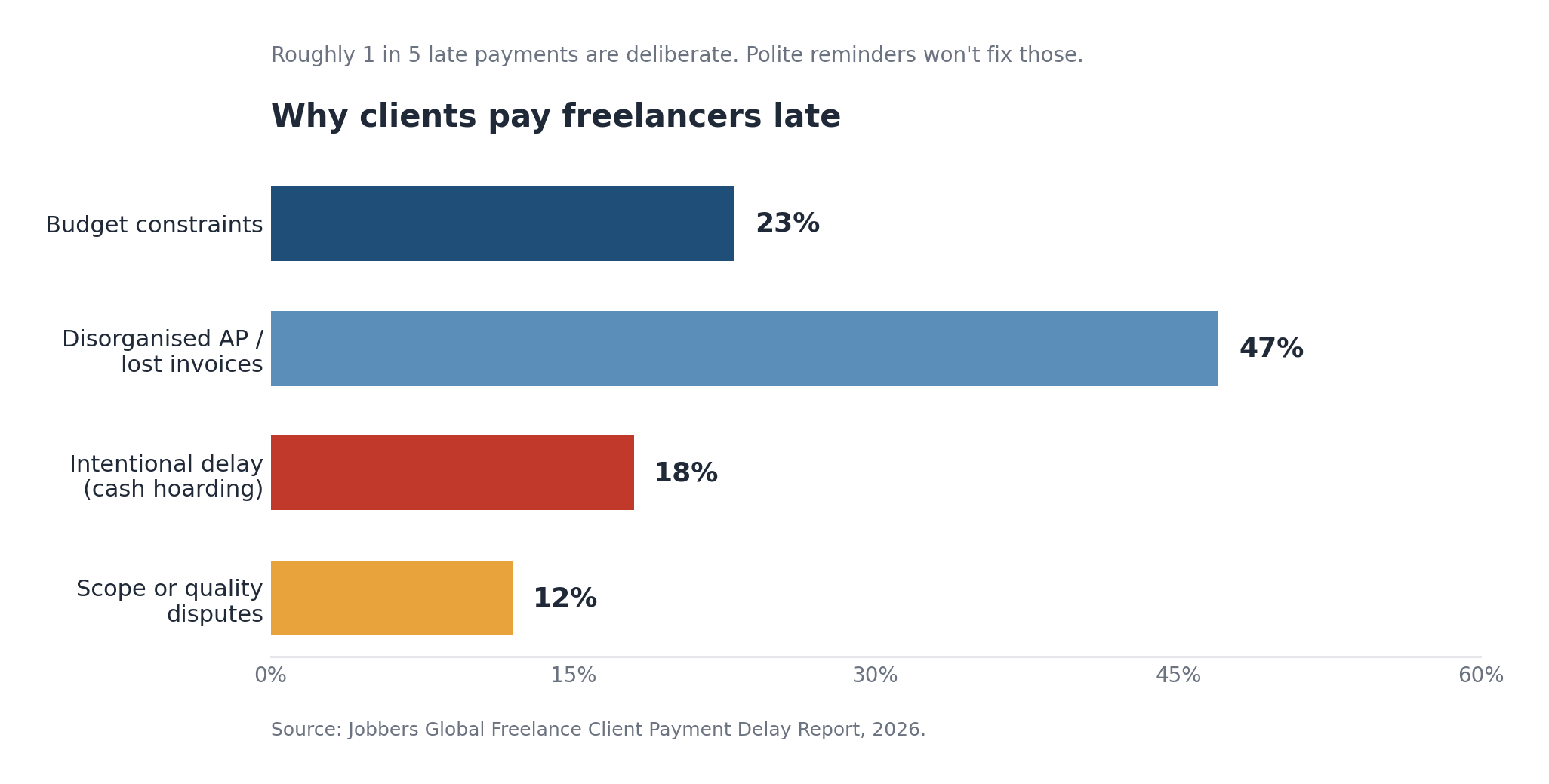

It’s tempting to assume a late-paying client is just disorganised. Sometimes that’s true. The data says it’s more often something else.

The Jobbers report breaks down the causes. Budget constraints account for 23% of delays. Intentional delay tactics, where clients deliberately postpone payment to preserve their own working capital, account for 18%. Poor accounts payable management adds an average of 9 days. Scope disputes cause 12%.

Small businesses and individual clients account for 70% of non-payment cases, usually citing budget constraints or dissatisfaction with deliverables.

This changes how you respond. If 18% of delays are deliberate, polite reminder emails will not fix them. The fix has to live in your contracts and your bank balance, not your tone. Clear payment terms. Deposits upfront. A cash reserve so a slow-paying client is annoying instead of catastrophic.

The legal landscape is moving, slowly. California’s Freelance Worker Protection Act, signed September 28, 2024 and effective January 1, 2025, requires written contracts for services valued at $250 or more, and payment within 30 days unless the contract specifies otherwise. New York’s Freelance Isn’t Free Act expanded statewide in August 2024, with a $800 threshold and the same 30-day default. The UK’s Prompt Payment Code requires large businesses to pay smaller suppliers within 30 days. The laws help, but enforcement is uneven and they offer little protection against clients who ignore the rules entirely.

Set things up so a single slow-paying client cannot wreck your month, regardless of what they decide to do.

How to Manage Cash Flow with a 30-to-60-Day Forecast

Most freelancers have a rough idea of what’s coming in. They know which invoices are out. What they don’t have is a written picture of their accounts receivable, set against what they owe and when. That’s the gap a forecast closes.

Step 1: Map Every Dollar Coming In

Write down every source of income expected in the next 60 days. Be specific about timing:

- Outstanding invoices already sent, with the expected payment date based on your actual terms, not your hope.

- Projects currently in progress, with a realistic completion and invoice date.

- Recurring clients on retainers, with the scheduled payment date.

- Any one-time projects still in negotiation, marked as probable rather than confirmed.

Be honest. If a client regularly pays 15 days late, don’t put them in the on-time column. If a project always runs long, build that in. Your forecast is only useful if it reflects reality.

Step 2: Map Every Dollar Going Out

List all your expenses for the same 60-day window:

- Fixed costs: software subscriptions, rent or co-working space, phone, internet, insurance.

- Variable costs: contractors, materials, stock images, tools you buy per project.

- Tax set-asides: 25 to 30% of every dollar earned. If you’re not doing this, your forecast will be misleading. That money isn’t really yours.

- Personal bills: mortgage or rent, utilities, groceries, loan payments, anything with a due date.

Step 3: Calculate Your Cash Position

Subtract total outgoing from total incoming. That number is your cash position for the period. Here’s a worked example for a freelance graphic designer with two active clients and one retainer:

| Item | Amount |

|---|---|

| Incoming | |

| Invoice sent 8 days ago (Net 30 client, pays on time) | $3,200 |

| Project finishing in 18 days (invoice on completion) | $2,500 |

| Monthly retainer client (paid on 1st of month) | $1,800 |

| New project in proposal stage (not confirmed) | $0 |

| Total Incoming | $7,500 |

| Outgoing | |

| Rent / co-working space | $800 |

| Adobe Creative Cloud + Figma + storage | $85 |

| Personal bills (mortgage, utilities, groceries) | $2,200 |

| Tax set-aside (28% of income) | $2,100 |

| Contractor (outsourced copywriting) | $400 |

| Total Outgoing | $5,585 |

| Net Cash Position | +$1,915 |

You’re positive in this scenario. Now watch what happens if that Net 30 client pays 15 days late. The $3,200 doesn’t arrive in time, your position swings to -$1,285 before the retainer lands, and that’s the gap that sends people to their credit card. Run the exercise weekly. Most accounting tools refresh it automatically once you’ve connected your bank account.

Some freelancers prefer a 13-week rolling forecast over a 60-day one. Same approach, longer horizon. The 13-week view is what finance teams use because it covers a full quarterly tax cycle plus typical Net 30 and Net 60 invoice timing in a single picture.

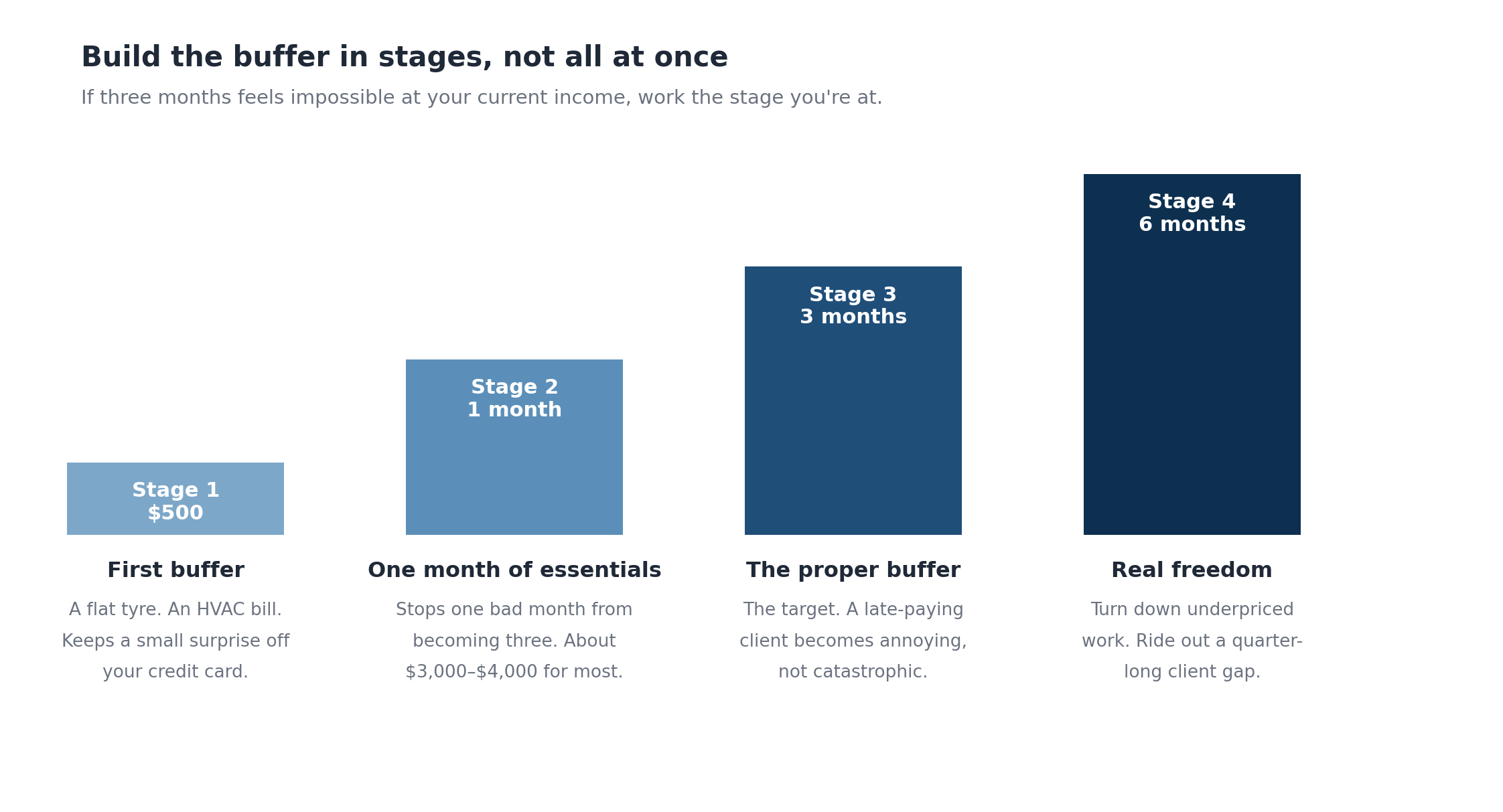

The 3-Month Buffer Target (and a Realistic Way to Get There)

Before you chase growth, build stability. The first financial goal is three months of fixed costs in a separate savings account. If your monthly fixed costs are $3,000, target $9,000. Once that’s in place, a client paying 30 days late costs you patience, not sleep.

If three months feels impossible at your current income, build it in stages:

- $500. Stops a small surprise (a flat tyre, an HVAC bill) from going on a credit card.

- One month of essentials. Stops one bad month from becoming three.

- Three months of fixed costs. The proper buffer. Most clients pay within this window.

- Six months of essentials. Lets you turn down bad-fit work and ride out a quarter-long client gap.

Work on the stage you’re at now. Skipping ahead doesn’t work.

Separate Your Money Before You Do Anything Else

This step gets skipped, and it causes more chaos than almost anything else on the list.

Roughly half of freelancers still pay business expenses out of a personal account. If that’s you, stop. Open a business checking account today. Every invoice payment lands in it. Every business expense comes out of it. Your personal account only receives a fixed transfer that you treat as your salary, paid on a regular schedule.

You get three things from this. Your cash position is obvious at a glance. Tax season becomes an afternoon of admin instead of a panic. And you stop treating every dollar in the account as spending money.

The tax angle alone justifies the five minutes it takes to open the account. When business and personal money mix, it’s easy to spend what you owe to the tax authority. A dedicated account for tax set-asides, with 25 to 30% of every payment moved there automatically, means you never accidentally spend money that was never yours.

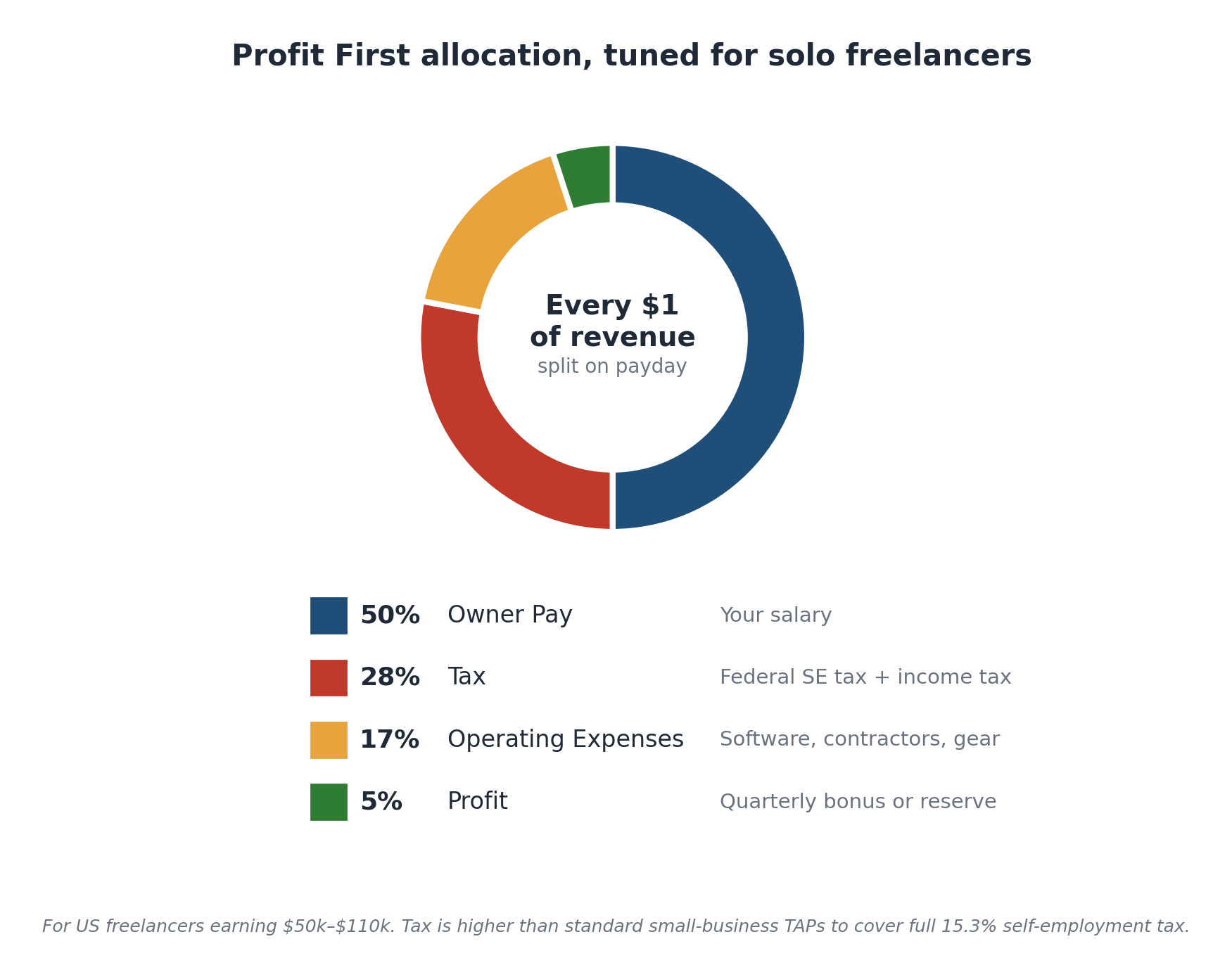

A Quick Profit First Allocation for Freelancers

Mike Michalowicz’s Profit First framework gets recommended a lot in solo-business circles. Instead of paying expenses first and hoping profit appears at the end, you allocate every payment to a fixed set of accounts the moment it arrives. The leftover at the end of the month is what you have to work with, not what you might have. The percentages are sometimes called Target Allocation Percentages, or TAPs.

For a US freelancer earning between $50,000 and $110,000, the starting TAPs look roughly like this:

- Owner Pay: 50%. The salary you transfer to your personal account.

- Tax: 25 to 30%. Federal self-employment tax plus federal and state income tax. Closer to 35% if you’re in a high-tax state.

- Operating Expenses: 15 to 20%. Software, contractors, equipment, anything the business actually consumes.

- Profit: 5%. Yes, profit. Treat it as a quarterly bonus to yourself or a long-term reserve.

These percentages are tilted from Michalowicz’s standard small-business numbers because solo freelancers carry the full 15.3% self-employment tax. A storefront business splitting payroll tax with employees would land closer to 50–60% OpEx and 30–50% owner pay.

You don’t need five separate bank accounts to run this. Two checking accounts and two savings accounts cover it: business operating, owner pay (your personal account), tax savings, and profit savings. Move the percentages on a fixed day each month, usually the 10th and 25th. The discipline is the point.

If 5% to profit feels impossible right now, start at 1%. The number matters less than building the habit of allocating before spending.

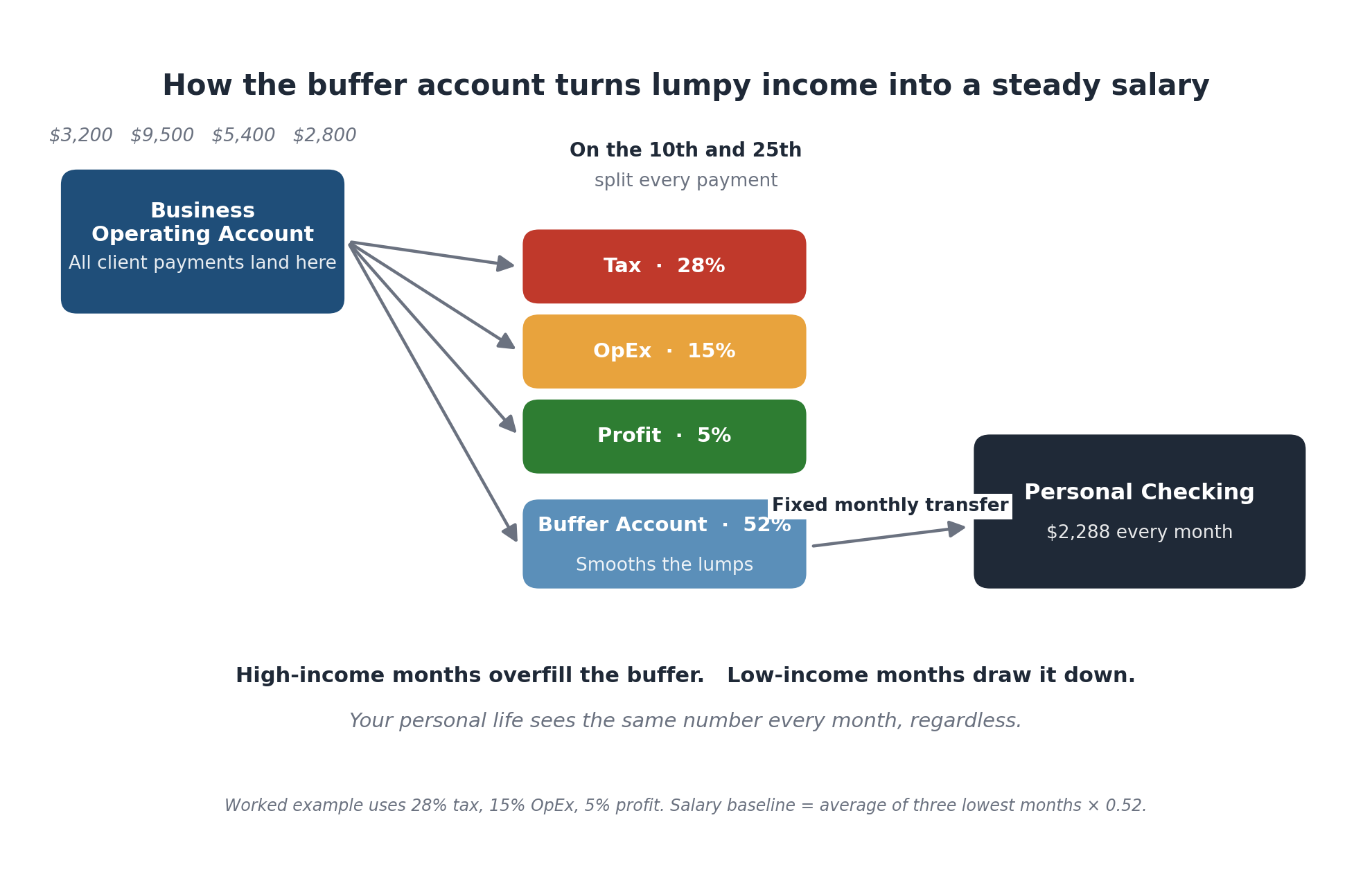

The Buffer-Account Trick: Pay Yourself a Real Salary

This is the biggest single change you can make for cash flow stress, and almost nobody teaches it.

The problem with allocating “owner pay” as a percentage of every payment is that your personal income still swings around. A $9,000 month and a $2,500 month produce different salaries even after you’ve taken your 50%. That’s the volatility most freelancers actually live with, and it’s what makes mortgage applications, rent budgets, and basic mental peace difficult.

The fix is a buffer account that sits between your business income and your personal salary. Here’s the flow:

- All business income lands in the business operating account.

- On the 10th and 25th of each month, you move tax (28%), OpEx (15%), and profit (5%) to their respective accounts.

- The remaining 52% goes to a buffer account, not directly to your personal account.

- From the buffer account, you transfer a fixed amount to your personal checking on the same date every month. That’s your salary.

High-income months overfill the buffer. Low-income months draw it down. Your personal life sees the same number every month regardless.

How to set the salary number: take your last six months of revenue, subtract the percentages you’d allocate to tax, OpEx, and profit, and use the average of your three lowest months as your monthly salary baseline. Conservative, but protective. You can revise it every quarter as the buffer grows.

Worked example. A freelance illustrator with revenue swinging between $3,200 and $9,500 over six months has an average of $6,200 and a low-three-month average of $4,400. After 28% tax, 15% OpEx, and 5% profit (48% total), the salary baseline is $4,400 × 0.52 = $2,288 per month. That’s the fixed transfer to her personal account. In a $9,500 month, the buffer absorbs the surplus. In a $3,200 month, the buffer covers the gap.

Within six to twelve months, the buffer typically holds two or three months of salary. That’s when the system genuinely starts working. You can take a vacation, go through a slow quarter, or turn down underpriced work without your personal cash flow noticing.

This is the closest a freelancer gets to a paycheck.

Tools That Handle the Tracking for You

A spreadsheet works. It gets the job done, especially when you’re starting out. The cost is time. According to Flexable’s 2025 Freelance Payment Report, AI-driven invoicing tools like FreshBooks cut payment delays by 40% for around 2 million freelancers worldwide, mostly through automated reminders. Automation directly speeds up how fast you get paid.

FreshBooks

Best for: Freelancers who bill by time or project and want the simplest possible setup.

FreshBooks is built for service providers who invoice clients, track time, and need a clear financial picture without a bookkeeping degree. The dashboard shows outstanding invoices, anything overdue, and your projected income over the next 30 days. Connect your bank account and expenses import automatically. Payment reminders fire without you touching them. The time tracker converts tracked hours straight into invoice line items, which catches the hours that would otherwise go unbilled.

The Lite plan starts at $19 a month and caps you at five billable clients. The Plus plan, around $38 to $43 a month depending on promotional pricing, removes that cap and suits most freelancers. Customer satisfaction scores sit consistently near the top of the category.

One catch worth flagging: adding your accountant as a user costs extra on most plans.

Xero

Best for: Freelancers who work with a bookkeeper, have multiple income streams, or want professional-grade reporting.

Xero connects to more than 1,000 third-party apps and gives unlimited users on every plan, which means your accountant logs in without an extra fee. The cash flow reporting beats FreshBooks. You get a proper cash flow statement alongside profit and loss, and once you connect your bank, reconciliation is largely automatic.

The Starter plan (formerly Early) starts at $20 a month, but most freelancers need the $47 a month Standard plan (formerly Growing), because Starter caps you at 20 invoices and 5 bills per month. Xero renamed these plans in April 2026, though pricing carried over. The learning curve is steeper than FreshBooks, so budget a few hours to get oriented if accounting software is new territory for you.

Wave

Best for: New freelancers or anyone who wants to get started without a monthly fee.

Wave is genuinely free for the core invoicing and accounting features. No credit card required. The Pro plan at $16 a month adds automatic bank transaction imports and receipt scanning. The limitations are real. The free plan requires manual expense input, integrations are thin, and there’s no built-in time tracking. It covers the basics well, but most freelancers outgrow it within a year or two. When you do, migrating to FreshBooks or Xero is straightforward.

Zoho Books

Best for: Freelancers who want strong features at a lower price, or who already use other Zoho products.

Zoho Books is free for businesses with annual revenue under $50,000. Paid plans start at around $15 a month. The cash flow reports are detailed, automated payment reminders work well, and the mobile app is one of the better ones in this category. If you’re already on Zoho CRM, the two products talk to each other smoothly. The weakness is third-party integrations. If your workflow leans on tools outside the Zoho family, you’ll find fewer native connections than with Xero or QuickBooks.

Five Strategies That Help You Manage Cash Flow Faster

Tools help. They don’t replace process. These five practices make a measurable difference.

1. Invoice on the Day You Deliver

Every day between finishing work and sending the invoice adds a day to your payment timeline. Deliver on Friday, wait until Monday to invoice, and on Net 30 terms the client now has until Monday plus 30 days to pay. Four wasted days per invoice, every time, all year. Send the invoice the day you submit the work. Most tools let you prepare it in advance and fire it the moment you hand off the deliverable.

Finance teams measure this with a metric called days sales outstanding, or DSO. The lower your DSO, the healthier your cash position. Same-day invoicing alone typically cuts a freelancer’s DSO by 8 to 12 days, which is real money sitting in your account two weeks earlier than it would otherwise.

2. Put Payment Terms (and Late Fees) on Every Invoice

“Please pay when you can” is not a payment term. “Payment due within 7 days of invoice date” is. Put the actual due date on the invoice, not just the terms. “Due: April 17, 2026” reads clearer than “Net 14.” Net 7 is reasonable for project-based work under $2,000. Net 14 or Net 30 is standard for bigger projects. A 2% early payment discount can be worth offering. On a $5,000 invoice, a 2% discount costs you $100 and gives the client a concrete reason to push your invoice ahead of the others sitting in their AP queue.

For the other end of the curve: the standard freelance late fee is 1% to 1.5% per month on the overdue balance, which works out to 12% to 18% annualised. On a $5,000 invoice, a 1.5% monthly late fee adds $75 each month it’s overdue. The fee has to appear in the signed contract and on every invoice before the due date arrives. State usury caps vary, so check your local rules before charging anything above 18% annualised.

3. Automate Your Follow-Up Sequence

Send a reminder on day one overdue. Follow up on day 7. Follow up again on day 14. Make a phone call after that. Every tool in this guide automates at least the first two reminders. Set the sequence up once and let it run. Most late payments come down to disorganisation rather than bad intent. A well-timed reminder lands at the right moment, someone approves it, and the money moves.

4. Require a Deposit from New Clients

For any project over $1,000, require 50% upfront before work starts. The deposit filters out low-commitment clients and means that even if the final payment drags, your time and costs are already covered. For bigger projects, a 30/30/40 split works well: 30% on signing, 30% at a defined midpoint, 40% on completion. The cash moves throughout the project instead of arriving in one lump at the end.

If a new client refuses any deposit, treat that as information. Most established businesses expect to pay something upfront. Hard resistance usually points to cash flow problems on their end, which is the last thing you want to inherit.

5. Screen New Clients With These Seven Questions

Before you sign a contract, run the new client through this list. Ask in a discovery call or in writing. Their answers tell you most of what you need to know about how the engagement will end.

- Have you worked with freelancers before? What did the payment process look like?

- Who handles invoice approval and payment processing? A name and email, ideally.

- Do you have a vendor onboarding process? If yes, how long does it usually take from invoice to payment?

- What payment terms do you typically work with? If they say Net 60 or longer, decide upfront whether you can carry that much float.

- Are you comfortable with a 50% deposit before work starts? A flat no on first-time projects is a yellow flag.

- If a deliverable needs revisions, how do you usually handle scope and pricing changes? Vague answers here lead to invoice disputes later.

- Can you confirm the budget for this project is approved? Many late payments trace back to a project that was started before the client’s own internal sign-off.

If the hours you spend chasing a client cost more than the profit on the project, the project isn’t profitable. The screening list catches most of those clients before you sign.

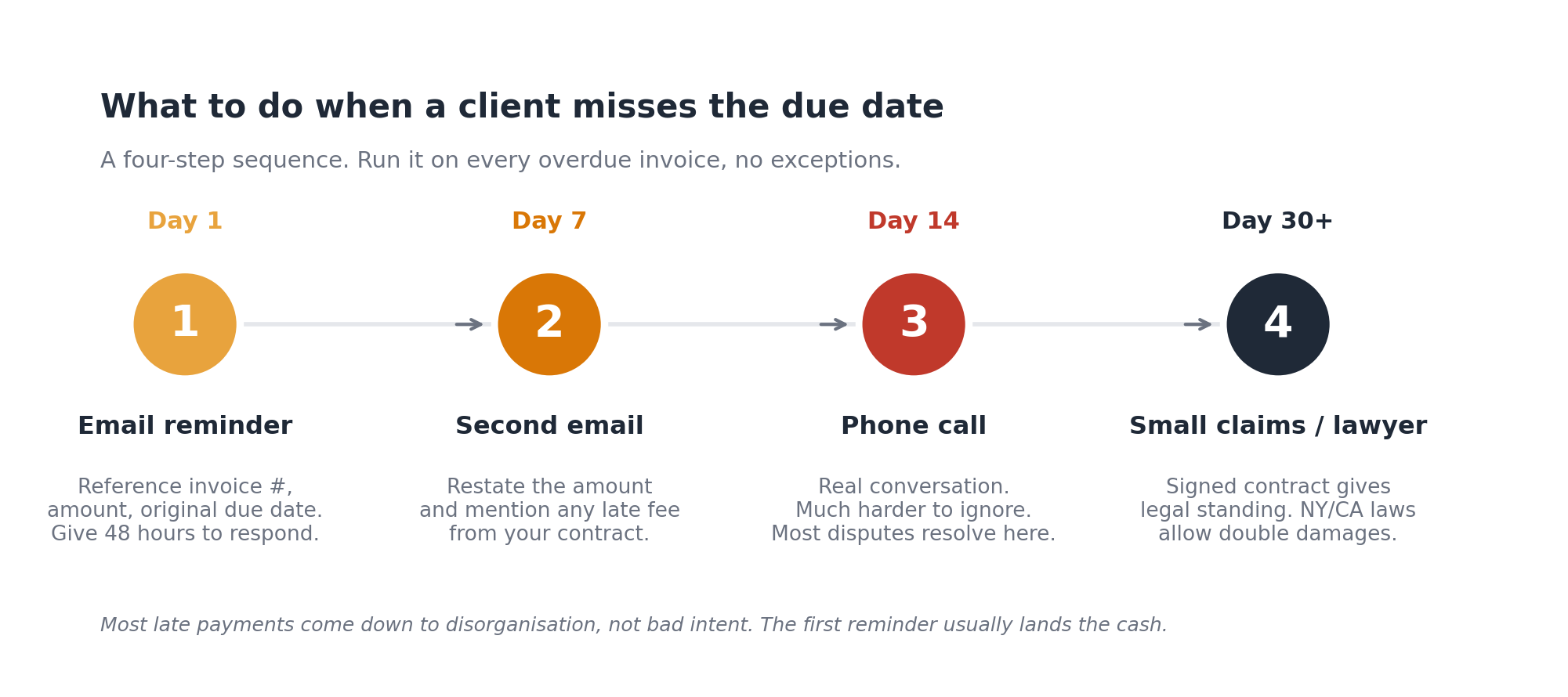

What to Do When a Client Doesn’t Pay

No strategy eliminates this entirely. At some point a client will go quiet. The following sequence handles most cases.

Start with a direct email referencing the invoice number, the amount, and the due date. Be specific: “Invoice #47 for $2,400 was due on March 15. Please confirm when this will be processed.” Give them 48 hours to respond before escalating.

If there’s no response, call. A phone call creates a real conversation and is much harder to ignore than email. Plenty of invoice disputes get resolved the moment someone picks up.

If the project was completed under a signed contract with clear payment terms, you have legal standing to pursue unpaid invoices. In New York, the Freelance Isn’t Free Act allows freelancers who win a case to recover double damages plus attorney’s fees on contracts of $800 or more. California offers similar protections under the Freelance Worker Protection Act. Small claims court handles most freelance disputes without requiring a lawyer. The cap varies by state, ranging from $2,500 in Kentucky to $25,000 in Tennessee and Delaware, with most states between $5,000 and $12,500.

For international clients, your best protection is the deposit. Once a project is complete and the dispute crosses borders, enforcement is expensive and slow.

How to Manage Cash Flow Around Tax Season

Tax sits in its own section because this is where freelancers get hurt most severely.

When you’re employed, taxes come out before you see the money. When you freelance, the gross amount lands in your account and it feels like yours. Most of it is. A meaningful chunk isn’t. Depending on your country and income level, 20 to 35% of every dollar belongs to the tax authority. Spend it before setting it aside and you’ll face a tax bill you can’t pay, on top of any cash flow problems you already have.

Set aside a fixed percentage of every payment received, immediately, into a separate account. In the US, 25 to 30% is a reasonable estimate for federal self-employment tax plus income tax for most freelancers. If you’re in a higher bracket or a high-tax state, go closer to 35%. Your accountant can give you a more precise figure and identify deductions you might be missing.

Quarterly estimated tax payments are required in the US if you expect to owe more than $1,000 for the year. The due dates are typically April 15, June 15, September 15, and January 15 of the following year. Missing them triggers an underpayment penalty, calculated on IRS Form 2210. If you missed a payment this year, pay it as soon as possible. The penalty accrues daily, so each week of delay costs more.

Include your tax set-aside in your cash flow forecast as an outgoing expense. It’s money you owe. Treat it that way from the moment it arrives.

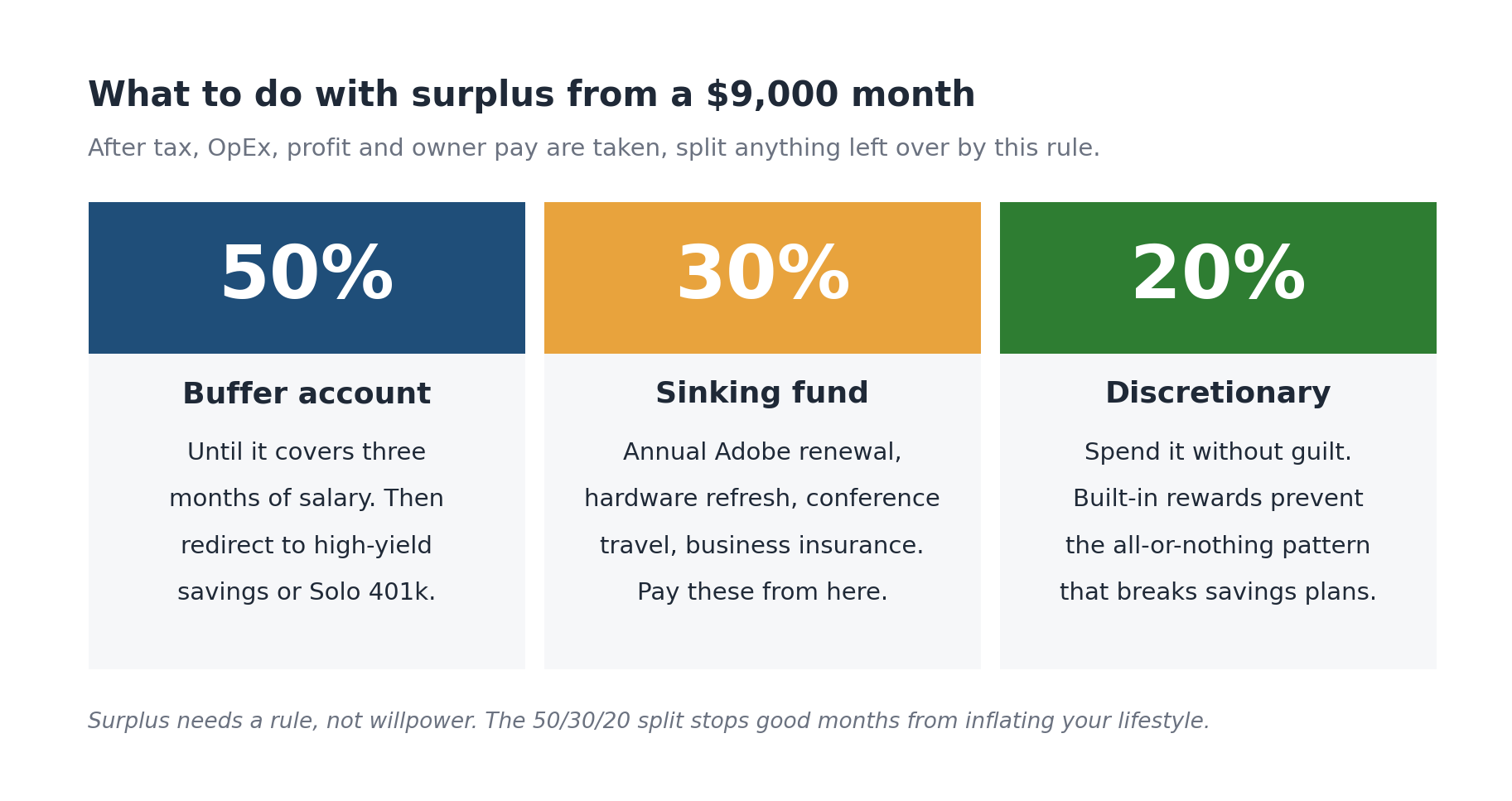

Surplus Rules: What to Do With a $9,000 Month

Most cash flow advice focuses on lean months. The bigger lifestyle risk is the good month. A $9,000 deposit lands and a freelancer who’s been worried for weeks suddenly buys a new monitor, upgrades a software plan, and books a long weekend away. Two months later, the buffer is empty.

Surplus needs a rule, not willpower. After your normal allocations (tax, OpEx, profit, owner pay) are taken, treat anything left over as one of three categories:

- 50% to the buffer account until it covers three months of salary. Once the buffer is full, redirect this slice to a high-yield savings account or retirement (Solo 401k or SEP IRA).

- 30% to a sinking fund for known irregular expenses. Annual Adobe renewal, hardware refresh every two years, conference travel, business insurance renewal. Pay these from the sinking fund when they hit, not from operating cash.

- 20% discretionary. Spend it without guilt. Built-in rewards prevent the all-or-nothing pattern that breaks most savings plans.

The 50/30/20 split stops high-income months from inflating your lifestyle and feeds the surplus into the buffer that gets you through the next slow stretch.

Retainer Clients: The Fastest Way to Manage Cash Flow Stability

Retainer clients are the most direct fix for cash flow chaos.

A retainer is a fixed monthly fee a client pays for ongoing access to your work, usually a set number of hours or deliverables per month. The income is predictable. The same amount arrives on the same date every month, which turns your forecasting from guesswork into planning.

One retainer client at $2,000 a month covers most freelancers’ fixed expenses. Two retainer clients at $1,500 each give you a stable floor. Project work on top of that becomes income for growth, not income for keeping the lights on.

Retainer work usually starts with project work done well. After a successful project, the conversation is straightforward: “I’d like to continue supporting you on an ongoing basis. I offer a monthly retainer of $X for Y hours per month.” Most clients who were happy with the work will at least consider it.

Start by converting one project client to a retainer. One is enough to change how the rest of the month feels.

Get Your Free Cash Flow Forecasting Template

I’ve put together a simple Cash Flow Forecasting Template in Excel and Google Sheets. Plug in your numbers and it calculates your 60-day cash position automatically. It covers:

- Incoming project and retainer payments

- All outgoing categories including tax set-asides

- A visual 8-week rolling forecast

- A buffer-account calculator with the salary baseline math worked out

- A warning flag when your projected balance drops below your target reserve

Frequently Asked Questions

How often should I update my cash flow forecast?

Weekly works for most freelancers. Block 30 minutes every Monday or Friday. If you’re using FreshBooks or Xero, most of the data updates automatically. You’re mainly reviewing the picture, not rebuilding it from scratch.

What if my income is completely irregular?

Take the average of your last six months as your baseline for incoming cash, then overlay your currently confirmed projects on top. The average tells you what to expect from recurring work. The confirmed projects tell you what’s actually coming. The combination gives you a realistic range, not the false optimism of best-case math or the panic of worst-case math.

Should I include taxes in my forecast?

Yes. Set aside 25 to 30% of every payment as it arrives and include the set-aside as an outgoing item. The money is not available to spend, so it should not look available in your forecast.

What’s the minimum cash reserve I should target?

Three months of fixed expenses, held in a separate savings account you don’t dip into for operating costs. If your fixed costs are $4,000 per month, target $12,000. The reserve protects you when two clients pay late in the same month, which will eventually happen.

Can I do this with a spreadsheet?

Yes. A well-built spreadsheet does everything described in this guide. The trade-off is time: building it, maintaining it, and updating it manually every week. Paid tools save 4 to 6 hours a month for most freelancers and reduce the chance you’ll skip updates when you’re busy. Wave’s free plan gives you the basics without a spreadsheet and without a monthly fee.

What payment terms should I use?

Net 7 is fair for projects under $2,000. Net 14 or Net 30 is standard for larger projects. Whatever you use, put the actual due date on the invoice. Ambiguity delays payment more than longer terms do.

What if I missed a quarterly tax payment?

Pay it as soon as you can. The IRS underpayment penalty is calculated on Form 2210 and accrues daily, so each week of delay adds to it. The penalty is generally modest (a few percentage points annualised on the underpaid amount), but it builds up over the year. If you’ve missed Q1 or Q2, you can catch up in Q3 or Q4 with a larger payment, though the penalty for the earlier quarter still applies. If you’ve missed every quarter, expect to owe a penalty when you file. A CPA can sometimes apply the safe harbor rule (pay 100% of last year’s total tax, or 110% if last year’s AGI was over $150,000, or $75,000 if married filing separately) to reduce or eliminate the penalty.

What questions should I ask a new client before signing?

Seven that catch most late payers in advance: have you worked with freelancers before; who handles invoice approval; do you have a vendor onboarding process; what payment terms do you usually work with; are you comfortable with a 50% deposit; how do you handle revisions and scope changes; and is the budget for this project already approved? The full screening list is in the Five Strategies section above.

Start Here

Pick one thing from this guide and do it today. No separate business account? Open one. Never set aside tax money? Move 28% of your last client payment into savings right now. Invoices going out days after work is complete? Set a rule that they go out same-day from here on. Want to stabilise your personal income first? Open the buffer account and set the salary baseline using your last six months of revenue.

You don’t need to overhaul everything at once. You just need to start.

If you want the fastest setup with the least friction, FreshBooks handles invoicing, expense tracking, payment reminders, and cash flow reporting in one place. It’s where a lot of freelancers land when they decide to get serious about their finances.

About the author

Gareth is an entrepreneur based in Dubai and the founder of AI Finance Tools for Freelancers. He’s not a CPA or a bookkeeper. He started this site after months of looking for honest, thorough reviews of AI finance tools written for freelancers, and not finding any. Every guide draws on real user reviews, official documentation, and expert sources.