How much should freelancers set aside for taxes? The honest answer sits between 22% and 35% of your net freelance income. The gap between those two numbers is about $5,000 a year on a typical income. Below is the math that decides where you land, plus a calculator built on the 2026 IRS figures.

You set aside 25% all year. You felt responsible. Then you filed your return and you owed another $2,400 you did not have. Sound familiar? This is what tax shock looks like in April, and it is preventable.

The “set aside 25 to 30 percent” advice you’ve read on Bonsai, Keeper, FreshBooks, NerdWallet, and every other freelancer blog is a starting point, not a finish line. The right number for you depends on four things. Get it wrong by three percentage points on $80,000 of income and you owe an extra $2,400 at filing time. This guide walks the actual math using 2026 brackets, gives you a working calculator, and shows you what moves your number up or down.

One housekeeping note before we start. Tax law shifted in July 2025 when the One Big Beautiful Bill Act became law. The QBI deduction is now permanent, the standard deduction stepped up, and the 2026 brackets reflect both inflation and the new structure. Older posts using 2024 figures or referencing a “QBI sunset” are out of date. Everything below uses the IRS 2026 numbers from Revenue Procedure 2025-32.

The short answer to how much should freelancers set aside for taxes

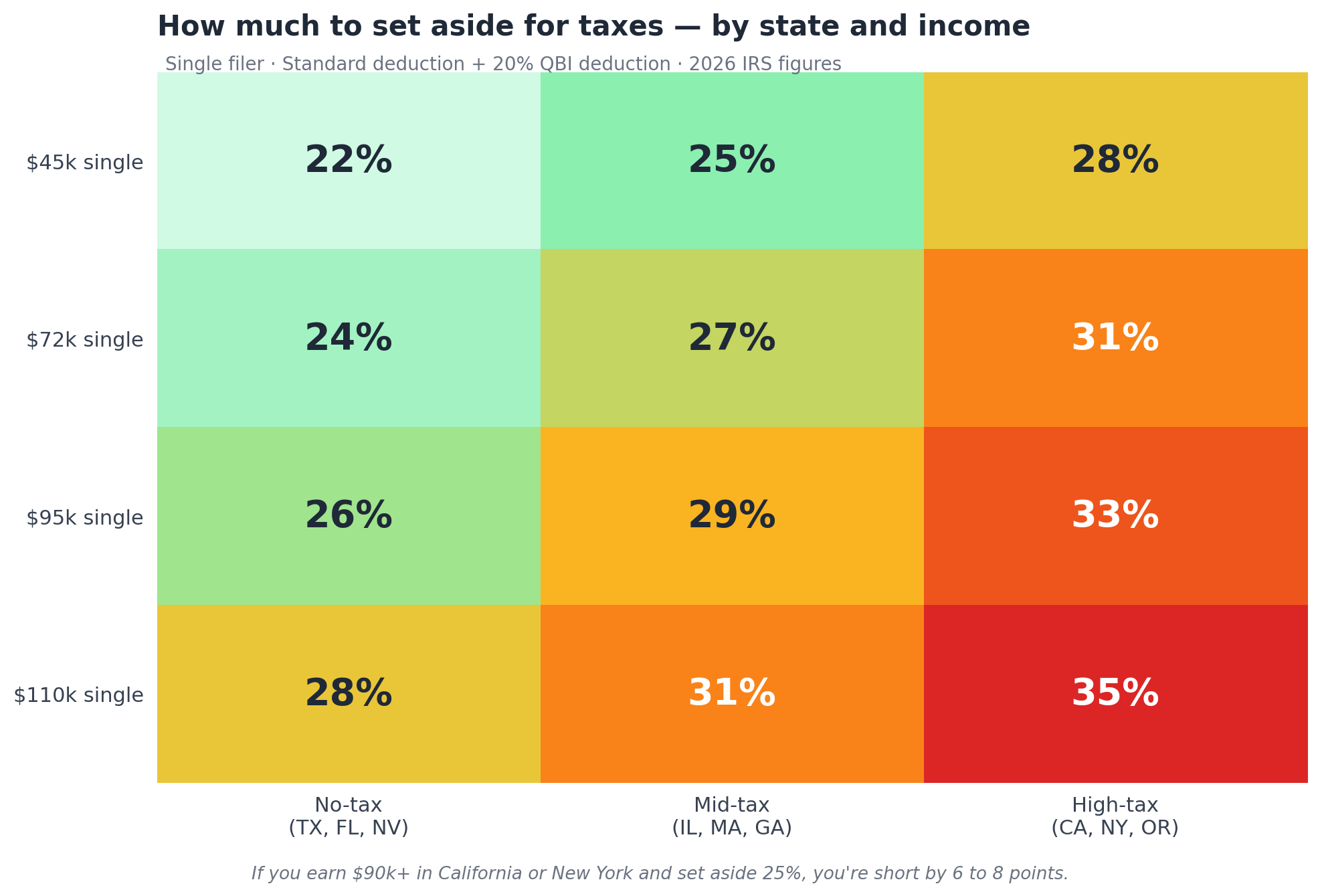

For most US freelancers earning $45,000 to $110,000 of net business income, set aside 22% to 32% of every freelance dollar that lands in your account. Where you sit inside that band depends on your state, your filing status, and how clean your books are.

Here is a rough breakdown by situation, before deductions and credits get involved:

If you’ve been setting aside 25% in California or New York at $90,000+ of income, you have been short by four to six percentage points. That is real money. On $90,000, six points works out to $5,400.

Why one percentage cannot work for everyone

Your total tax bill is three taxes stacked on top of each other. Each one responds to different things:

- Self-employment tax at 15.3% on 92.35% of your net earnings. This rate is flat for income up to $184,500 in 2026. It does not care about your state, your filing status, or your deductions. Anyone with $400 or more of net self-employment income owes it. See IRS guidance on self-employment tax.

- Federal income tax ranging from 10% to 37% depending on your taxable income. Your filing status, the standard deduction, retirement contributions, and the QBI deduction all change what counts as taxable.

- State income tax ranging from 0% in nine states to over 13% at the top in California. Your state runs its own brackets and does not care what the IRS says. The Tax Foundation’s 2026 state income tax breakdown covers every state.

The reason “25%” is the most repeated number on the internet is that it roughly equals 15.3% (SE tax) plus 10% (the effective federal rate at low incomes). For a $40,000 single freelancer in Florida claiming the standard deduction and the QBI deduction, that math is honest. For a $95,000 single freelancer in California with the same setup, it is wrong by eight points.

And here’s something the round-number advice never mentions. Your effective federal rate jumps the moment your taxable income clears $50,400 (single) or $100,800 (married filing jointly), because that is where the 22% bracket starts in 2026. Cross that line and your set-aside percentage needs to step up with it.

The four factors that move your real number

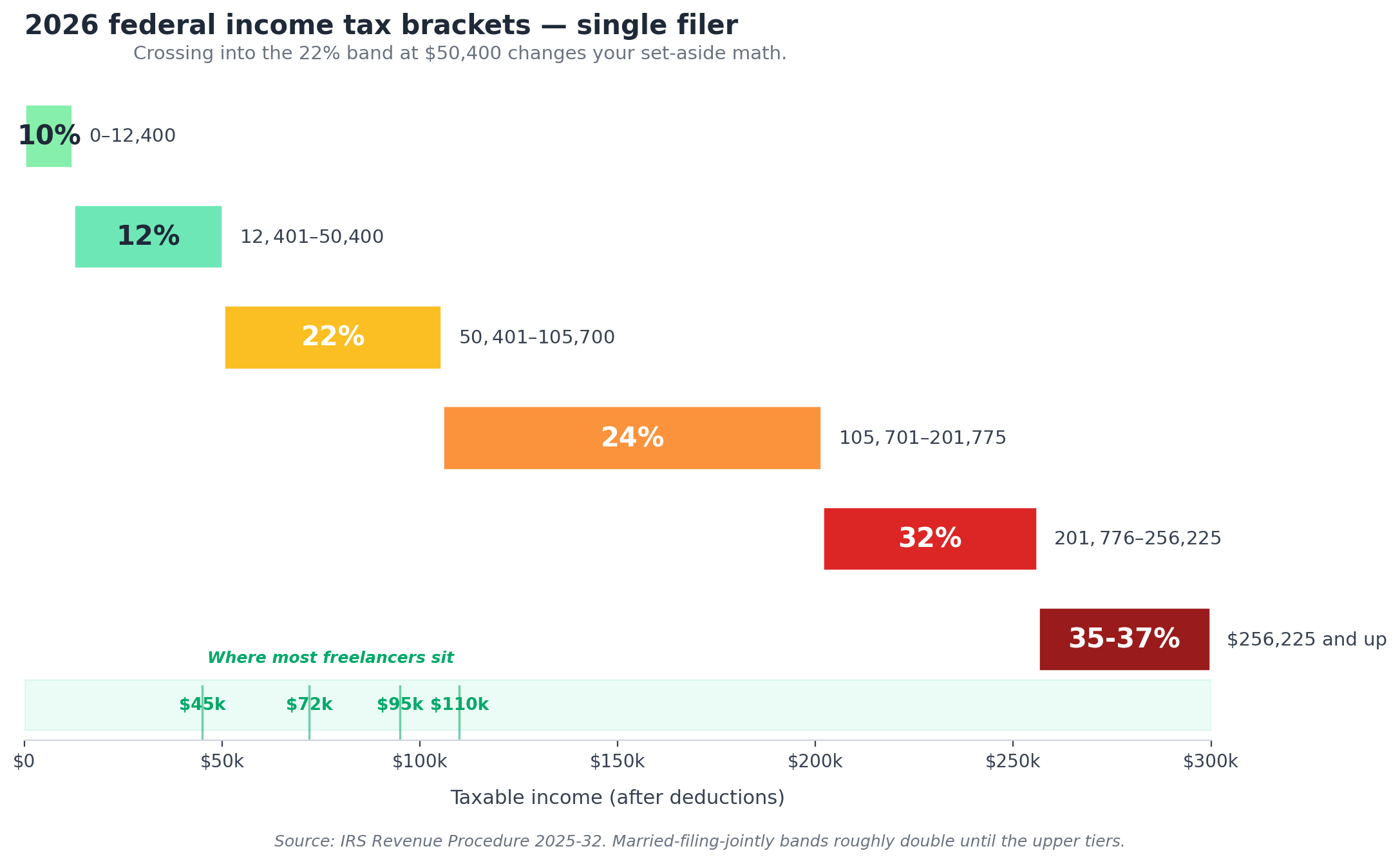

1. Your federal tax bracket (and where you sit inside it)

The 2026 federal income tax brackets for a single filer:

- 10% on taxable income up to $12,400

- 12% on income from $12,401 to $50,400

- 22% on income from $50,401 to $105,700

- 24% on income from $105,701 to $201,775

- 32% on income from $201,776 to $256,225

- 35% and 37% above that

Married filing jointly, the brackets double until you hit the higher tiers. Source: IRS Revenue Procedure 2025-32.

What matters for your set-aside percentage is your marginal rate, the rate on the next dollar you earn. A single freelancer with $80,000 of taxable income pays 22% on every additional dollar, even if their effective (average) rate is closer to 13%. That’s why crossing into 22% territory matters more than the small bracket movements below it.

2. Self-employment tax (the part W-2 employees never see)

SE tax is the bit that breaks the brain of every first-year freelancer. As a W-2 employee, you paid 7.65% in payroll taxes and your employer paid the matching 7.65%. As a freelancer, you pay both halves. That’s 15.3% of your net earnings, before any income tax shows up.

Two technical details to know. First, you only pay SE tax on 92.35% of your net earnings, not the full amount. The IRS lets you exclude the employer-equivalent half from the base. Second, you can deduct half of your SE tax when working out your federal income tax. So 15.3% feels worse on paper than it lands in practice. It’s still the largest single line on most freelancers’ tax bills.

For 2026, the 12.4% Social Security portion stops applying once your combined wages and self-employment income hit the Social Security wage base for 2026 of $184,500. Above that, only the 2.9% Medicare portion continues, plus a 0.9% Additional Medicare Tax above $200,000 (single) or $250,000 (joint). Most readers won’t hit those thresholds. If you do, your effective SE tax percentage drops, which is one of the few good things about earning more.

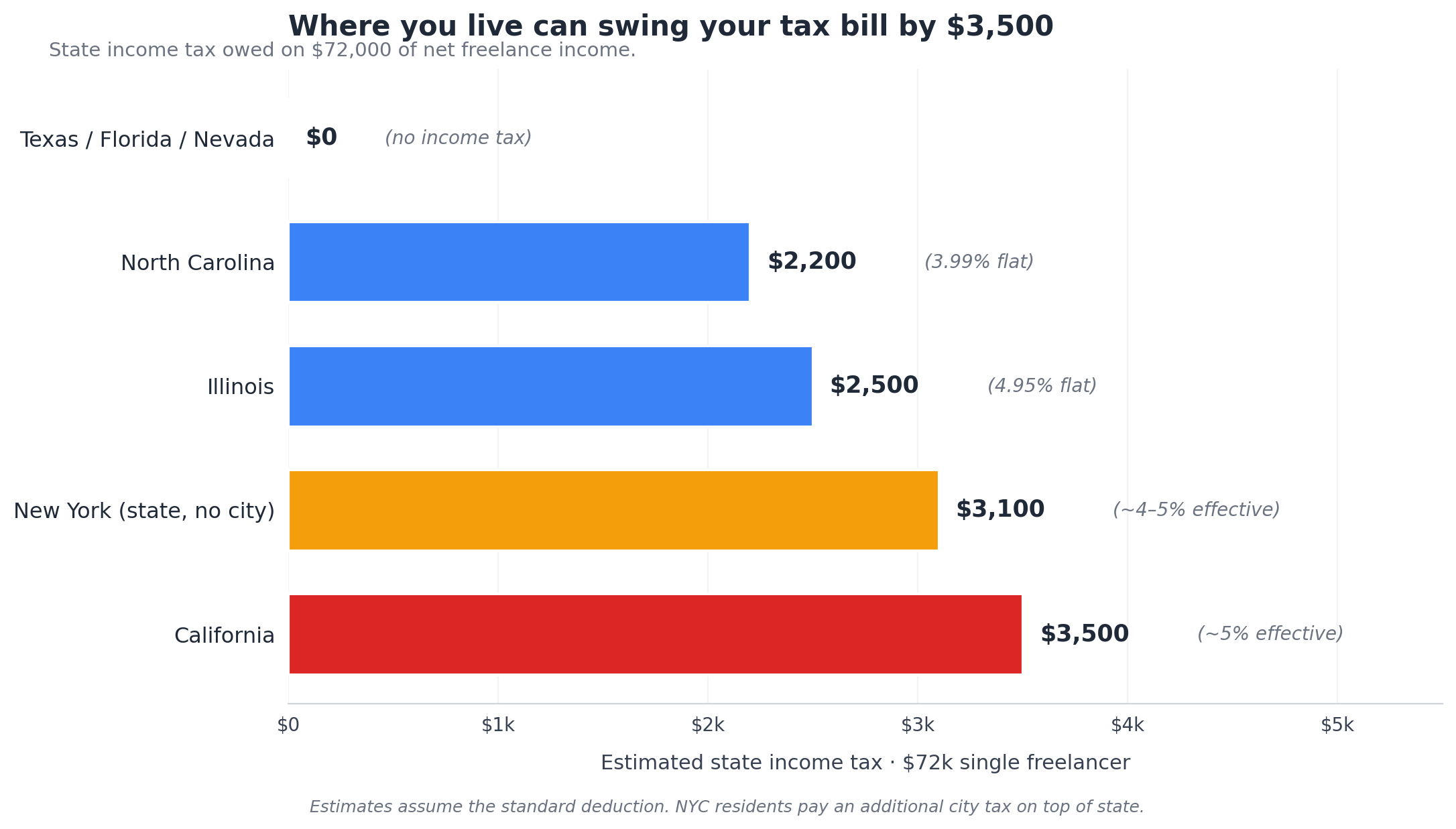

3. Your state’s income tax

Where you live can swing your set-aside number by 7 to 9 percentage points. The nine states with no income tax (Texas, Florida, Nevada, Washington, Tennessee, South Dakota, Wyoming, Alaska, and New Hampshire) give you the lowest total burden. California, New York, Hawaii, Oregon, Minnesota, and New Jersey put you on the high end.

For a $72,000 single freelancer, here’s what state tax adds:

If you live in a high-tax state and you’ve been copying the same percentage as a friend in Florida, you have been short. Always.

4. Deductions you actually qualify for

The big three for most freelancers are the standard deduction, the QBI deduction, and retirement contributions. Each one cuts your taxable income, which cuts your federal tax bill, which cuts your set-aside percentage. For a fuller list, see the deductions most freelancers miss.

- Standard deduction (2026): $16,100 single, $32,200 married filing jointly, $24,150 head of household. You get this without itemizing.

- QBI deduction (Section 199A): up to 20% of your qualified business income, made permanent by the One Big Beautiful Bill Act. Reported on Form 8995 (or Form 8995-A if you’re in the phase-in range). For 2026 there’s also a new minimum deduction of $400 for anyone with at least $1,000 of active QBI. Phase-ins start at $201,750 single or $403,500 MFJ. Below those thresholds (where most readers sit), you get the full 20%.

- Half of self-employment tax: automatically deductible when you fill in Schedule SE.

- Retirement contributions: a SEP IRA contribution can shave 20% of your net SE income off your taxable income. A Solo 401(k) can go higher. We have a separate guide on picking the right accounting software that flags retirement contribution tracking.

The QBI deduction is the one most freelancers underuse, because they didn’t realise it survived the 2025 sunset. It did. If you have $60,000 of qualified business income, the QBI deduction takes $12,000 off your taxable income before the federal brackets even start to bite.

Calculate your real number

The calculator below answers exactly how much should freelancers set aside for taxes given their own situation. It uses the 2026 IRS figures: $184,500 Social Security wage base, the 15.3% SE tax rate on 92.35% of net earnings, the 2026 federal brackets, the 20% QBI deduction, and 2026 standard deductions. Plug in your numbers.

Freelancer Tax Set-Aside Calculator (2026)

Enter your numbers. Estimates only. Verify with a CPA before you file.

Three real examples worked out

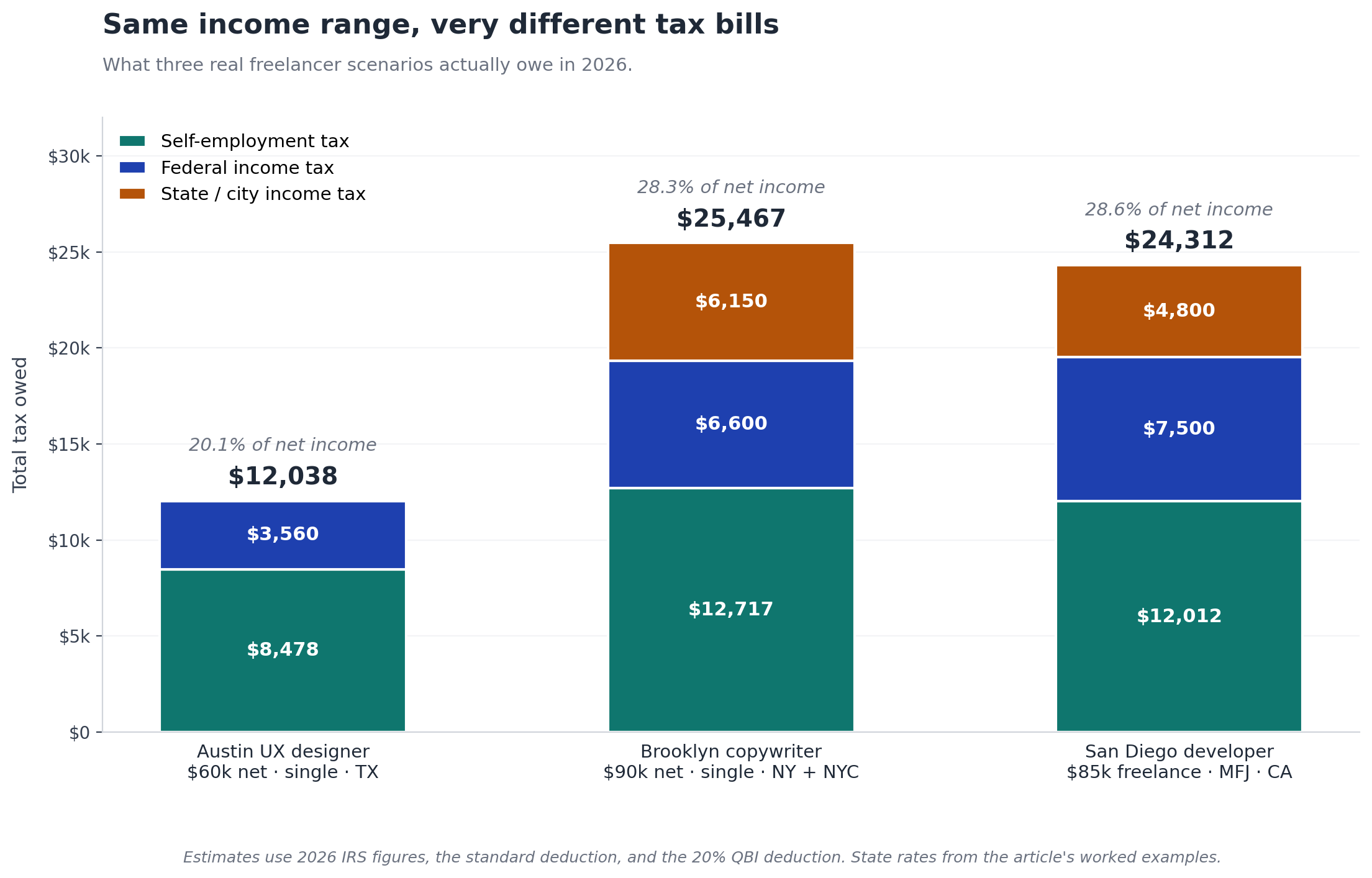

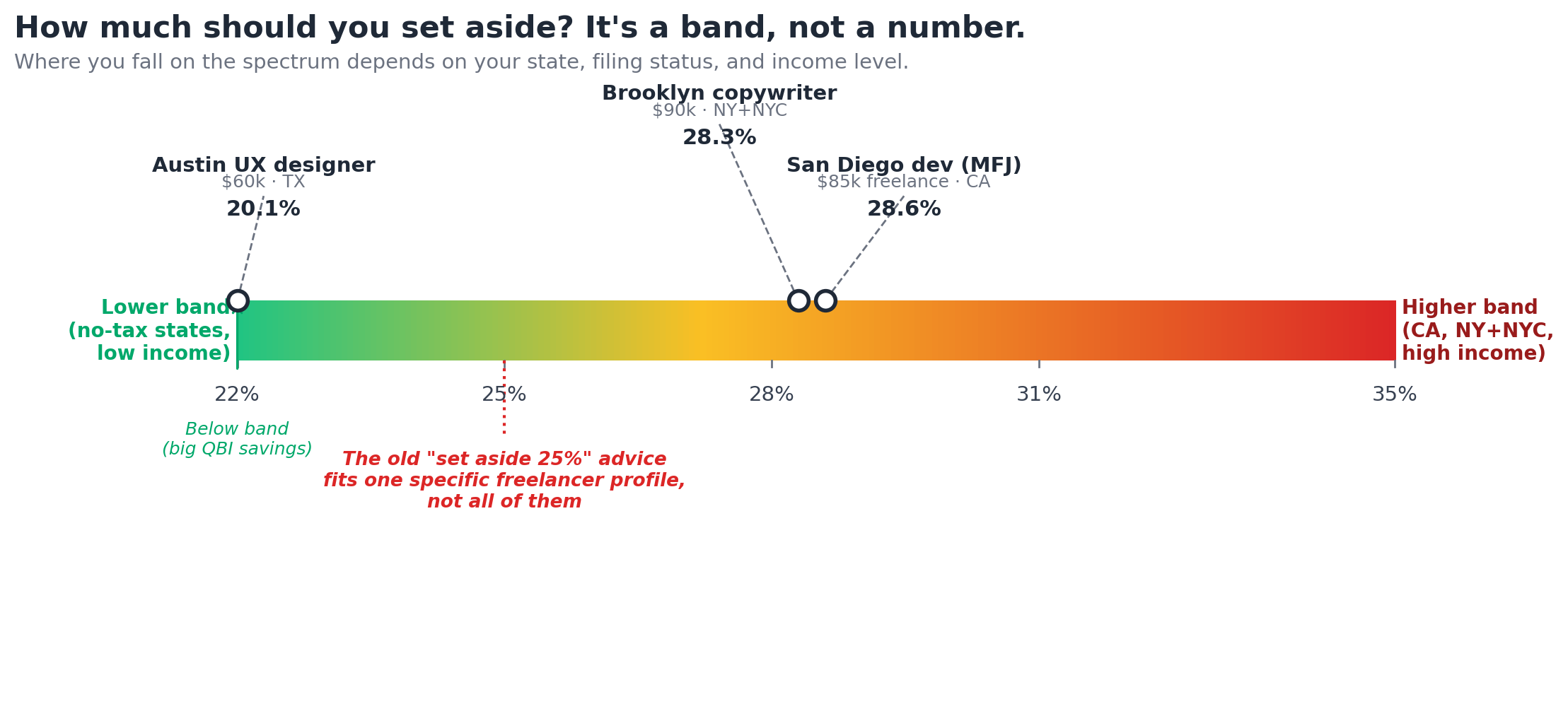

A freelance UX designer in Austin, $60,000 net, single filer

You bill clients $80,000 over the year. After laptop depreciation, software subscriptions, your home office, and other deductions, your net is $60,000. Texas has no state income tax.

- SE tax: $60,000 × 92.35% × 15.3% = $8,478

- AGI after half-SE deduction: $55,761

- After standard deduction ($16,100) and QBI deduction (about $7,932): taxable income around $31,729

- Federal income tax: roughly $3,560

- State tax: $0

- Total: $12,038. Set aside 20% of net income, or about $1,000 a month.

A freelance copywriter in Brooklyn, $90,000 net, single filer

Same setup, different state. New York runs progressive state tax that lands around 5.5% effective at $90,000.

- SE tax: $12,717

- Federal income tax (after standard deduction and 20% QBI): roughly $6,600

- NY state and city tax (combined effective ~6.8% on this income): roughly $6,150

- Total: $25,467. Set aside 28.3% of net, or about $2,122 a month.

NYC residents pay an extra city income tax on top of state. If you live in Manhattan or Brooklyn and you’ve been setting aside 25%, you’re about $3,000 short every year. That’s the difference between paying your CPA bill and paying the IRS interest.

A freelance developer plus W-2 spouse in San Diego, $85k freelance + $70k W-2, MFJ

Married filing jointly changes the brackets and the standard deduction. The W-2 income is already taxed through payroll, so your set-aside on the freelance side only covers the freelance portion.

- SE tax on $85,000: $12,012 (the W-2 income doesn’t affect this because the spouse earns it, and combined income is below the $184,500 SS cap anyway)

- Joint AGI: roughly $148,994

- After joint standard deduction ($32,200) and 20% QBI on the freelance portion: taxable around $101,000

- Federal income tax: roughly $11,600, but most of that is already covered by the spouse’s W-2 withholding. The marginal portion attributable to the freelance income is around $7,500

- CA state tax on the freelance income: roughly $4,800

- On the freelance income alone: set aside about 28.6%, or $2,025 a month from the $85,000.

The W-2 spouse’s withholding does real work here. If you’re MFJ and one of you has steady W-2 income, ask your spouse to bump up their W-4 withholding to cover the freelance portion. This gives you a withholding buffer that handles penalties more cleanly than quarterly estimated payments do.

The safe harbor rule (the only real way to avoid penalties)

The IRS does not technically care if you owe money in April. They care that you’ve paid enough during the year to satisfy one of two safe harbor tests.

- Pay 90% of your current year’s tax through quarterly payments and any withholding. Hard to do because you don’t know your final number until the year is over.

- Pay 100% of last year’s total tax (110% if your prior year AGI was over $150,000). This is the lazy-person safe harbor and what most freelancers should aim for.

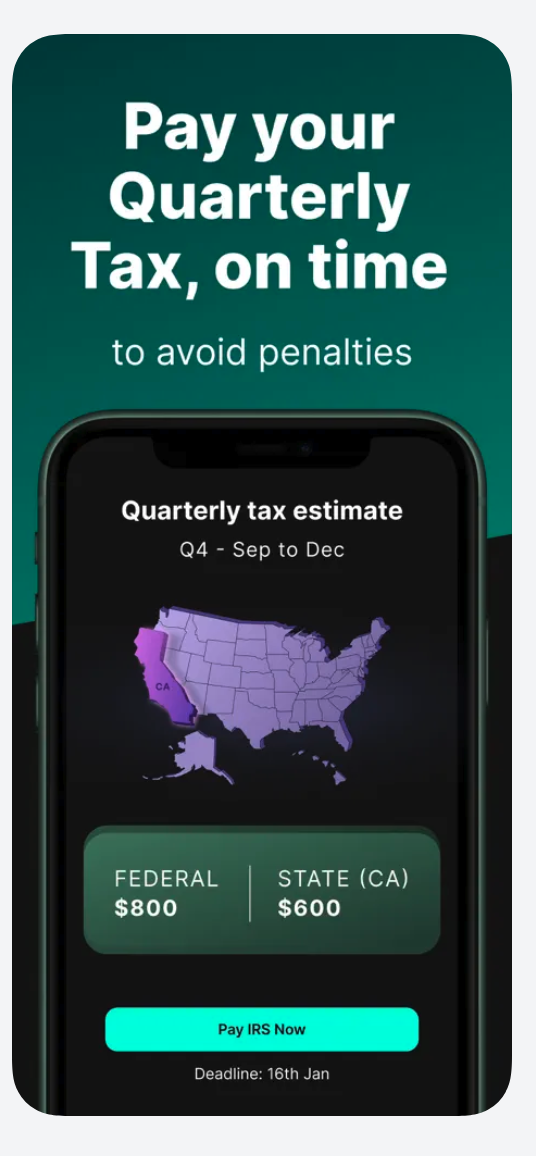

If your 2025 total tax was $18,000, paying $4,500 each quarter in 2026 ($18,000 ÷ 4) puts you in the safe harbor regardless of how much you make this year. You might still owe in April, but the IRS won’t charge you the underpayment penalty.

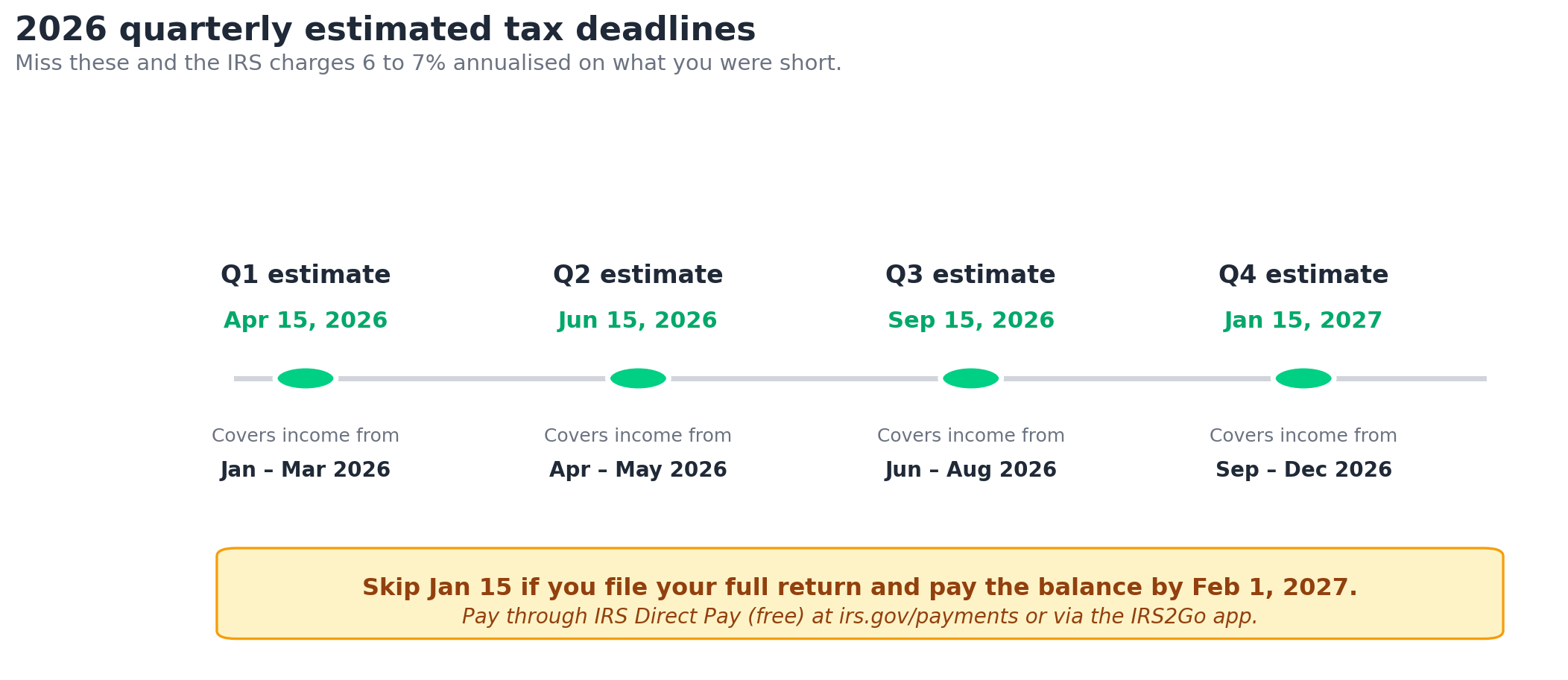

The 2026 quarterly deadlines are April 15, June 15, September 15, and January 15, 2027. You can also skip the January 15 payment if you file your return and pay the balance by February 1, 2027. Source: IRS Form 1040-ES.

The penalty if you miss the safe harbor is the federal short-term rate plus three percentage points, charged on the underpayment for each quarter you were short. The IRS set that rate at 7% for the first quarter of 2026 and 6% for the second quarter, so the working figure is roughly 6 to 7% annualised. On a $5,000 underpayment for nine months, that comes to about $200 to $250. Annoying, not catastrophic. The bigger danger is the cash crunch in April when you owe the unpaid balance plus the penalty in one go.

Tools that handle this for you (and what’s wrong with them)

Two AI-flavoured tools dominate the freelancer tax space right now. Both calculate your quarterly estimates by reading your bank transactions. Both have real strengths and real flaws. Honest summary, then you decide.

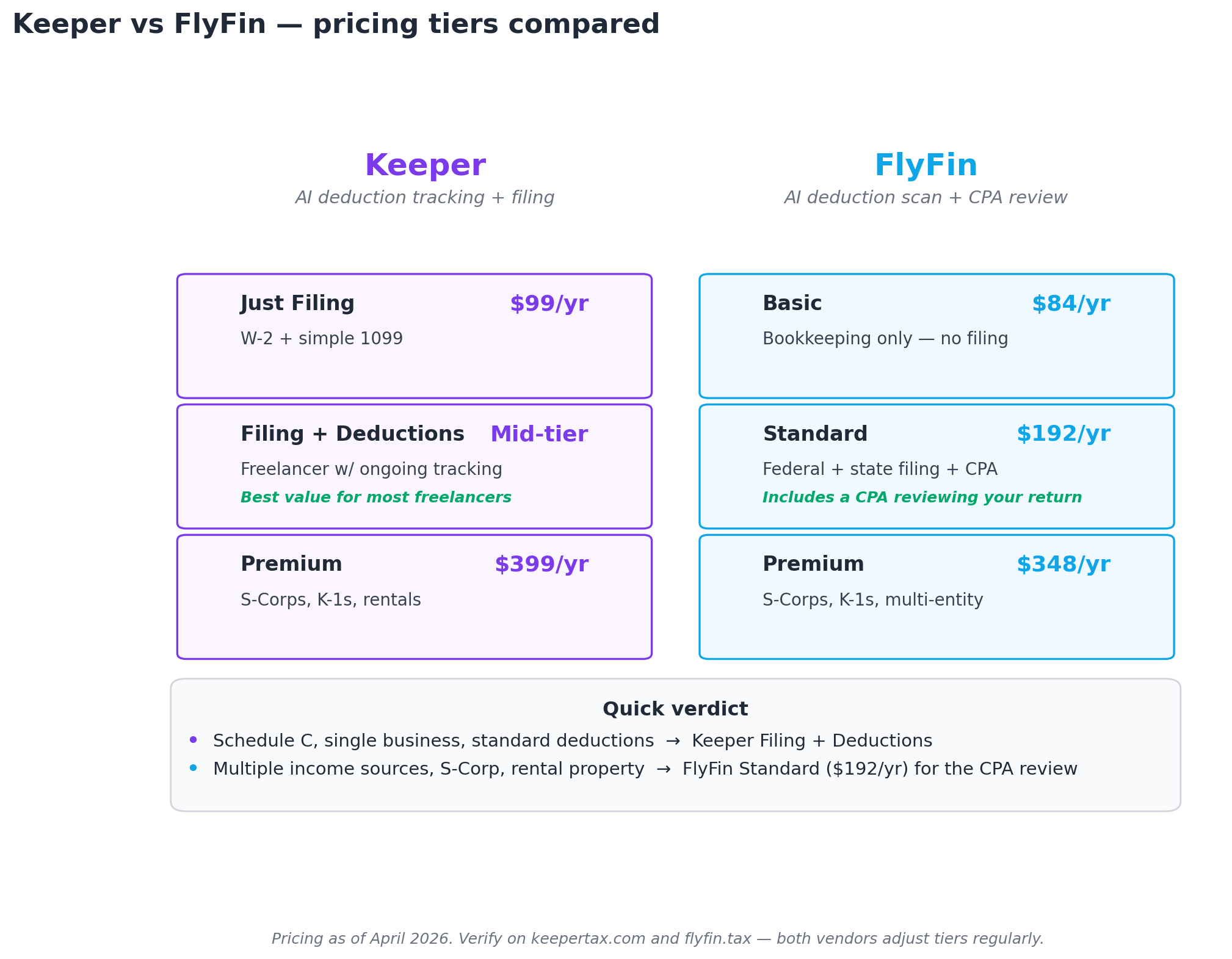

Keeper

Keeper (formerly Keeper Tax) connects to your bank and credit card accounts and texts you when it spots a possibly deductible expense. The interface is mobile-first, and the daily verification flow is the cleanest of any tool I’ve used. Keeper now sells three annual plans rather than the older monthly setup: $99/year for Just Filing (W-2 plus simple 1099), a middle Filing + Deductions tier for freelancers with ongoing expense tracking, and $399/year for Premium (S-Corps, K-1s, rental property, complex situations). Check the current pricing page on keepertax.com before you sign up because the middle-tier figure has been moving.

What works well, based on G2 and Capterra reviews from freelancers and 1099 contractors: automated transaction categorisation, the daily SMS verification flow, and the $800 to $2,400 in deductions Keeper claims to find for the average user. What doesn’t: the $399 Premium price increase upset long-term users (one Google Play review I read called it “out of bounds” compared to the prior $200ish tier), and the BBB has complaints about email-only support and unexpected charges after free trials. The web interface lags well behind the mobile app.

Visit Keeper’s official website for current pricing and a free trial.

FlyFin

FlyFin pairs AI deduction scanning with a real CPA who prepares and files your return. Pricing as of April 2026: $84/year Basic (bookkeeping only), $192/year Standard (includes federal and state filing), $348/year Premium (S-Corps, K-1s, multi-entity). All tiers include a 7-day free trial.

What works well: the CPA review on every return is the headline feature, and reviewers consistently call out the swipe-to-classify mobile interface as the best in the category. The estimated quarterly tax tool calculates your safe harbor amounts automatically based on connected accounts. What doesn’t: there’s no integrated mileage tracking (you need a separate app like MileIQ for that), the bookkeeping-only Basic plan does not let you actually file taxes, and the platform is mobile-first to a fault if you prefer working on a desktop. Some users complain that the CPA hand-off has occasional delays during peak filing season.

Visit FlyFin’s official website for current pricing and the 7-day free trial.

The honest comparison

If your situation is straightforward (Schedule C, single business, standard deductions), Keeper at the Filing + Deductions tier is probably the best value. If you want a CPA review on your actual return because your situation is messier (multiple income sources, S-Corp, rental property), FlyFin Standard at $192/year edges ahead. If you want to do nothing and have a human file for you, hire a local CPA for $500 to $900. Neither tool replaces a CPA when your situation is genuinely complicated, and both companies will tell you that if you ask.

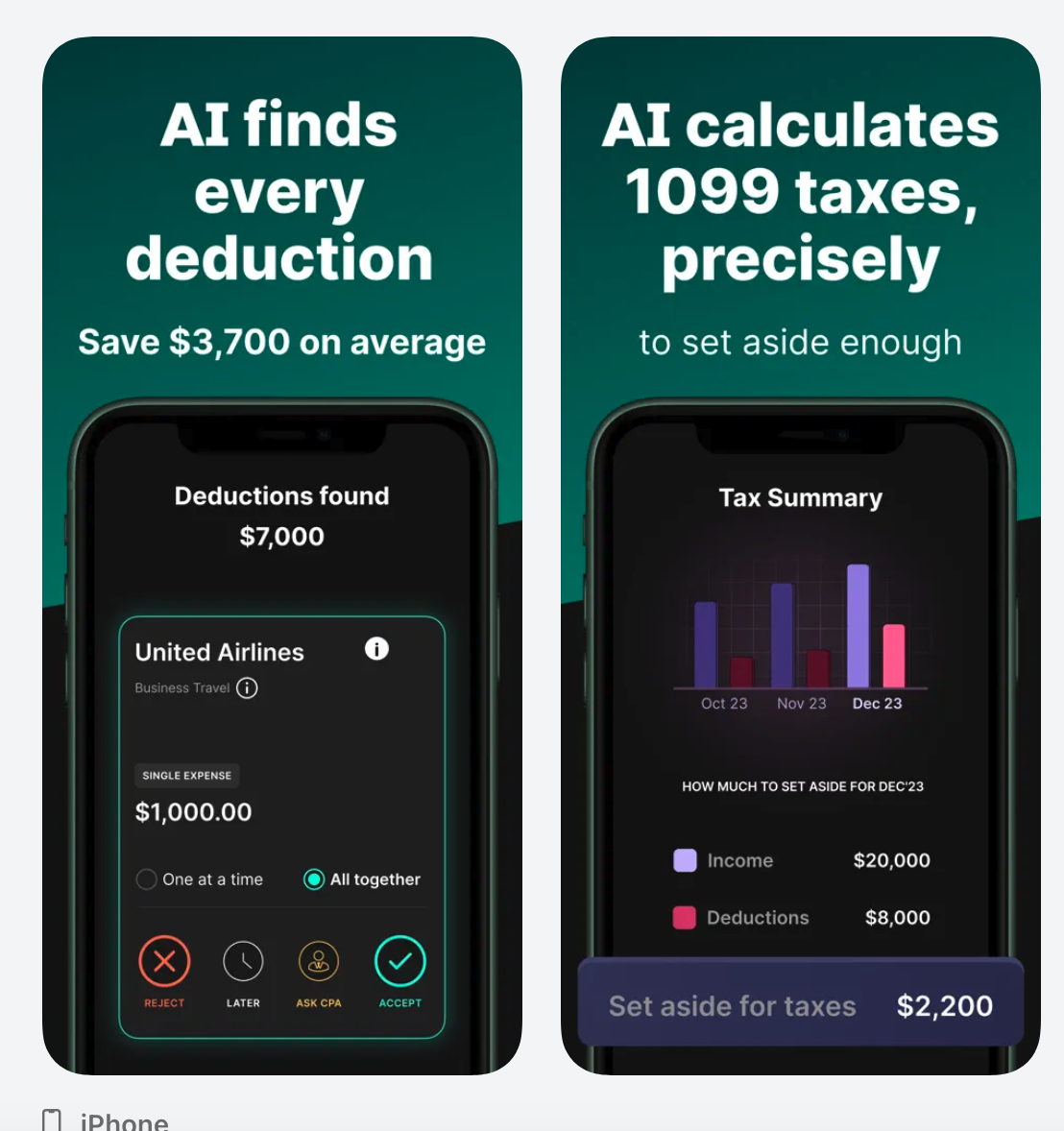

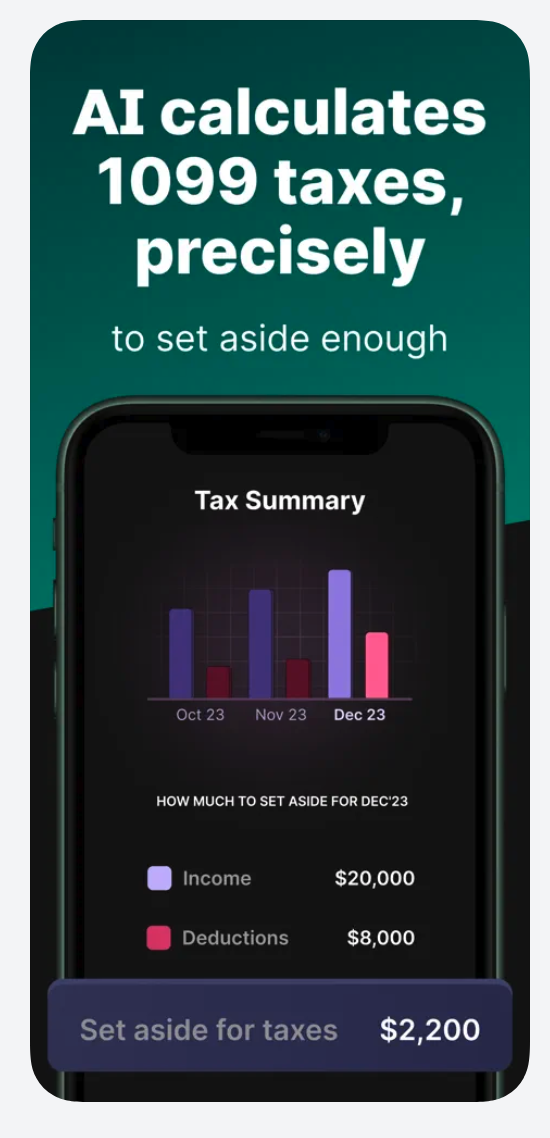

For the basic question of how much to set aside each month, you don’t need either tool. The calculator above does the same calculation. Where these tools earn their fee is in finding deductions you would have missed, which can return $800 to $3,000 a year for an active freelancer.

Want a deeper comparison? See our freelancer accounting software roundup, which covers QuickBooks, Wave, FreshBooks, Bonsai, and Indy alongside the AI tools.

Common mistakes that cost you money

Six mistakes I see over and over in freelancer subreddits and in my own client conversations:

- Setting aside on gross income instead of net. Your taxes are calculated on your net (after expenses). If you bill $100,000 and have $25,000 of legitimate expenses, you set aside on $75,000. Setting aside on $100,000 is overkill and starves your cash flow during the year.

- Forgetting the SE tax part. Brand new freelancers calculate their federal income tax (say, 12% effective), set aside that, and get blindsided in April when they discover they also owe 15.3% in SE tax on top.

- Ignoring 1099-NEC and 1099-K reporting. If clients pay you $600 or more, you get a 1099-NEC. If you take card payments through Stripe, PayPal, or Square totalling $5,000 or more in 2026 (the threshold drops further to $2,500 for 2026 reporting after the OBBBA-era phase-in), you also get a 1099-K. The IRS has those forms before you file. The set-aside math you do for yourself is the only thing standing between you and a surprise.

- Mixing personal and business in one bank account. If you cannot separate which transactions are business expenses, you cannot deduct them properly, and you over-set-aside as a defensive move. Open a separate business checking account on day one. Our guide to tracking business expenses walks through the setup.

- Not adjusting mid-year for income changes. A big Q3 retainer from a new client changes your numbers. So does a quiet summer. Recalculate your set-aside in July using your year-to-date income and re-project the remaining months.

- Keeping the tax money in your regular checking. You will spend it. Open a separate “Taxes” savings account and transfer the percentage from every payment that comes in. Treat that account as untouchable until quarterly deadlines. If you also struggle with month-to-month flow, the freelancer cash flow basics guide covers the wider system.

The mid-year recalculation is the one most freelancers skip. Your January estimate was based on your December assumptions. By July, you know whether the year is going better or worse. Re-running the numbers in early July (right after the Q2 deadline) takes 15 minutes and saves you more money than anything else on this list.

Get the freelancer tax setup checklist

One PDF. The accounts to open, the percentages to set aside, the deadlines for 2026, the exact line items on Schedule C and Schedule SE, and the QBI deduction worksheet flow. Built for US freelancers earning $45k to $110k who want to stop guessing. Drop your email and it lands in your inbox in two minutes.

Frequently Asked Questions

Is 30% always safe?

Thirty percent is safe for most single freelancers earning $60,000 to $110,000 in mid-tax states. It’s an over-set-aside if you live in Texas or Florida and earn under $70,000 (you should be closer to 22 to 24%). It’s an under-set-aside if you live in California or New York City and earn over $90,000 (you need 32 to 35%). The calculator above gives you the actual number for your situation.

Do I have to make quarterly payments?

Yes, if you expect to owe at least $1,000 in tax for the year after withholding and credits. If your total tax bill is going to be under $1,000 (rare for anyone earning meaningful freelance income), you can pay it all when you file. The 2026 deadlines are April 15, June 15, September 15, and January 15, 2027. Pay through IRS Direct Pay at irs.gov/payments for free, use the IRS2Go mobile app, or enrol in EFTPS at eftps.gov if you also pay business taxes (EFTPS is the better choice if you ever expect to run payroll or pay corporate taxes from the same account).

What happens if I underpay during the year?

The IRS charges an underpayment penalty equal to the federal short-term rate plus three percentage points, calculated quarter-by-quarter on the amount you were short. The rate was set at 7% for Q1 2026 and 6% for Q2 2026, so plan on roughly 6 to 7% annualised. On a $4,000 underpayment for half the year, the penalty comes to about $120 to $140. You also still owe the underpaid tax in April, plus interest on any unpaid balance after the filing deadline. The penalty isn’t the worst part. The cash crunch is.

Do business expenses lower my self-employment tax?

Yes. SE tax is calculated on your net earnings (gross minus business expenses), not your gross. Every legitimate deduction you take cuts your SE tax base by 15.3 cents on the dollar, on top of lowering your federal income tax. This is why expense tracking matters so much for freelancers. Missed expenses get taxed at the full freelancer rate of around 30%, including the SE portion.

Can I just have my W-2 employer withhold extra to cover my freelance taxes?

Yes, and this is one of the most underused freelancer tactics around. If you also have W-2 income (yours or a spouse’s on a joint return), you can submit a new Form W-4 with extra withholding on Line 4(c). Withholding is treated as if it was paid evenly throughout the year, which means it covers all four quarters at once. Cleaner than quarterly estimated payments, especially if your freelance income is lumpy.

Does the QBI deduction lower my self-employment tax too?

No. The QBI deduction only reduces your federal income tax, not your SE tax. The 15.3% you owe on your net earnings does not budge regardless of how much QBI deduction you take. Source: IRS guidance on Section 199A.

What if my income is wildly different each month?

Set the percentage from every payment you receive, the moment it lands. If your set-aside is 28% and a $4,000 client payment hits, transfer $1,120 to your tax account that day. This handles uneven income months automatically because you set aside on actual income rather than projected income. Some freelancers also use the IRS annualised income installment method (Form 2210, Schedule AI) to recalculate quarterly amounts based on the income earned in each quarter, which avoids penalties when most of your income comes late in the year.

Should I incorporate or stay a sole proprietor to lower my taxes?

Sole proprietors pay full SE tax on all net earnings. S-Corp owners pay SE tax (technically FICA tax) only on the W-2 salary they pay themselves, and the rest comes out as distributions which avoid SE tax. The catch is that the salary has to be “reasonable” by IRS standards, you have to run actual payroll, and you’ll pay $500 to $1,500 a year in extra accounting fees. The break-even point where S-Corp election starts saving you money is usually around $60,000 to $80,000 of net business income, depending on your state. We have a separate guide on this trade-off coming soon.

This guide on how much should freelancers set aside for taxes is informational and reflects 2026 IRS figures from Revenue Procedure 2025-32 and the One Big Beautiful Bill Act. Tax laws change. Verify everything against IRS.gov or work with a CPA before you file. Nothing here is tax, legal, or financial advice.

About the author

Gareth is an entrepreneur based in Dubai and the founder of AI Finance Tools for Freelancers. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide on this site is researched from real user reviews, official IRS documentation, and primary sources, then pressure-tested against the questions actual freelancers are asking on Reddit, G2, and BBB.