![]()

By Gareth · Founder, AI Finance Tools for Freelancers

Published: May 1, 2026 · Last reviewed: May 1, 2026

The home office deduction for freelancers is simpler than people think. A 200 sq ft office in a 2,000 sq ft home is worth $1,000 with the simplified method or $4,000+ with actual expenses. Here’s how to figure out which one wins for you, and how to claim it without raising flags.

Get the Home Office Deduction Worksheet

The home office deduction for freelancers is one of the most under-claimed write-offs in self-employment. Not because people don’t qualify. Because they’re scared of an audit.

You shouldn’t be. The rule is simple. Use a specific area of your home regularly and only for work, and the IRS lets you deduct part of your housing costs. That’s straight out of IRS Publication 587, the document the IRS itself wrote to explain the rules.

What follows is a plain breakdown of who qualifies, the two methods you can pick from, the actual math at four different freelancer setups, and the documentation that protects you if the IRS ever asks. No hedging. Real numbers.

Who qualifies for the home office deduction for freelancers (2026)

You qualify if you’re self-employed and you use part of your home for business in two specific ways: regularly and exclusively. Both words matter.

- Regular use means consistent, ongoing business activity. Not once a month when you happen to remember.

- Exclusive use means that area gets used only for work. Your kid doesn’t do homework at the desk. Your partner doesn’t fold laundry there.

The space also has to be your principal place of business. For most freelancers, this is automatic. You take client calls there, you do the work there, you handle invoicing and admin there. Even if you have a coworking membership, your home still qualifies as long as that’s where the bulk of your work hours land.

One thing that trips people up. W-2 employees don’t qualify. The Tax Cuts and Jobs Act removed unreimbursed employee business expenses starting in 2018, and that change is still in effect through 2025. If you’re a hybrid worker with a day job and a freelance side gig, you can only deduct the portion tied to your self-employed work, not the W-2 work.

The exclusive-use test has two narrow exceptions. Storage of inventory or product samples for a wholesale or retail business. And a licensed daycare. Most freelancers fall into neither, so assume you need a dedicated space.

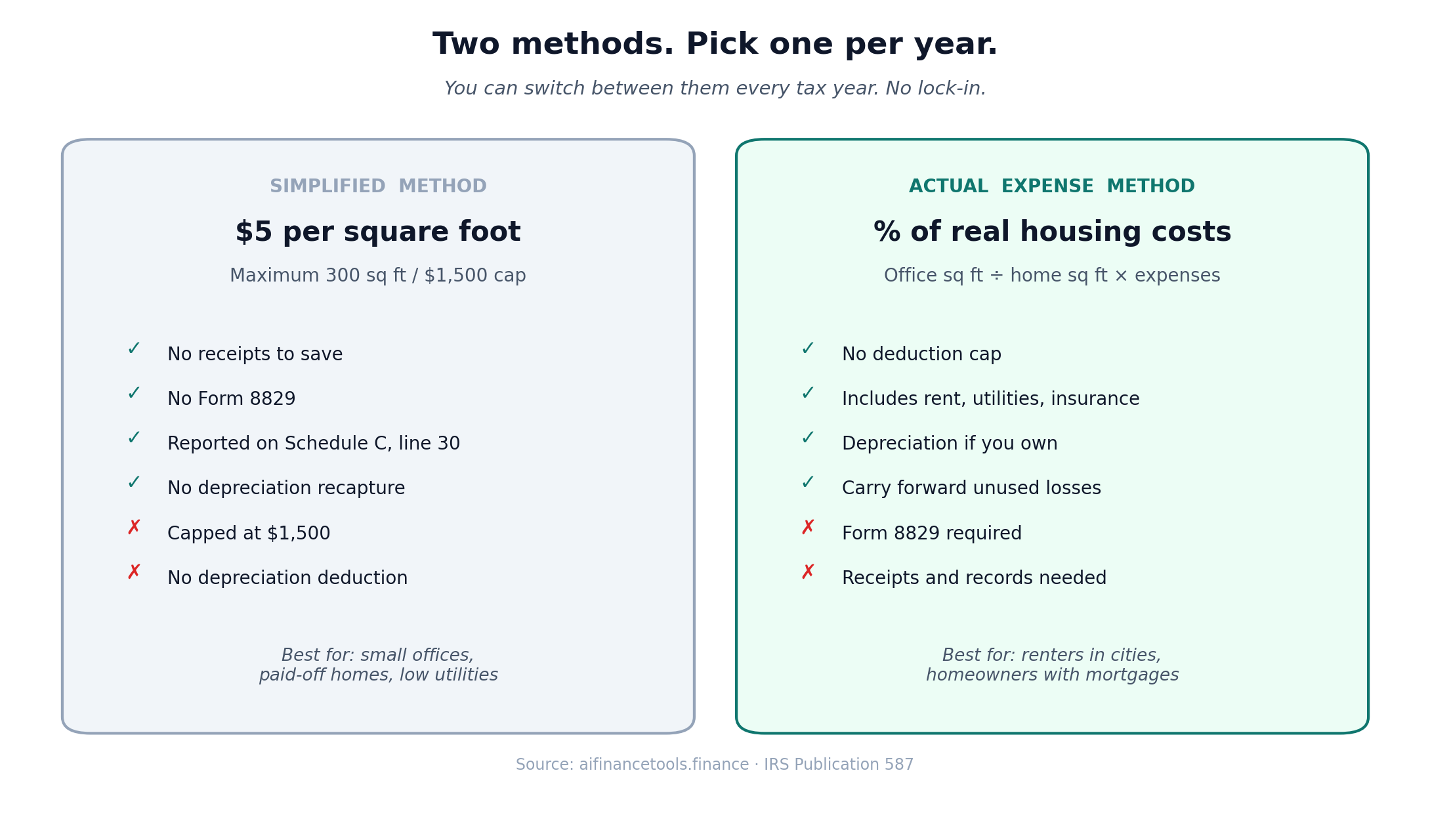

The two methods, side by side

The IRS gives you two ways to calculate the deduction. You can pick a different one each year. You just have to pick one method per year.

Method 1: Simplified method

You measure your office space in square feet. Multiply by $5. Stop at 300 square feet. The maximum deduction is $1,500.

If your office is 180 square feet, your deduction is $900. No receipts to save. No utility bills to dig out. You enter the square footage on your Schedule C and you’re done. No Form 8829 required.

The trade-off. It’s capped at $1,500, and you get no depreciation deduction.

Method 2: Actual expense method (regular method)

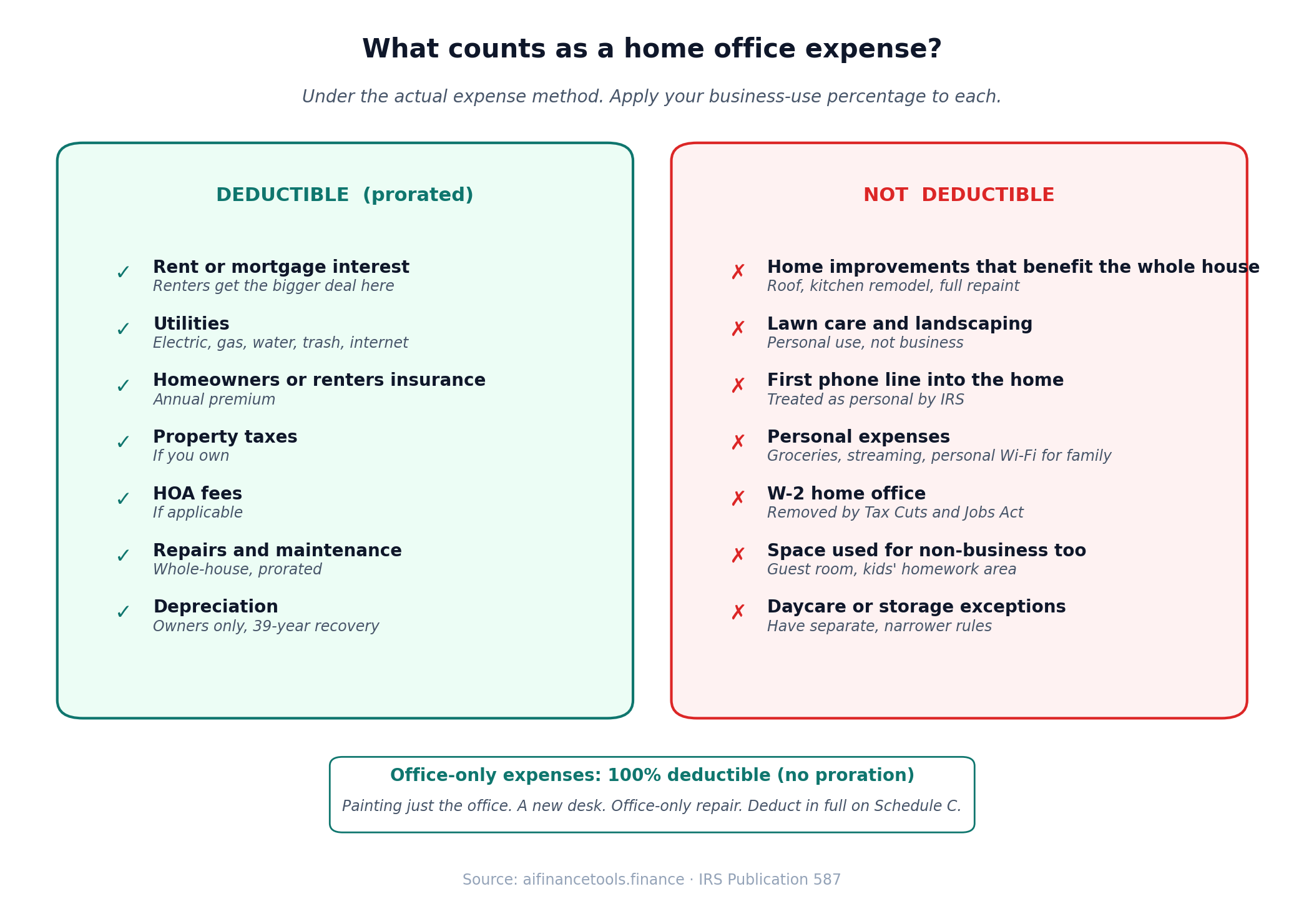

You calculate the percentage of your home used for business. Office square footage divided by total home square footage. You then apply that percentage to your housing costs for the year.

The deductible costs include:

- Rent or mortgage interest (renters get the bigger deal here, since the full rent flows in).

- Utilities, including electric, gas, water, trash, internet.

- Homeowners or renters insurance.

- Property taxes if you own.

- HOA fees if applicable.

- Repairs and maintenance on the whole house, prorated.

- Depreciation on the home itself if you own.

Direct office expenses, like painting just the office or buying a desk, get deducted at 100%. They don’t get prorated.

The actual method requires Form 8829 attached to your Schedule C, and it requires receipts. More work. Usually pays more.

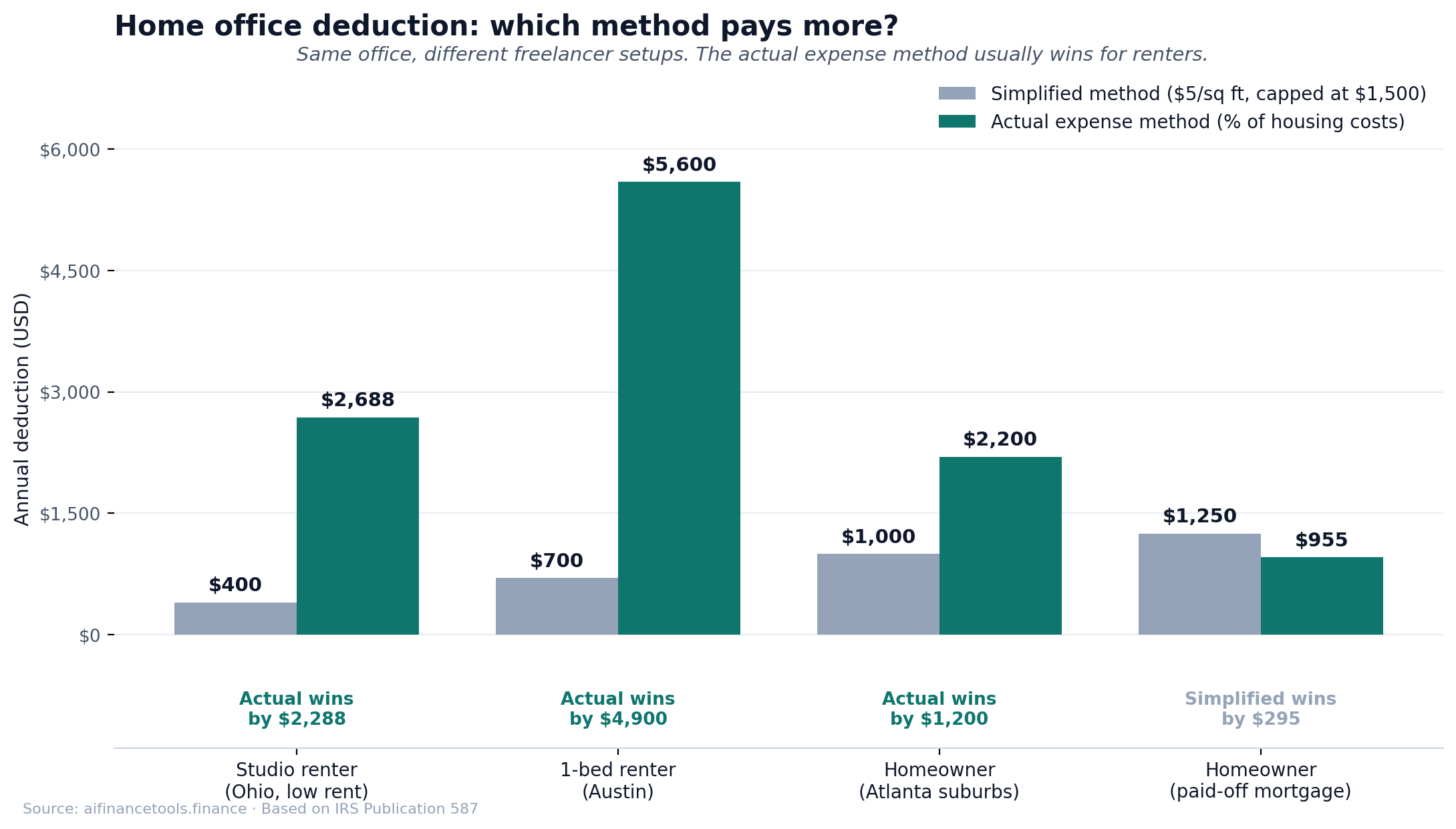

Real math: which method actually pays more for you

Run your own numbers in the worksheet →

This is where most articles wave their hands. Here’s the actual comparison at four real freelancer setups.

| Setup | Office sq ft | Home sq ft | Annual housing costs | Simplified ($5/sq ft) | Actual expense (% of housing) | Winner |

|---|---|---|---|---|---|---|

| Studio renter, low rent (Ohio) | 80 | 500 | $14,400 ($1,200/mo) + $2,400 utilities | $400 | $2,688 (16% of $16,800) | Actual, by $2,288 |

| 1-bed renter (Austin) | 140 | 800 | $28,800 ($2,400/mo) + $3,200 utilities | $700 | $5,600 (17.5% of $32,000) | Actual, by $4,900 |

| Homeowner, suburban (Atlanta) | 200 | 2,000 | $22,000 (mortgage interest, taxes, utilities, insurance) | $1,000 | $2,200 (10%) | Actual, by $1,200 |

| Homeowner, paid-off mortgage | 250 | 2,200 | $8,400 (taxes, utilities, insurance only) | $1,250 | $955 (11.4%) | Simplified, by $295 |

The pattern is clear. Rent in any city with reasonable rent, and the actual expense method beats the simplified method by a wide margin. Own a home with a paid-off mortgage and low utilities, and the simplified method might pull ahead. Barely.

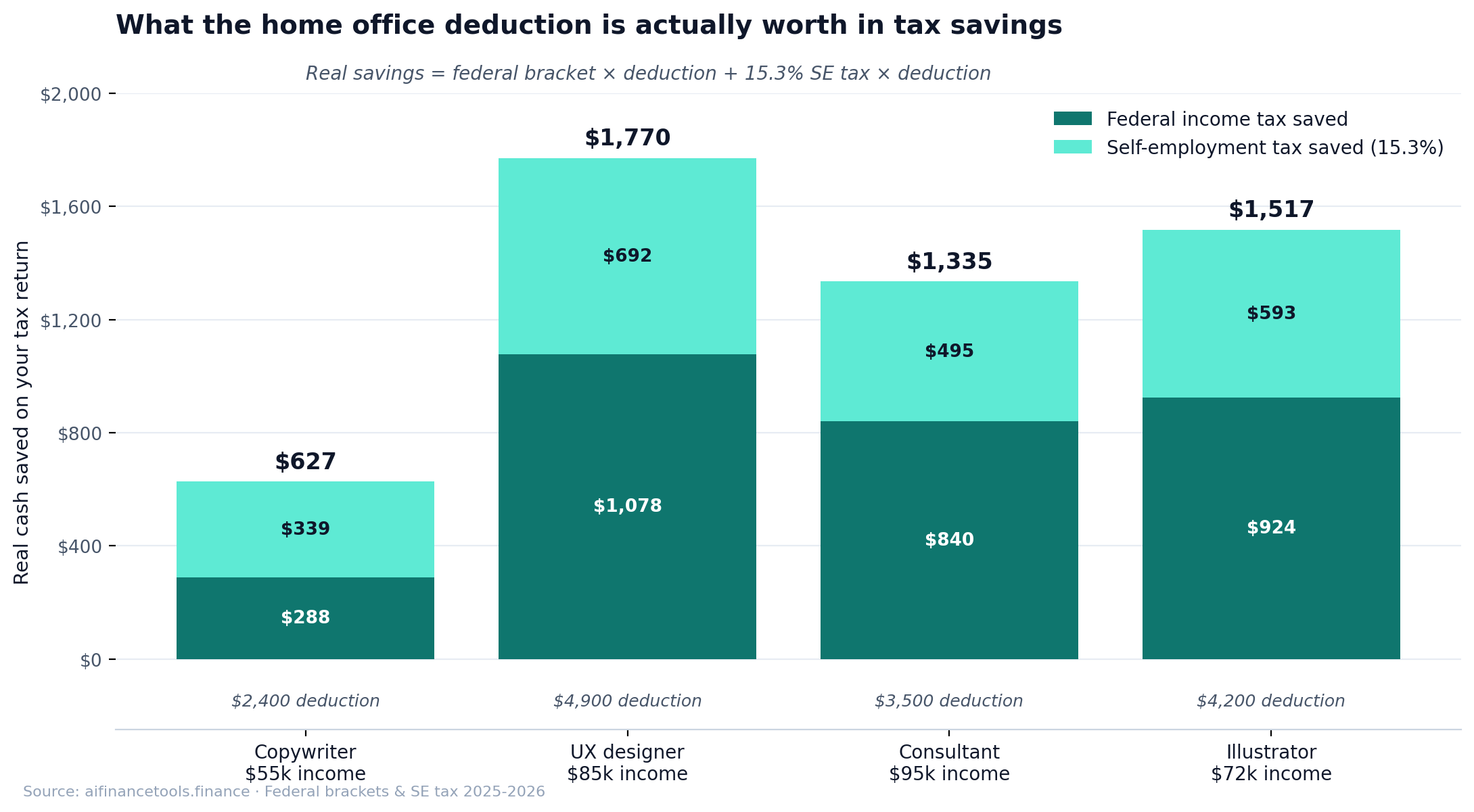

A freelance UX designer making $85,000 a year, renting a one-bedroom in a city, in the 22% federal bracket plus 15.3% self-employment tax. That $4,900 difference is worth roughly $1,830 in real tax savings. Walking past that to avoid paperwork is expensive.

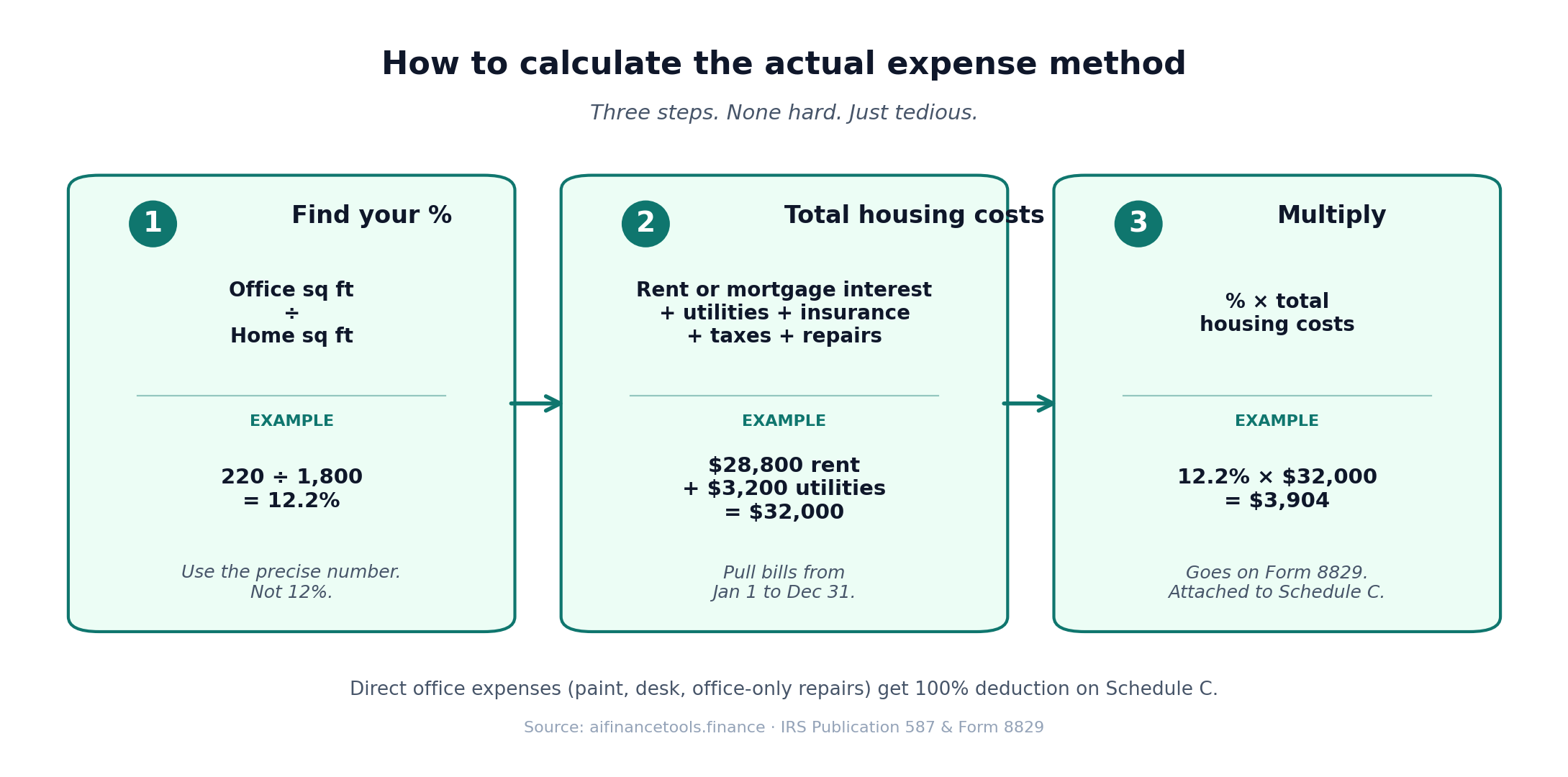

How to actually calculate the actual expense method

The math has three steps. None of them are hard. They are just tedious.

Step 1: Calculate your business-use percentage

Measure your office space. Then measure your total home square footage. Divide.

For example: a 220 sq ft office in a 1,800 sq ft apartment. 220 ÷ 1,800 = 12.2%. That’s your business-use percentage.

Round-numbered percentages like 10% or 25% draw more scrutiny than precise ones. If your math comes out to 12.2%, use 12.2%, not 12%.

Step 2: Total your home expenses for the year

Pull together one year of:

- Rent paid (or mortgage interest from your Form 1098).

- Property taxes if you own.

- Homeowners or renters insurance premiums.

- All utility bills: electric, gas, water, sewer, trash, internet.

- HOA fees.

- Repairs and maintenance to the whole home.

If you own, depreciation comes into play. The IRS uses a formula in Publication 587 based on the cost basis of your home and a 39-year recovery period for the business portion. This is where most homeowners hand it off to a CPA, and that’s fair. Getting depreciation wrong on a home is the kind of thing that shows up later when you sell.

Step 3: Apply your percentage

Multiply your total home expenses by your business-use percentage. That number goes on Form 8829.

Direct expenses just for the office (a paint job, a new desk, an office-only repair) get deducted in full as business expenses, separately on your Schedule C. Don’t double-count them.

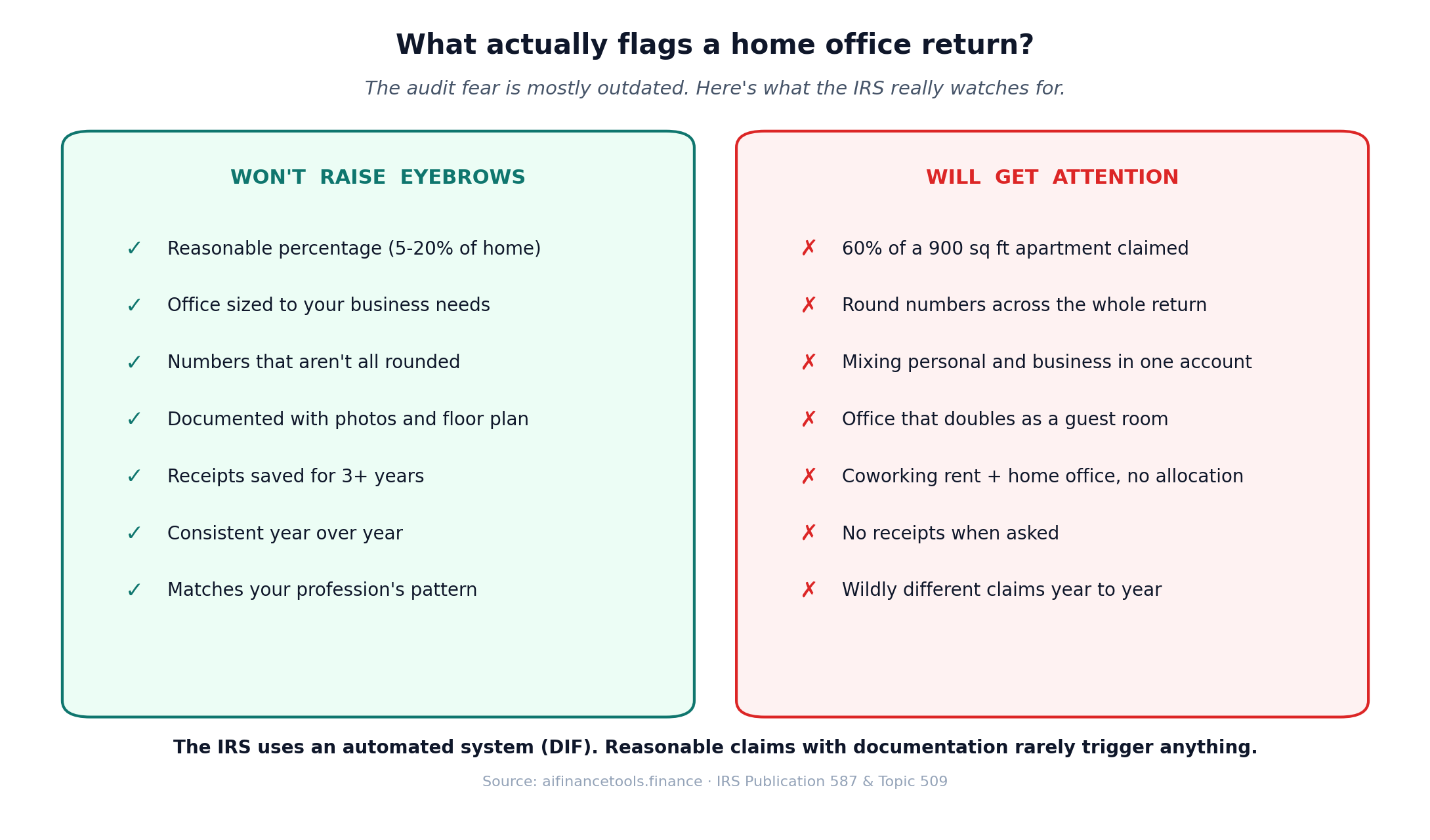

The audit risk question (and why it’s mostly overblown)

The “home office deduction triggers audits” idea is a holdover from the 1990s. It isn’t accurate now.

The IRS uses an automated system called the Discriminant Inventory Function (DIF) to compare your return to others in your profession. A freelance copywriter making $70,000 a year claiming a home office fits the pattern. The system doesn’t care.

What actually flags returns:

- Disproportionate claims. Saying 60% of your 900 sq ft apartment is your office. The IRS knows you have to sleep somewhere.

- Round numbers everywhere. $5,000 in utilities, $2,000 in repairs, $1,500 in insurance. Real numbers are messy.

- Mixing personal and business expenses all year and trying to clean it up at tax time. This is also why a separate business bank account matters from day one.

- Claiming a home office while also deducting commercial office rent with no clear allocation between them.

Freelancers on Reddit’s r/tax often share that they’ve claimed home office deductions for years with no issue. The pattern in those threads. People who lose audits on home offices either failed the exclusive-use test (the office doubled as a guest room) or had no documentation at all. Reasonable claims with reasonable documentation almost never get challenged.

If you want a deeper look at how to keep your books clean year-round so an audit is a non-event, our guide to tracking business expenses as a freelancer walks through the system.

Documentation that actually protects you

If the IRS ever asks, you want four things ready in 10 minutes.

- A floor plan or sketch of your home with the office area measured and marked. Hand-drawn is fine. Date it.

- Photos of the office showing it’s a real workspace, not a corner of the living room. Take them every January.

- A folder of receipts and bills for every home expense you’re claiming. Cloud storage is fine. Keep them for at least three years after filing, six if you want to be cautious.

- A simple log of business activity in that space. Calendar entries, client invoices, project files showing the work happens at your desk.

You don’t need a fancy system. A folder on Google Drive labeled “2026 Home Office” with five subfolders works fine. Most freelancers who get caught off-guard by an audit are the ones who improvise documentation after the fact.

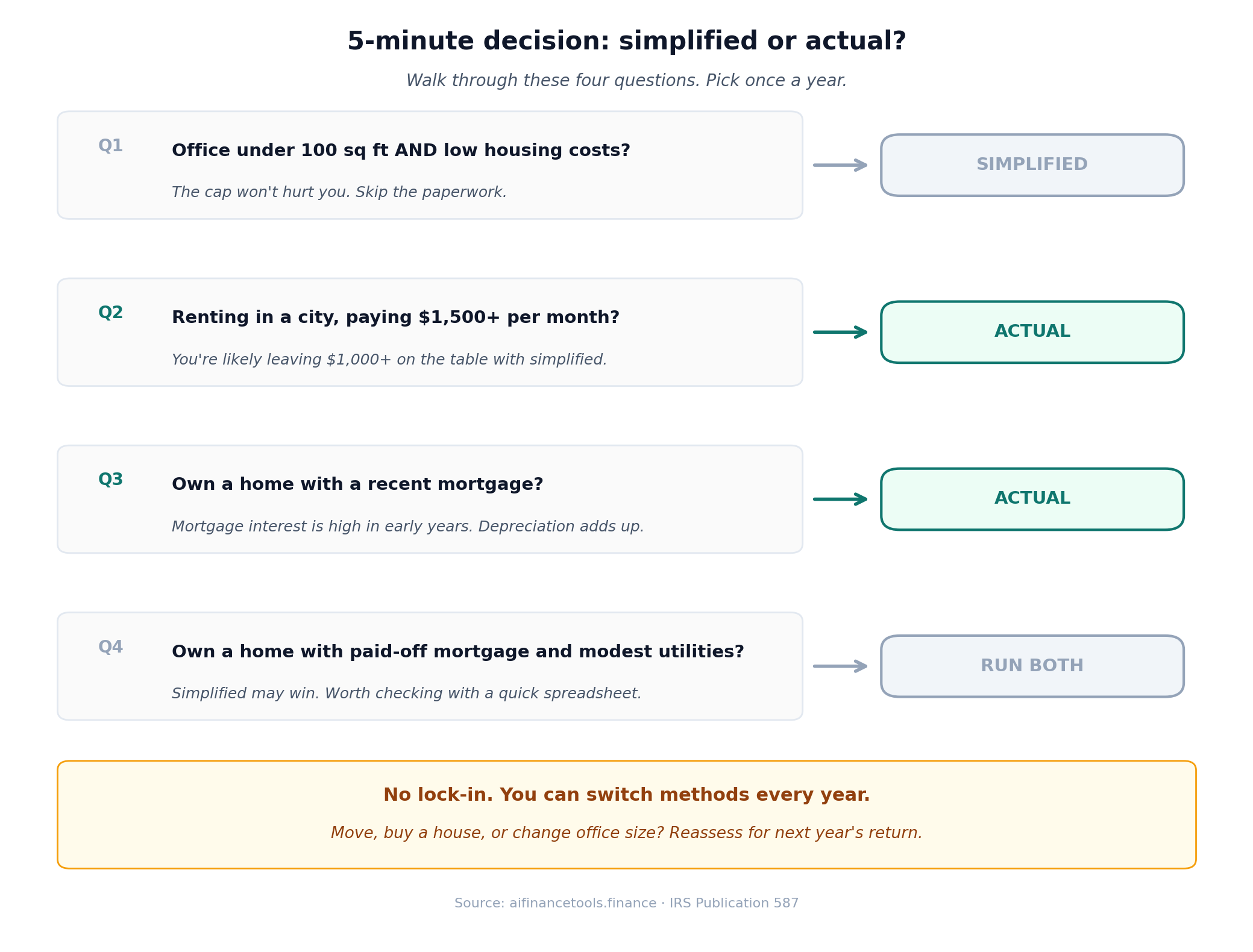

The 5-minute decision framework

Here’s the quickest way to decide which method to use this year. Sit down, run these four questions, decide.

- 1. Is your office under 100 sq ft and your housing costs low? Use the simplified method. The cap won’t hurt you, and the paperwork savings is real.

- 2. Do you rent in a city where rent is over $1,500/month? Run the actual expense method. You’re likely leaving $1,000+ on the table with the simplified method.

- 3. Do you own a home with a recent mortgage? Run actual. Mortgage interest in the early years is high, depreciation adds up, and the difference is meaningful.

- 4. Do you own a home with a paid-off mortgage and modest utilities? Run both. The simplified method may win, especially if you don’t want to track receipts.

The IRS lets you switch between methods every year with no lock-in. If your situation changes (you move, you buy a house, your office shrinks), reassess.

Common mistakes that cost freelancers money

The “guest room office” problem

Your office can’t double as where your in-laws sleep at Christmas. Exclusive use means exclusive. If the room genuinely doubles as something else, you can’t claim the full square footage.

The fix. Claim only the portion that is exclusive. If 70% of a 200 sq ft room is your dedicated office and the other 30% holds a futon for occasional guests, claim 140 sq ft. The math still helps, and you stay defensible.

Not claiming because you “might move”

You can claim a partial year. The IRS calculates an average monthly allowable square footage for situations where you started using the office mid-year, moved, or changed the size. Set up a 200 sq ft office in May and use it through December, and your average for the year works out to roughly 133 sq ft.

Forgetting depreciation recapture if you own

If you use the actual expense method and claim depreciation, the IRS will recapture that depreciation when you sell the home. You’ll pay tax on it at up to 25%. This isn’t a reason to skip the deduction. It’s a reason to know the trade-off and plan for it.

The simplified method has no depreciation recapture, which is one of its quiet advantages for homeowners.

Mixing the deduction with quarterly tax planning

Your home office deduction lowers your net Schedule C income. That lowers your self-employment tax and your federal income tax. It also lowers what you owe in quarterly estimated taxes through the year. Skip adjusting your quarterlies for deductions you plan to take, and you’re overpaying every three months.

Our guide on how to file quarterly estimated taxes as a freelancer covers the math for adjusting payments based on expected deductions, including this one.

How this fits with the rest of your Schedule C

The home office deduction is one line on a much longer return. A freelance illustrator making $72,000 with a real home office is probably also writing off:

- Software subscriptions: Adobe Creative Cloud, Procreate, Notion, accounting tools.

- Professional development: courses, books, conferences.

- Health insurance premiums if self-employed and not eligible for a spouse’s plan.

- Business meals at 50%.

- Mileage for business driving.

- Retirement contributions through a SEP IRA or Solo 401k.

The home office deduction is rarely the biggest line. It’s one of the most consistent. For a deeper line-by-line walk-through of the form everything goes on, see our Schedule C guide for freelancers.

Still on the fence about whether to stay sole prop or restructure as an LLC or S-Corp? The home office rules change a bit for S-Corp owners. They use an “accountable plan” through the corporation rather than a Schedule C deduction. Our breakdown of sole prop vs LLC vs S-Corp covers when that switch makes sense.

Tools that handle the home office calculation for you

If you don’t want to do this in a spreadsheet, a few tools track home office expenses through the year and run both calculations at tax time.

- Keeper Tax categorizes expenses, including home utilities, and asks you about your home office during onboarding. We covered the strengths and limits in our Keeper Tax review.

- FlyFin uses AI to scan your transactions and flag deductible expenses. Our FlyFin review goes through what it does well and where it falls short for freelancers.

- QuickBooks Solopreneur (the replacement for QuickBooks Self-Employed) tracks expenses and connects to TurboTax. The home office calculation is manual, but the categorization is solid.

- FreshBooks and Xero handle the bookkeeping but don’t specifically guide the home office deduction. You apply the percentage at tax time.

For a broader look at what works for solo operators, see our best accounting software for freelancers guide.

Get the home office deduction worksheet

I built a free worksheet that runs both methods side by side. Enter your office square footage, total home square footage, and annual housing costs. It tells you which method pays more, what the deduction is worth in real tax savings at your bracket, and what documentation to keep. Four tabs: Calculator, Documentation Checklist, What Counts, and Notes & Rules.

Drop your email and I’ll send it, plus a 5-day mini-course on freelancer tax savings.

Don’t want to share your email? Open the worksheet directly in Google Sheets →

Prefer Excel? Download the .xlsx version.

Frequently Asked Questions

Can I claim a home office if I rent?

Yes. Renters often benefit more than owners. Your full rent flows into the actual expense calculation, and rent is usually a freelancer’s largest housing cost. A renter paying $2,400 a month with a 12% business-use percentage deducts $3,456 just from rent, before utilities. The IRS doesn’t care whether you own or rent.

Does my home office have to be a separate room?

No. The IRS allows a clearly identifiable area, even within a larger room. A 60 sq ft corner of your living room with a dedicated desk, chair, and shelves can qualify, as long as that specific area is used only for business. Tape on the floor sounds silly but works as proof. A photo showing the dedicated setup helps.

What if I work from coffee shops half the time?

You can still claim the deduction as long as your home is your principal place of business. The IRS looks at where you do your administrative work: invoicing, planning, calls, project management. If those happen at home, your home office qualifies even if you do creative work at cafes. Document the home-based admin time and you’re fine.

Can I claim a home office and a coworking membership at the same time?

Yes, both can be deducted. The coworking fee goes on Schedule C as a regular business expense. The home office goes through the simplified or actual method. You just need to be honest about the time split. Spend 80% of your work hours at WeWork and your home isn’t really your principal place of business. The home office claim gets shaky.

What happens to my home office deduction if I have a loss for the year?

The home office deduction can’t create or increase a business loss. Under the simplified method, the deduction is capped at your gross income from the business, and any unused amount is gone. Under the actual expense method, you can carry forward the unused deduction to next year. This makes the actual method better for freelancers in early years when business is still ramping up.

How does the home office deduction affect what I pay in self-employment tax?

It reduces it. The home office deduction lowers your net Schedule C profit. Self-employment tax (15.3%) is calculated on net profit. So if your home office deduction is $4,000, you save 15.3% of $4,000 in SE tax (about $612), plus your federal income tax savings on top. For a guide to estimating your full tax burden, see how much freelancers should set aside for taxes.

Do I have to use Form 8829?

Only if you use the actual expense method. The simplified method is reported directly on Schedule C, line 30, with the square footage entered on the form. Form 8829 is for the actual method, where you list out each home expense category, apply the business percentage, and total it up. Most tax software handles this for you if you answer the questions accurately.

Will claiming a home office get me audited?

Probably not. The IRS made the rule. Millions of freelancers claim it every year. What raises flags is the size of the claim relative to your home and income, round-numbered estimates, and inconsistencies between your home office claim and the rest of your return. A reasonable claim with documentation is low-risk. To keep your tax season calm overall, our piece on avoiding tax liability shock covers the broader habits that prevent unpleasant surprises.

One concrete action for this week

Measure your office space. Measure your home. Pull last month’s utility bills, your rent or mortgage statement, and your insurance policy. Run the numbers both ways using the worksheet above.

Most freelancers who run the home office deduction for freelancers calculation for the first time find a deduction worth $2,000 to $5,000 a year they weren’t claiming. At a 22% federal bracket plus 15.3% SE tax, that’s real money back in your account, every year you keep working from home.

For a fuller picture of what else you can write off this year, our list of tax deductions for freelancers walks through every line on Schedule C, including the ones most people miss.

Start Your Free Trial with Keeper

Tax laws change. The figures in this article reflect the 2025 and 2026 tax years and reference IRS Publication 587, Topic 509, and Revenue Procedure 2013-13. Verify current rules at IRS.gov before filing. This is informational content, not tax or legal advice. For complex situations, especially involving home depreciation, S-Corp accountable plans, or partial-year use, work with a qualified CPA.

About the author

Gareth is an entrepreneur based in Dubai and the founder of AI Finance Tools for Freelancers. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide is researched from real user reviews, official documentation, and expert sources.