The honest LLC vs S-Corp for freelancers guide: plain-English help to decide whether to stay a sole proprietor, form an LLC, or elect S-corp in 2026. Real numbers, real deadlines, real costs.

You set aside 25 percent for taxes. You owed 32 percent. Then you saw a Reddit thread claiming an S-corp election would have saved you $5,000. Now you have three browser tabs open. Your Secretary of State’s website. IRS Form 2553. A CPA’s calendar booking page asking $300 for a first call. You’re not sure what to do.

Most articles on this topic explain the differences between a sole proprietorship, an LLC, and an S-corp. You already know the differences. What you actually need is a number. The dollar amount where the math flips in your favor. The date you have to file by. The list of what each option will actually cost you in 2026.

That’s what this guide is. Numbers come from the IRS, the SSA’s October 2025 announcement, the One Big Beautiful Bill Act signed July 4, 2025, and current pricing from the payroll and tax-prep tools you would actually use. Nothing is rounded. Nothing is invented.

LLC vs S-Corp for freelancers: the three structures in 90 seconds

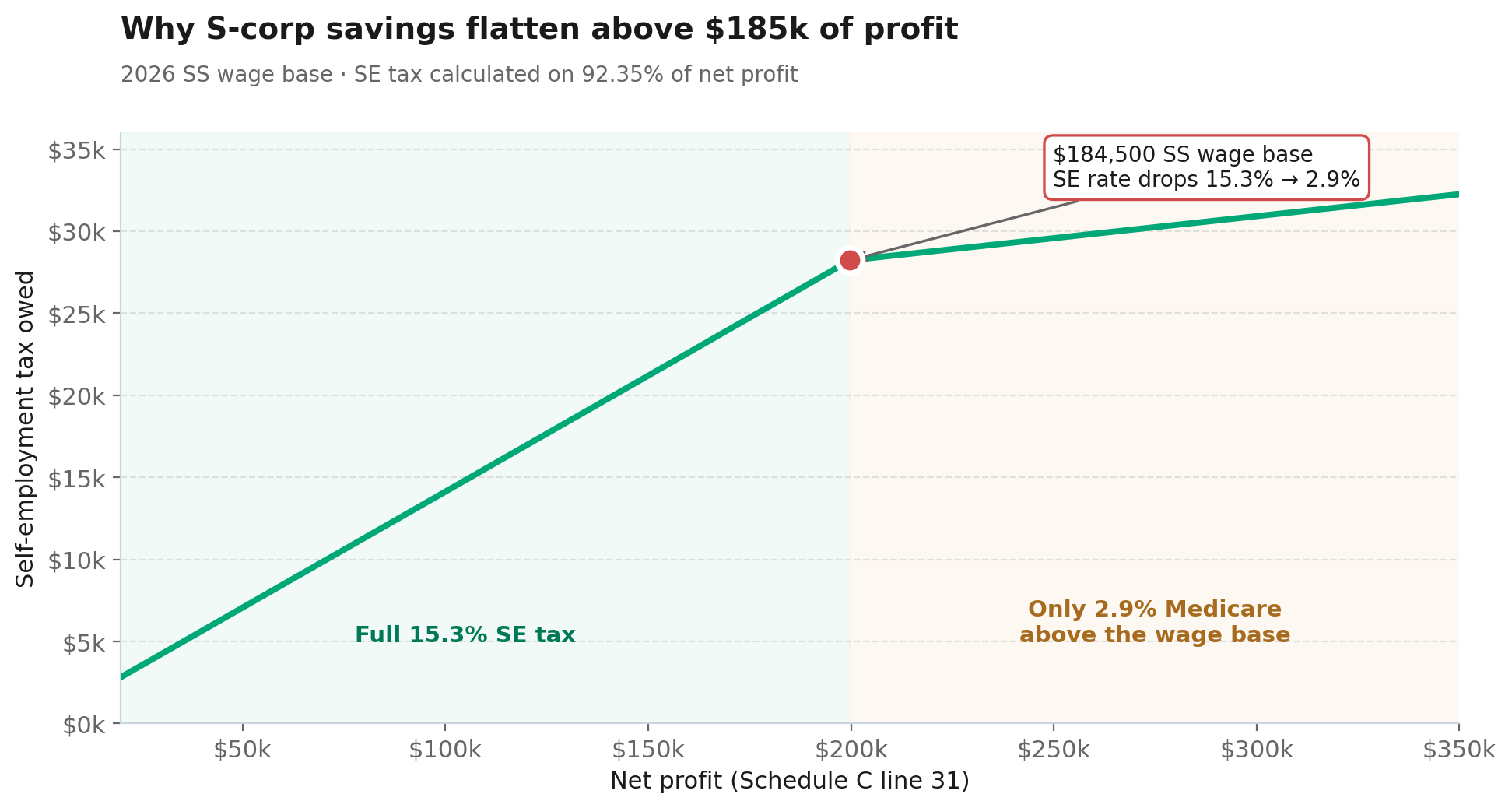

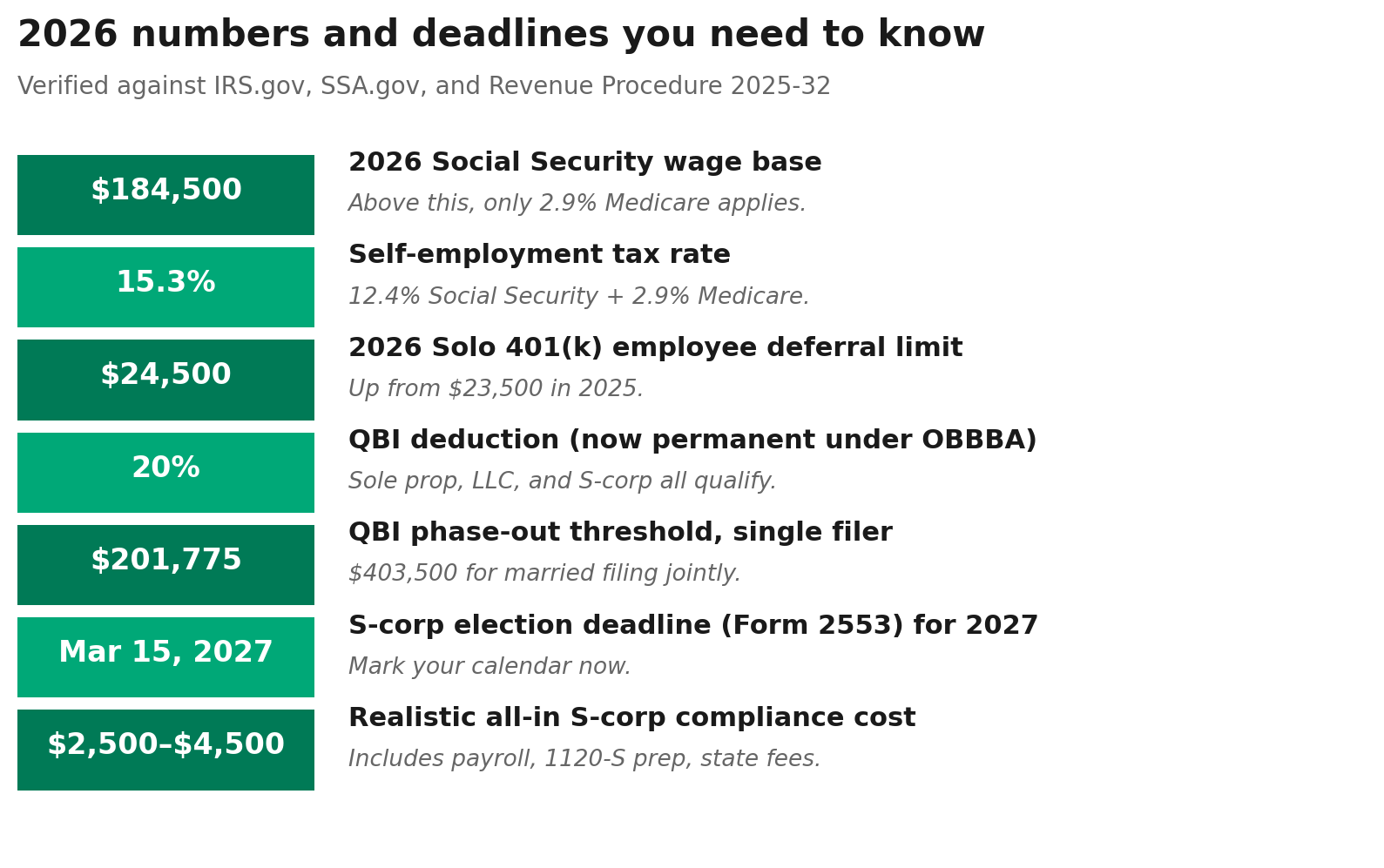

If you started freelancing without filing any state paperwork, you’re a sole proprietor. The IRS sees no difference between you and your business. You report income on Schedule C. You pay 15.3 percent self-employment tax on net profit up to $184,500 in 2026. After that, only the 2.9 percent Medicare portion continues.

An LLC is a state-level legal entity. You file with your Secretary of State and pay a fee somewhere between $50 in Kentucky and $500 in Massachusetts. Your personal assets now sit behind a legal wall. A single-member LLC is what the IRS calls a “disregarded entity,” which translates to: we tax you exactly the same as a sole proprietor. Same Schedule C. Same 15.3 percent self-employment tax.

An S-corp is not a separate legal entity. It’s a tax election you make with the IRS using Form 2553. Most freelancers who want S-corp treatment first form an LLC, then elect S-corp taxation on top of it. The LLC stays an LLC at the state level. The IRS just taxes it differently. You pay yourself a W-2 salary. The salary gets hit with 15.3 percent payroll tax. The rest comes out as a distribution that does not get hit with self-employment tax.

That gap, the part where the rest comes out as a distribution, is the entire point. Everything else flows from it.

“At what income should I switch from sole proprietor to LLC?”

This question gets asked on r/freelance and r/selfemployed every week. Most answers are wrong because they confuse two different decisions.

An LLC is not a tax decision. It’s a liability decision. So the right question isn’t “how much do I need to make.” The right question is: what could I lose if a client sued me, claimed I missed a deadline that cost them money, or argued my work damaged their business? If the answer is your house and your savings, form an LLC. If the answer is your $400 emergency fund, wait.

Three signs you’re ready to form an LLC:

- Your contracts are getting bigger. Once you sign anything over $5,000, especially with a corporate client, you’re exposed. A web developer in r/freelance described a $150,000 settlement after using a stock image without a license on a client’s site. He had no LLC, so the lien attached to his personal property.

- You have personal assets worth protecting. A home you own. Retirement accounts. Savings over $20,000. A car you actually paid off. These are what creditors come after when there’s no entity wall.

- A client is asking for your EIN, not your SSN. Larger clients often prefer paying entities. It also stops you from putting your Social Security number on every W-9 you send out.

What an LLC does not do: change your taxes by one cent. If anyone tells you forming an LLC will lower your tax bill, they’re confusing LLC formation with a separate S-corp election. The two are unrelated.

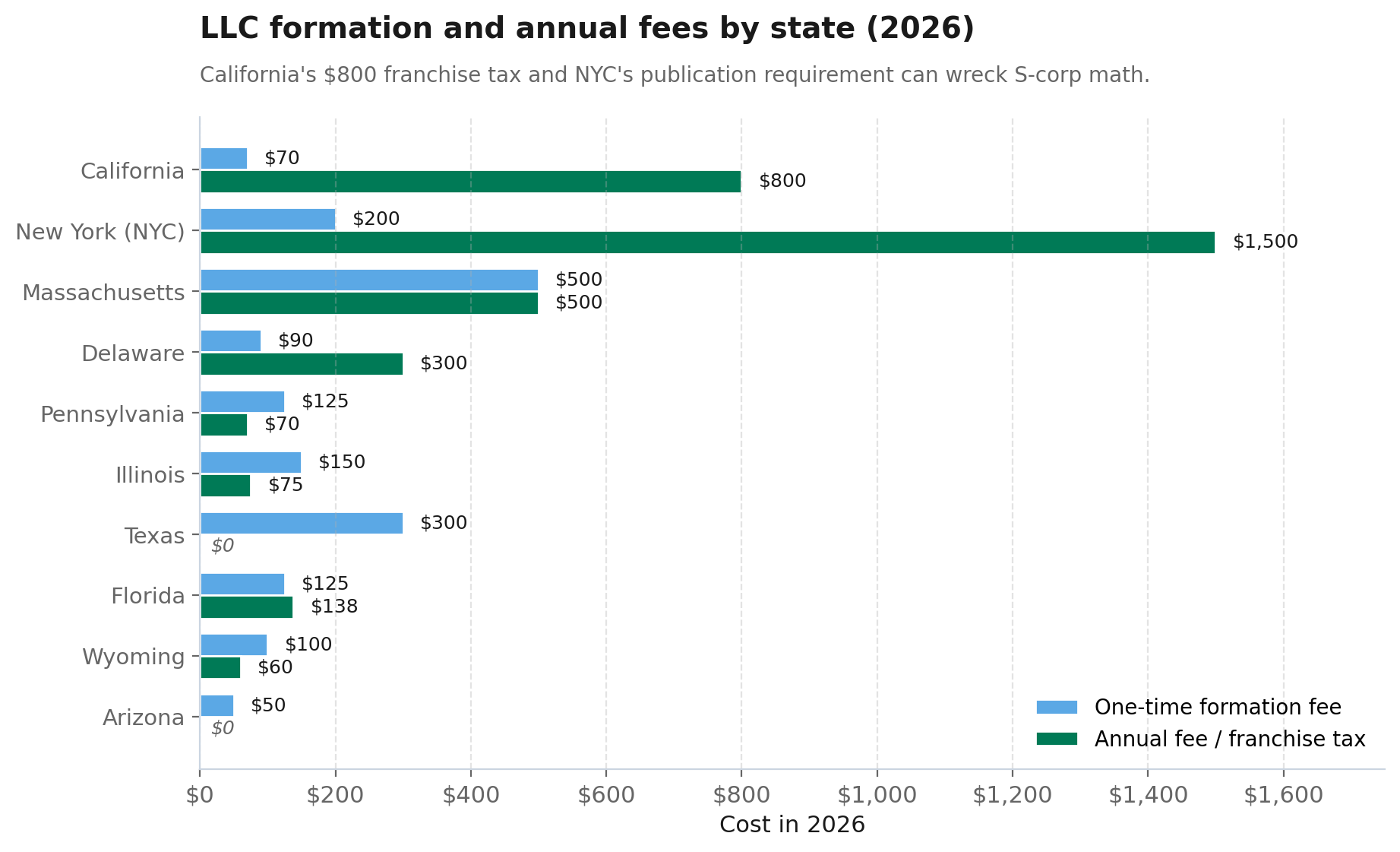

Cost in 2026: a single-member LLC runs $50 to $500 to form, plus annual reports of $0 in Arizona and Missouri up to $800 in California. Check your state’s Secretary of State website. The numbers vary wildly. California freelancers pay an $800 minimum franchise tax every year regardless of profit. Texas, Florida, and Wyoming charge nothing annually for a basic LLC.

“At what income does S-corp election actually save me money?”

This is the real question. The honest answer depends on three things: your net profit, your state’s payroll tax rules, and how much you’re willing to pay for compliance.

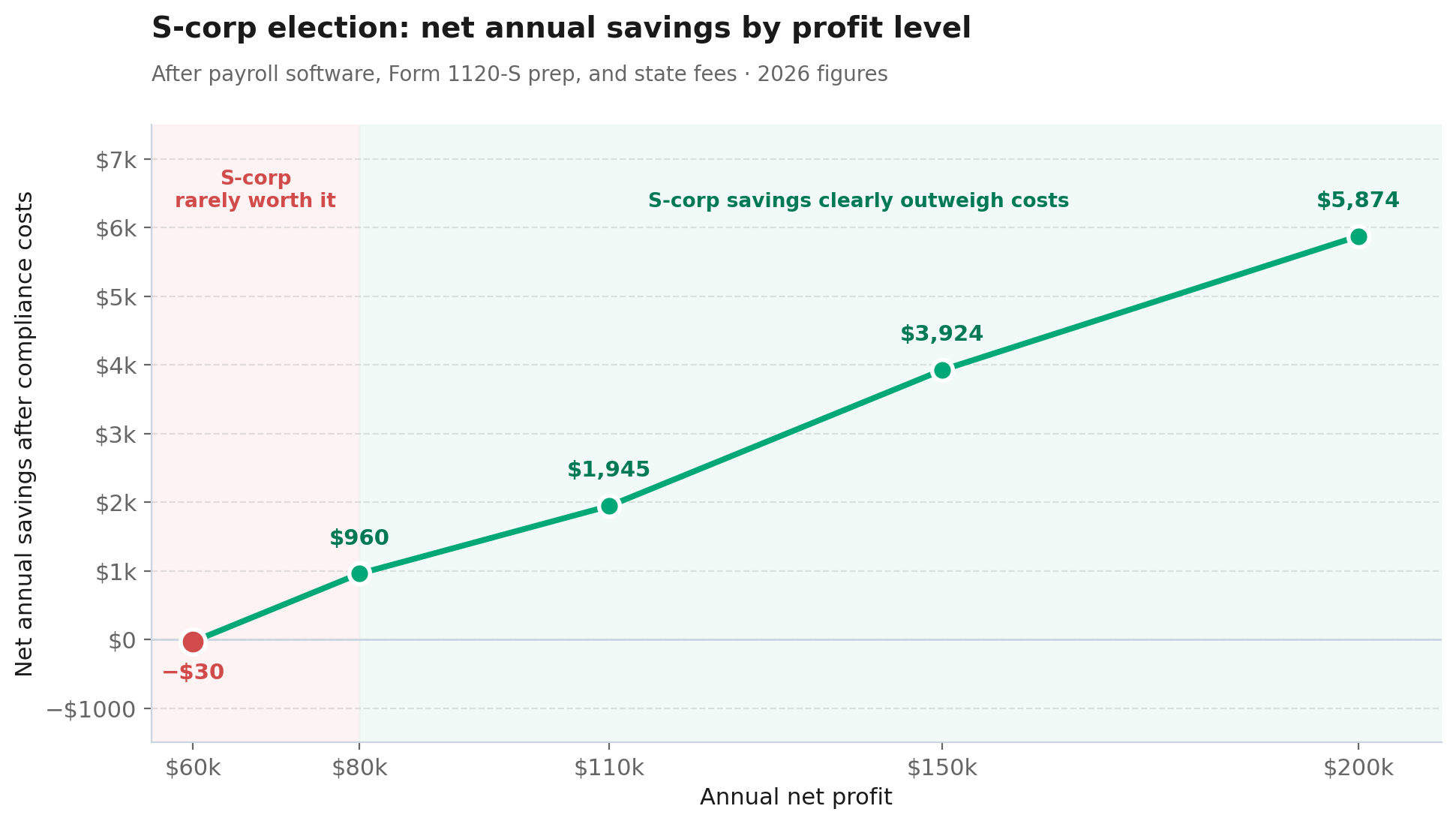

The CPA consensus, repeated across practitioner blogs and confirmed in client case studies, lands between $80,000 and $100,000 in net annual profit. Below $60,000, the math almost never works. Between $60,000 and $80,000, it depends. Above $80,000, the savings start to clearly outweigh the costs.

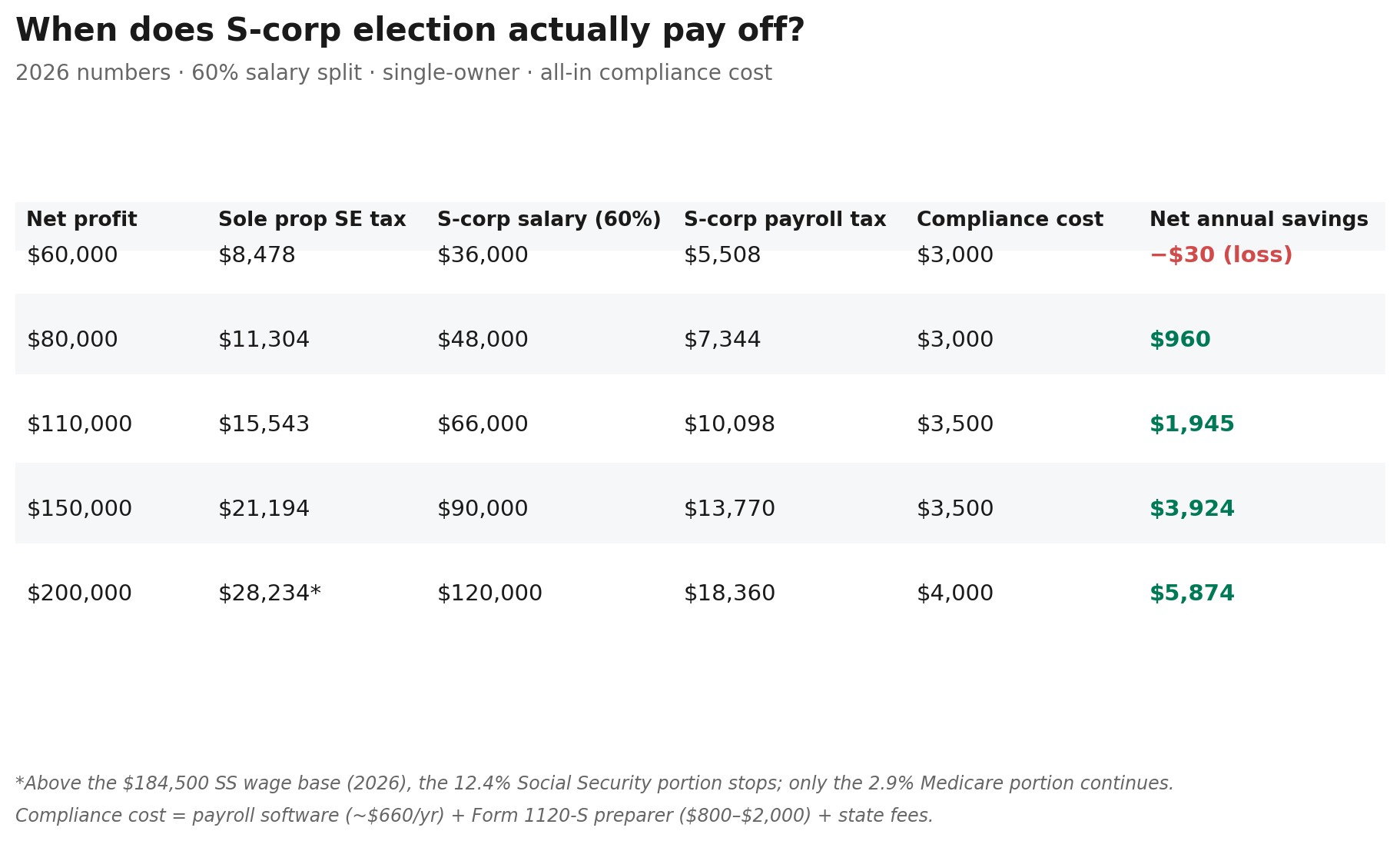

The break-even table for 2026

Here’s what most articles will not show you. The actual side-by-side at four common freelancer profit levels, using 2026 numbers, with a “reasonable salary” set at 60 percent of profit (a defensible middle-ground ratio that matches Bureau of Labor Statistics medians for most knowledge work).

| Net Profit | Sole Prop / LLC SE Tax | S-Corp Salary (60%) | S-Corp Payroll Tax | Annual Compliance Cost | Net Annual Savings |

|---|---|---|---|---|---|

| $60,000 | $8,478 | $36,000 | $5,508 | $3,000 | -$30 (lose money) |

| $80,000 | $11,304 | $48,000 | $7,344 | $3,000 | $960 |

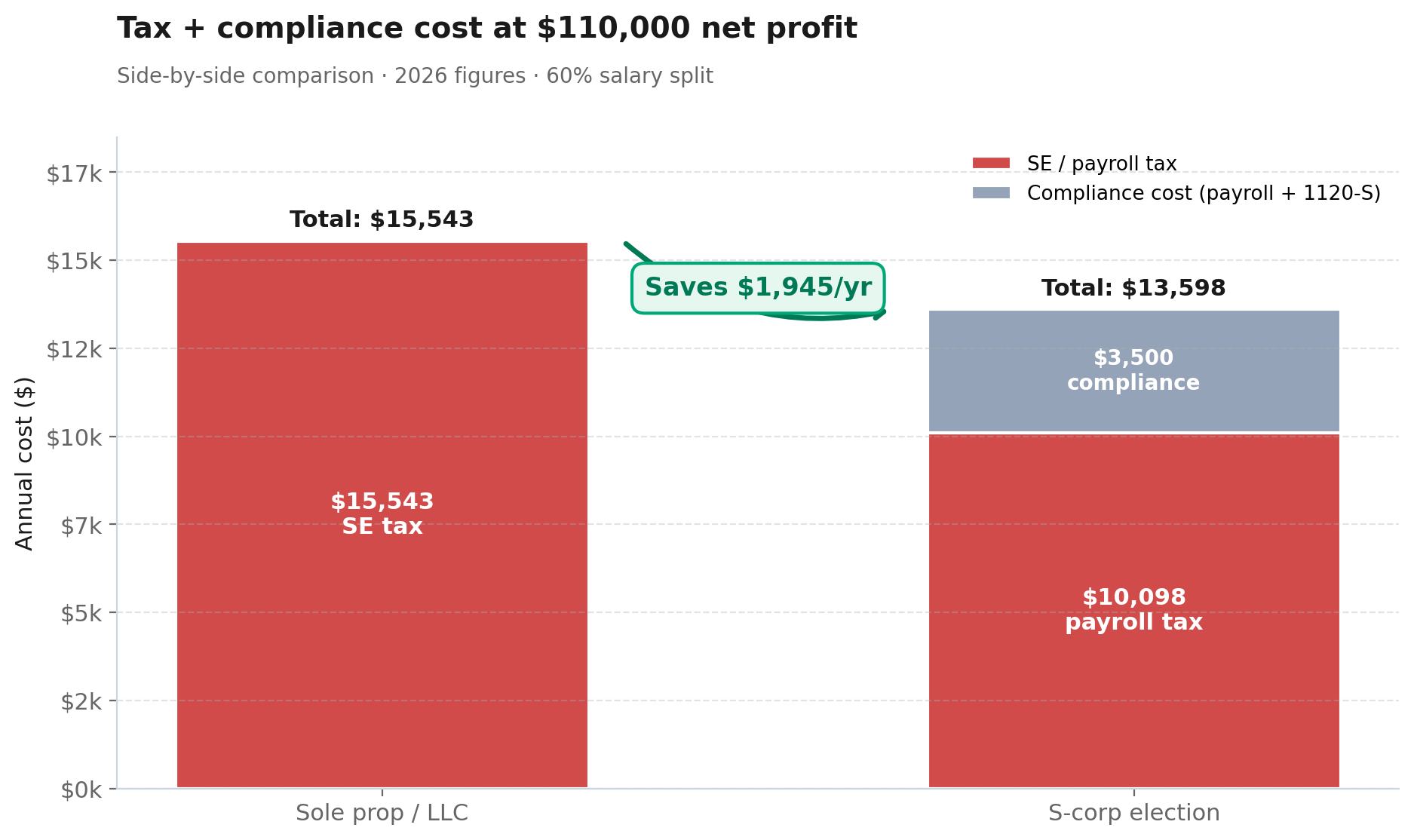

| $110,000 | $15,543 | $66,000 | $10,098 | $3,500 | $1,945 |

| $150,000 | $21,194 | $90,000 | $13,770 | $3,500 | $3,924 |

| $200,000 | $28,234* | $120,000 | $18,360 | $4,000 | $5,874 |

*Above the $184,500 SS wage base for 2026, the 12.4 percent Social Security portion stops. Only Medicare (2.9%) continues. Compliance cost includes payroll software (Gusto Simple at $49/month plus $6/employee, roughly $660/year as of March 2026) plus an 1120-S preparer ($800 to $2,000) plus state filing fees.

Look at how the asterisk works at $200,000. The 12.4 percent Social Security portion of self-employment tax stops at $184,500 of net SE income in 2026. Above that line, only the 2.9 percent Medicare portion continues. S-corp savings keep growing as profit grows, but the curve flattens. Going from $80k to $150k saves you about $3,000 more a year. Going from $150k to $200k adds another $1,950. Big wins early. Smaller wins later.

Real client examples shared by CPAs in interviews:

- A freelance designer netting $150,000. Saved roughly $8,000 a year after payroll and tax-prep costs.

- A consultant netting $90,000. Saved closer to $3,000 a year.

- A freelance technical writer netting $120,000. Set salary at $78,000 (the BLS median), distributed $42,000, saved roughly $5,000 a year.

One catch. All of this assumes your income is steady. If your profit swings from $40,000 one year to $130,000 the next, S-corp election can become a liability. You have to run payroll every month. That costs the same whether you billed $0 or $30,000 that month. Multiple CPAs interviewed by SelfEmployed.com flagged feast-and-famine income as the most common reason freelancers regret electing too early. If your cash flow is still unpredictable, fix that first before you add fixed payroll obligations on top.

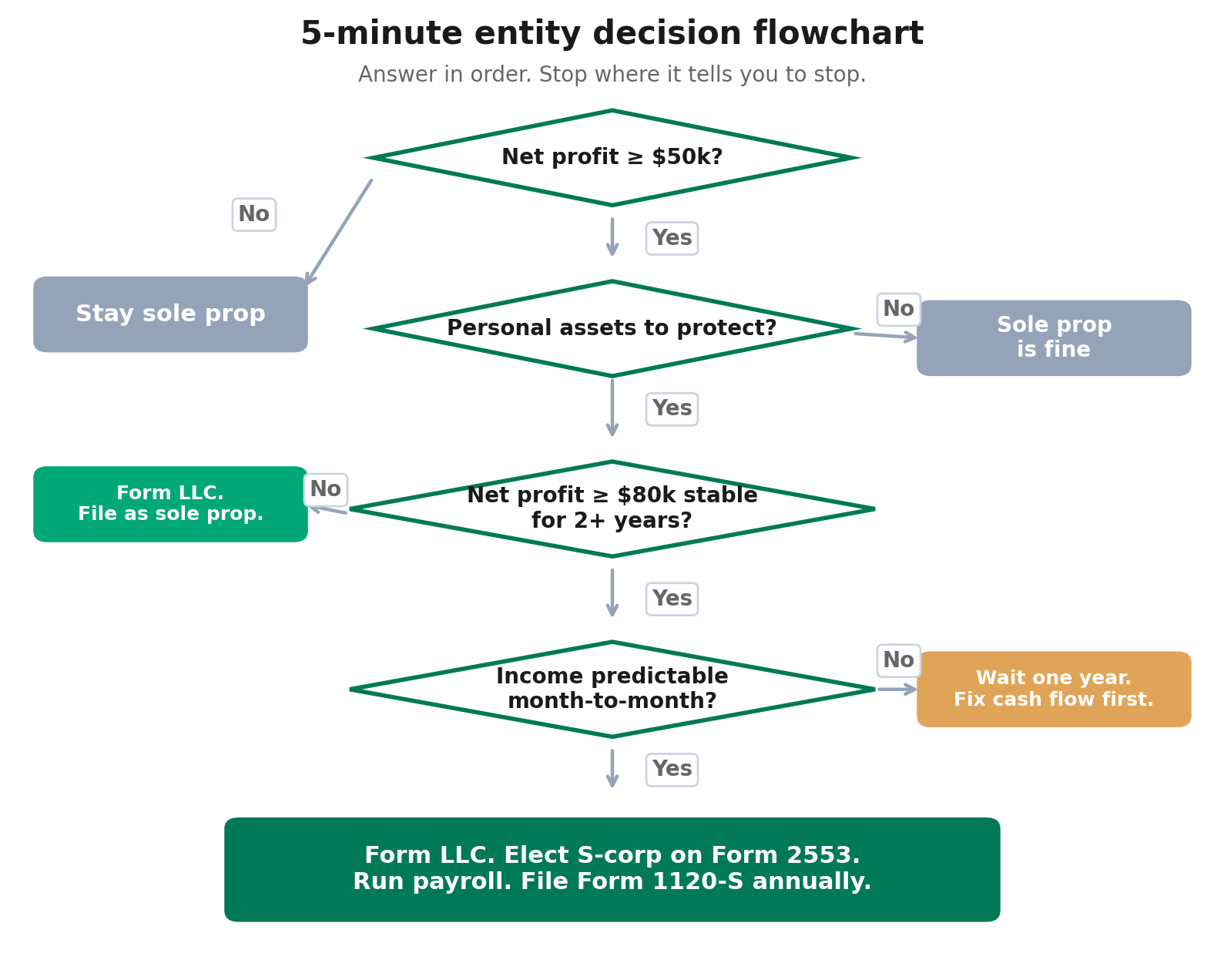

The 5-minute decision framework

Stop reading and answer five questions. Be honest with yourself.

- Last year’s net profit, after expenses, before tax. Write it down. If you haven’t finished your books for last year, finish your bookkeeping first. Guessing here will cost you money.

- The trend. Is this year tracking similar, higher, or lower? If you have less than two years of consistent income, default to staying simple.

- Your state. Look up your LLC formation cost and annual fee. Add California’s $800 franchise tax if you’re in California. Add New York’s publication requirement (about $1,500 in NYC) if you’re in New York.

- Your tolerance for admin. Running payroll twice a month, filing Form 941 quarterly, filing Form 1120-S annually, and keeping clean separate books is roughly 4 to 6 hours of monthly attention. Are you good for that, or will you fall behind and trigger penalties?

- Your CPA situation. Do you have one who works with S-corps and freelancers, or are you DIYing on TurboTax? Filing Form 1120-S yourself is technically possible but rarely a good idea. Budget $800 to $2,000 a year for an S-corp tax return.

Answer key:

- Profit under $50,000: Stay a sole proprietor. Maybe form an LLC if you have personal assets to protect. Skip the S-corp.

- Profit $50,000 to $80,000, stable: Form an LLC for liability protection. Continue filing as sole proprietor. Revisit S-corp next year if profit grows.

- Profit $80,000 to $200,000, stable, two-plus years running: Run the math on S-corp election. Savings probably justify the costs. Talk to a freelancer-savvy CPA before filing.

- Profit over $200,000: S-corp is almost always worth it. Savings on the Medicare portion alone, plus access to better retirement vehicles like the Solo 401(k), pay for the complexity.

- Volatile income at any level: Wait one more year. Confirm the income holds.

The mistake most freelancers make

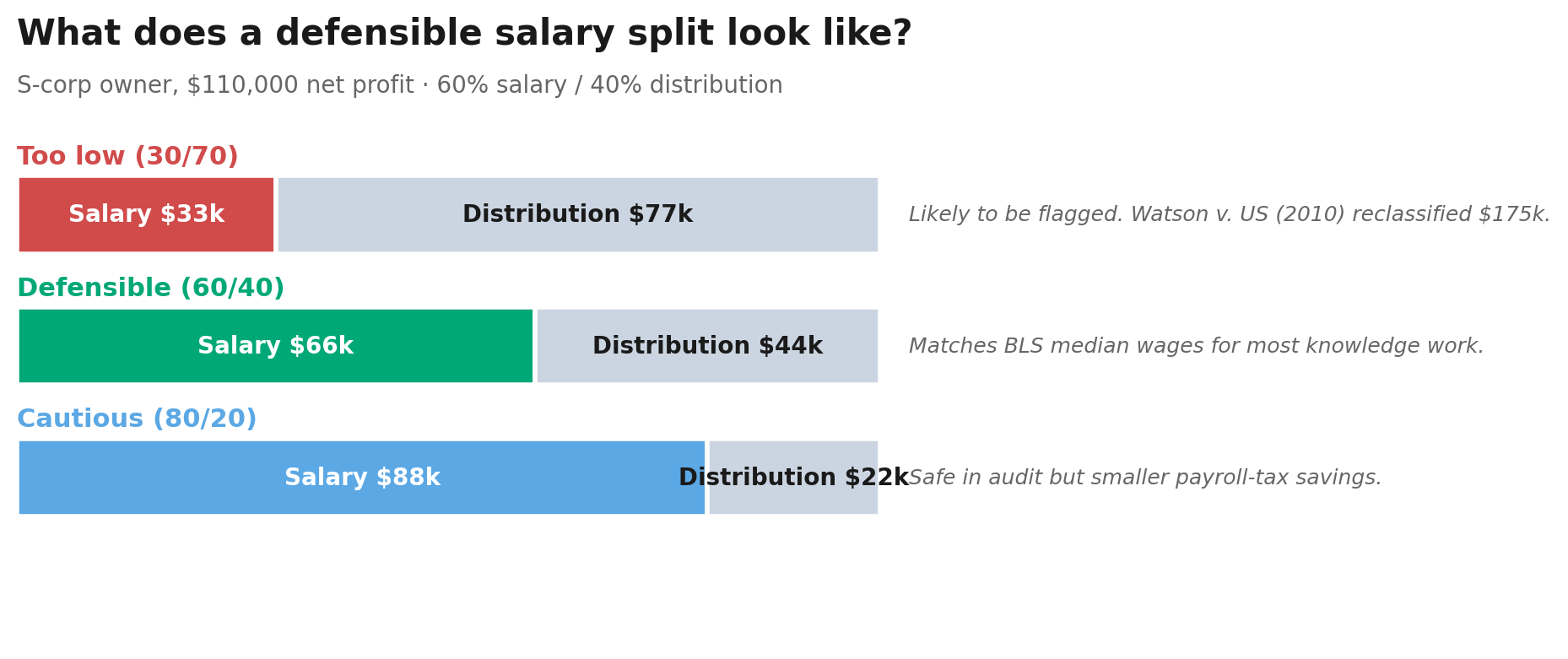

You see “S-corp saves me $5,000 a year” on a Reddit thread. You file Form 2553 in a hurry. You set your salary at $20,000 because you read somewhere it should be “low to maximize distributions.”

That’s how you end up in tax court.

The IRS requires “reasonable compensation” for S-corp owner-employees. There is no exact formula in the tax code. There is a body of case law. The most cited case is Watson v. United States (2010). A CPA in Iowa paid himself $24,000 in salary and $220,000 in distributions. The IRS reclassified $175,000 of his distributions as wages and assessed back payroll taxes plus penalties. He lost in district court. He lost on appeal.

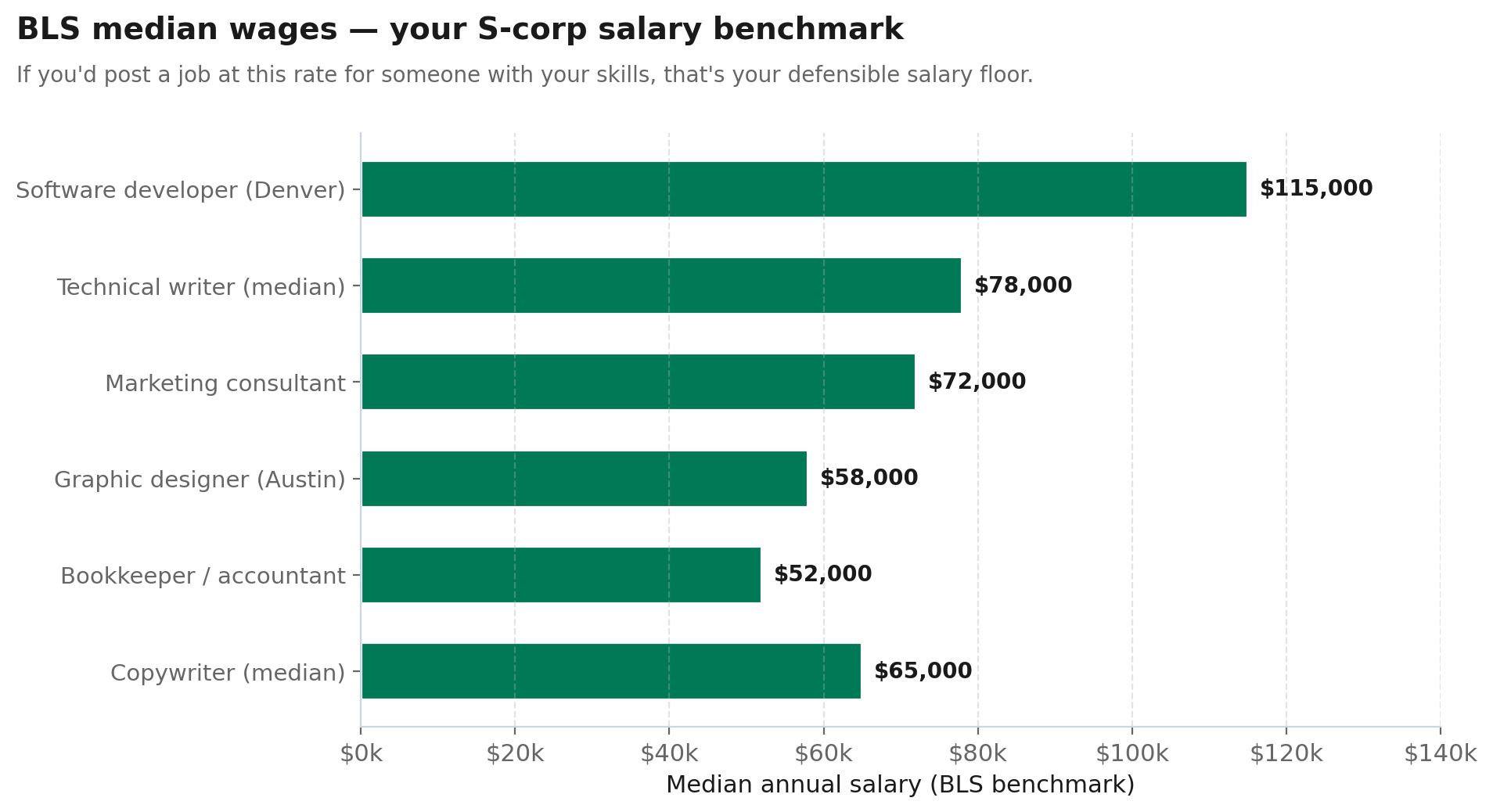

The standard the courts use is simple. What would you pay an employee to do the same work in your market? For a freelance graphic designer in Austin, the Bureau of Labor Statistics median is around $58,000. For a freelance software developer in Denver, it’s closer to $115,000. Your “reasonable salary” should look like a salary you would actually post on Indeed for someone with your skills. Splitting profit 60/40 (60 percent salary, 40 percent distribution) is defensible for most knowledge workers. Splitting 30/70 will get you flagged.

Practical implication: the lower your profit, the smaller your distribution can defensibly be, and the smaller your tax savings. This is another reason the S-corp math doesn’t work below $80,000. There’s no room to take a meaningful distribution after paying yourself a credible salary.

“What does the One Big Beautiful Bill change for me?”

The OBBBA was signed July 4, 2025. Two changes matter for this decision.

First, the 20 percent Qualified Business Income deduction (Section 199A) is now permanent. It was scheduled to expire at the end of 2025. Now it doesn’t. The deduction applies to sole proprietors, single-member LLC owners, and S-corp shareholders equally. So it doesn’t push you toward one structure over another. But it does mean you can’t use “the QBI deduction is going away” as a reason to rush into S-corp election. It’s staying. The QBI deduction sits on top of all your other freelance tax deductions, not in place of them.

Second, starting in 2026, there’s a new $400 minimum QBI deduction for anyone with at least $1,000 of qualified business income who materially participates in the business. The phase-out thresholds expanded too. $201,775 for single filers and $403,500 for married filing jointly in 2026, with the phase-out window stretching to $276,775 (single) and $553,500 (joint).

The QBI deduction interacts with S-corp election in a specific way. Your salary portion is W-2 wages, not QBI, so it doesn’t qualify for the deduction. Your distribution does. Setting your salary too low boosts the QBI base but invites IRS scrutiny. Setting it too high reduces the deduction. The optimal balance for most freelancers in service businesses (consulting, design, marketing, coaching) lands close to that 60/40 split. If you’re in one of the Specified Service Trade or Business categories (consulting, financial services, performing arts, athletics) and your income is climbing toward $200,000, talk to a CPA before the end of the year about salary planning.

“What’s the deadline for S-corp election in 2026?”

March 16, 2026 was the deadline to elect S-corp status retroactive to January 1, 2026. March 15 fell on a Sunday, so the IRS pushed it to the next business day. If you missed it, you have two options.

Option one: file Form 2553 now. Your election takes effect January 1, 2027. You operate as a sole proprietor or LLC for all of 2026 and pay full self-employment tax on this year’s profit.

Option two: late election relief under Revenue Procedure 2013-30. If you intended to elect S-corp from the start of the year, have a reasonable cause for the delay, and have been treating your books as if the election were already in place, you can file Form 2553 with “FILED PURSUANT TO REV. PROC. 2013-30” written across the top. The IRS grants this relief if you file within 3 years and 75 days of the intended effective date. It’s not automatic. You need a written reasonable cause statement.

For 2027 elections, the deadline will be March 15, 2027. Mark your calendar now if you’re anywhere near the threshold.

“What about state taxes when I elect S-corp?”

Most freelancer articles skip this part. It can wreck your math.

- California: $800 minimum franchise tax for LLCs and S-corps, plus a 1.5 percent S-corp tax on net income (with an $800 minimum). At $100,000 of profit, that’s $1,500 in state-level S-corp tax a sole proprietor would not pay.

- New York: Requires a separate New York S-corp election (Form CT-6). Without it, the IRS treats you as an S-corp federally and New York treats you as a C-corp at the state level. New York City also adds an Unincorporated Business Tax that may or may not apply depending on structure.

- New Jersey: Requires a separate state S-corp election and an annual S-corp report.

- Texas, Florida, Wyoming, Nevada, South Dakota, Washington, Tennessee: No state income tax, generally easier on S-corps. Texas charges a small franchise tax above $1.23 million in revenue, so most freelancers are exempt.

Before you file Form 2553, look up your state’s separate S-corp filing requirements. Doing the federal election without the state election can create a tax mismatch that costs you more than the savings.

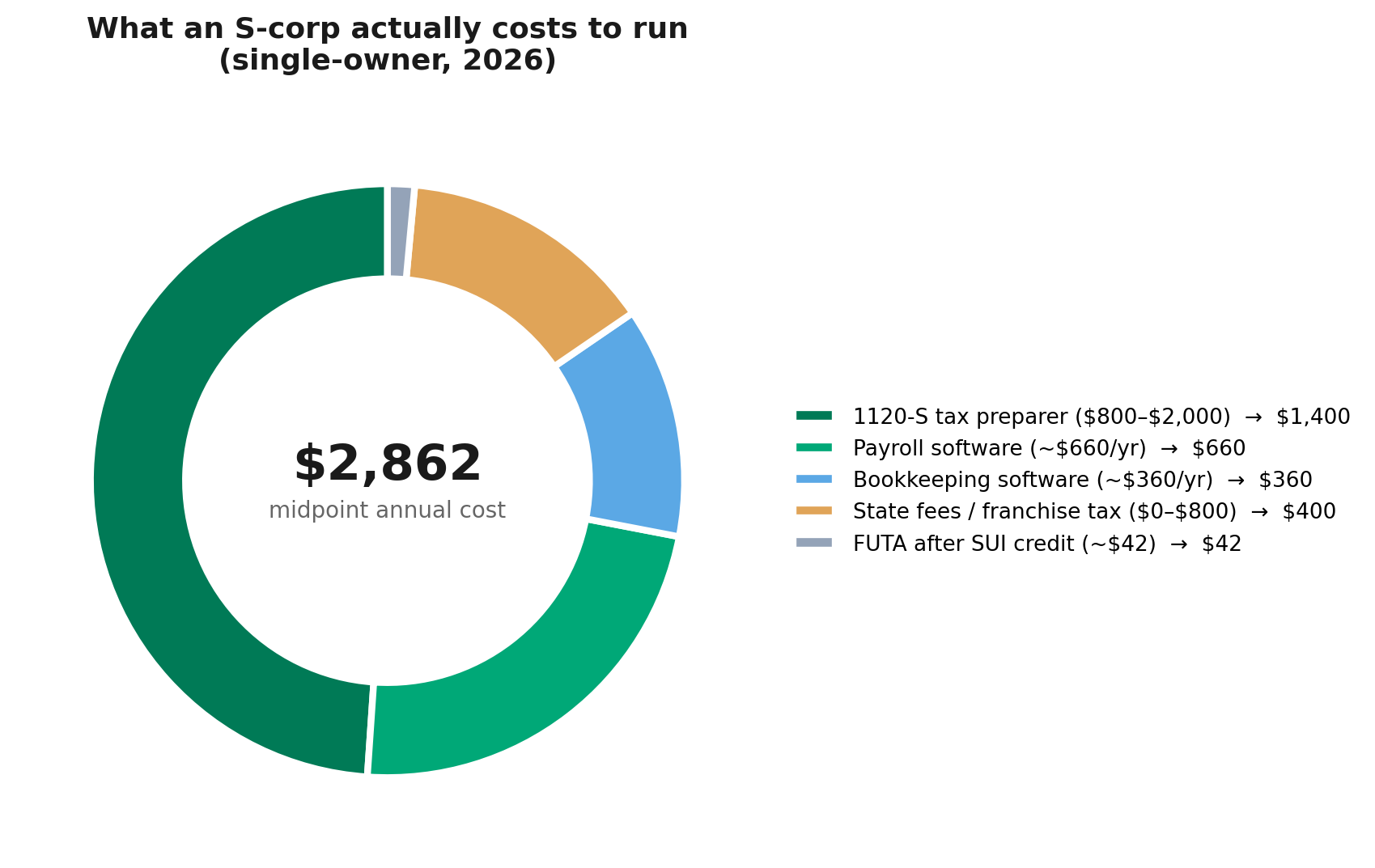

What an S-corp actually costs to run in 2026

Real numbers, current as of April 2026:

- Payroll software: Gusto Simple is $49 per month plus $6 per employee per month after the March 2026 price increase. For a single owner-employee, that works out to $660 a year. QuickBooks Payroll runs similar. Patriot Payroll is cheaper at around $20 base plus per-employee fees.

- S-corp tax return (Form 1120-S): $800 to $2,000 per year from a CPA. DIY is technically allowed but the form is complex enough that even Hsing Tseng, a freelance writer who documented her own S-corp election, said tax software is strongly advised.

- Bookkeeping: If you weren’t already keeping separate books, you have to start. DIY using accounting software works at $20 to $40 a month. A bookkeeper runs $200 to $500 a month.

- State fees: $0 to $800+ depending on state.

- Federal Unemployment (FUTA): 6 percent on the first $7,000 of wages per year (max $420), usually offset by state unemployment insurance credits.

Realistic all-in compliance budget for a single-owner S-corp in 2026: $2,500 to $4,500 per year. That’s the number you have to clear in tax savings before S-corp election makes sense.

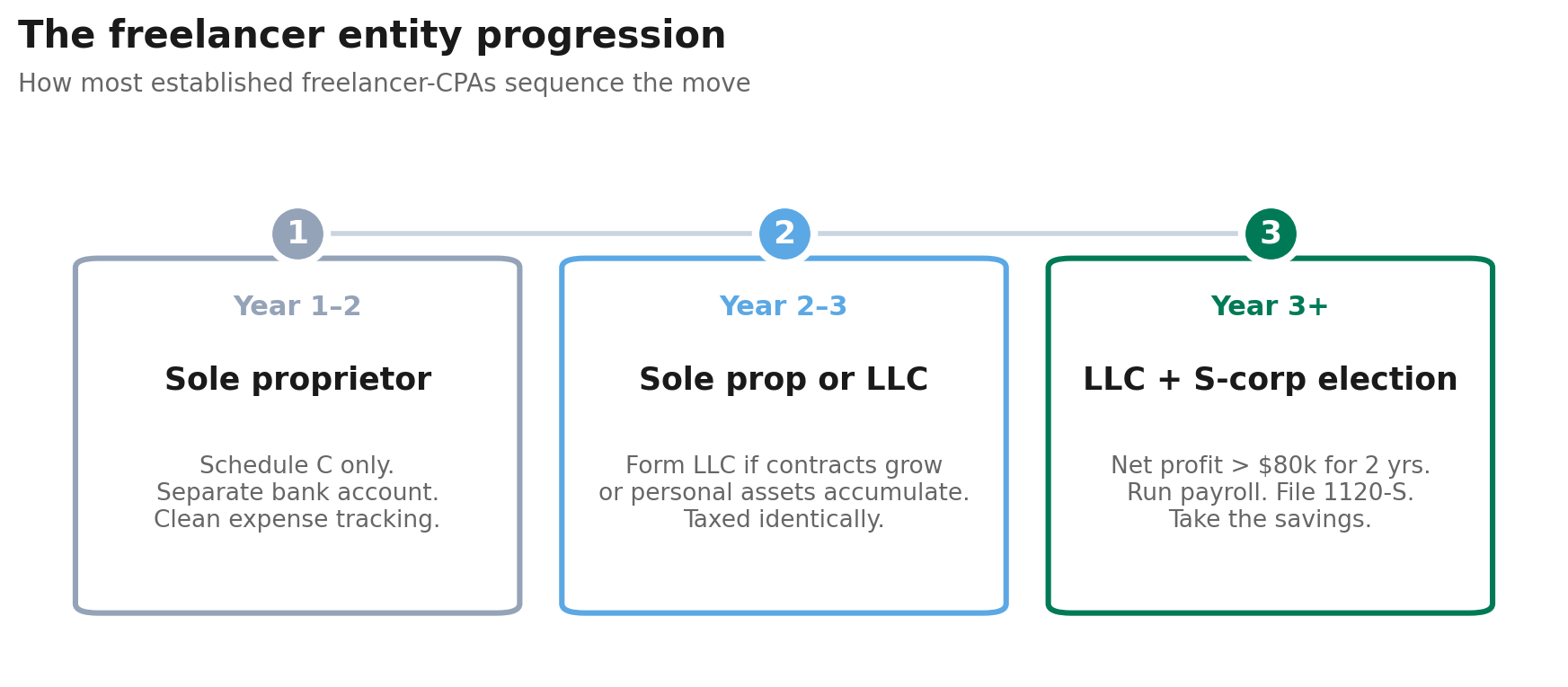

“Should I form an LLC and elect S-corp at the same time?”

Generally no. Sequence matters here.

Year one to two of freelancing: stay a sole proprietor. Use a separate business bank account anyway, even though the IRS doesn’t require one. Track everything in a real expense system. Get clean numbers on what you actually earn after expenses.

Year two to three, once contracts grow or assets accumulate: form an LLC. Cost is small. Protection is real. Keep filing as a sole proprietor for tax purposes (the LLC changes nothing on this front).

Year three plus, once net profit is consistently above $80,000 for at least two years: file Form 2553 and elect S-corp tax treatment for your existing LLC. Set up payroll. Build a relationship with a CPA. Take the savings.

This sequence is what most established freelancer-CPAs recommend. Optimize for simplicity early when you’re figuring out whether the income will hold. Optimize for savings later when the math actually works.

When to call a CPA, not Reddit

Reddit is fine for general orientation. It’s dangerous for entity decisions because the answer that worked for someone in Texas with $200,000 of profit will be wrong for you in California with $90,000.

What you want is a paid 30 to 60 minute consultation, not a free chat. Expect to pay $200 to $400 for it. The CPA should be one who works specifically with freelancers and S-corps, not your aunt’s general practice CPA who mostly does W-2 returns. Ask three questions on the call:

- Given my net profit and my state, does S-corp election save me money this year after all costs?

- What reasonable salary would you defend in an audit for someone in my line of work?

- Can you handle the Form 1120-S filing, or do I need a separate preparer?

If they can’t answer those three clearly, find a different CPA.

Get the free Entity Switch Decision Worksheet

One-page worksheet. Plug in your net profit, your state, and your projected income for next year. It runs the actual SE-tax-versus-S-corp-payroll math, factors in your state’s fees, and tells you whether to switch, wait, or stay where you are. No spreadsheet skills required.

Frequently Asked Questions

Do I need an LLC to freelance?

No. The default structure when you start working for yourself is a sole proprietorship. Zero paperwork required. Most freelancers operate this way for the first year or two with no problems. You only need an LLC when your contracts grow large enough that personal liability is a real concern, or when you have personal assets you want to put behind a legal wall. The IRS treats sole props and single-member LLCs identically for tax purposes, so forming an LLC will not change your tax bill.

Can I switch from sole proprietor to LLC mid-year?

Yes. You file articles of organization with your Secretary of State and obtain an EIN from the IRS. From the formation date forward, business income belongs to the LLC. You file one Schedule C for the year that combines pre-LLC and post-LLC income, since a single-member LLC is taxed identically to a sole proprietorship. Update your client contracts, invoicing, and bank account to the LLC name. Most freelancers find a January 1 effective date cleaner, but mid-year switches work fine.

What’s a “reasonable salary” for a freelancer with an S-corp?

The IRS standard is what someone else would pay an employee to do your work in your market. There is no formula in the tax code, but Bureau of Labor Statistics median wages for your job and city are the most defensible benchmark. A common middle-ground split is 60 percent salary, 40 percent distribution. Going below 50 percent salary is risky. Below 30 percent salary, you’re inviting an audit and potential reclassification. The case law (Watson v. United States, 2010) shows the IRS does pursue this and wins.

If I missed the March 2026 S-corp deadline, am I stuck for a year?

Not necessarily. Revenue Procedure 2013-30 allows late election relief if you file Form 2553 within 3 years and 75 days of the intended effective date, you have a reasonable cause for filing late, and you have been treating your books as if the election were already in place. You write “FILED PURSUANT TO REV. PROC. 2013-30” across the top of Form 2553 and attach a written reasonable cause statement. The IRS does grant this regularly. It’s not automatic, and you can’t just claim it because you forgot.

Does an S-corp election affect my SEP IRA or Solo 401(k)?

Yes, in a way that often helps. As a sole proprietor, your SEP-IRA contribution is capped at roughly 20 percent of net SE income. As an S-corp, you can contribute as both employee (up to the elective deferral limit, $24,500 in 2026) and employer (up to 25 percent of W-2 wages) to a Solo 401(k), often resulting in higher total contributions. This is one reason high-earning freelancers prefer S-corp structure beyond just the payroll tax savings. Coordinate this with your CPA before setting up.

Can I run an S-corp without payroll software?

Technically yes. Practically no. You’re required to withhold federal income tax, Social Security, and Medicare from your own paycheck, file Form 941 quarterly, file Form 940 annually, deposit taxes through EFTPS, and issue yourself a W-2 at year end. Doing this by hand on a single-owner S-corp is how you miss a deposit and trigger a penalty that wipes out your tax savings. Gusto, QuickBooks Payroll, and Patriot all handle this for $20 to $60 a month. The cost is built into the break-even math above.

Is forming an LLC enough, or do I also need business insurance?

An LLC and business insurance protect against different things. An LLC creates a legal wall between business debts and personal assets. Insurance (general liability, professional liability, errors and omissions) covers actual claims from clients. You generally want both. A web developer who forms an LLC but has no E&O insurance is still on the hook for a client lawsuit through the LLC’s assets, including any savings the LLC holds. For most freelancers, professional liability coverage runs $400 to $1,200 per year and is worth carrying alongside an LLC.

What happens to my QBI deduction when I elect S-corp?

Your W-2 salary does not count as qualified business income, so the salary portion is not eligible for the 20 percent QBI deduction. Your distribution is QBI and qualifies. Setting salary too low maximizes QBI but invites an audit. Setting salary too high shrinks your QBI base. For freelancers below the 2026 phase-out thresholds ($201,775 single, $403,500 joint), the wage interaction doesn’t matter much. Above those thresholds, especially for Specified Service Trades like consulting or financial services, salary planning becomes a real optimization problem worth a CPA conversation.

Do this week

Pull last year’s Schedule C. Find your net profit on line 31. Write that number down. If it’s below $50,000, close this tab and read about avoiding tax liability shock or how to file quarterly estimated taxes instead. If it’s above $80,000 and your income has been steady for two years, book a 30-minute call with a freelancer-savvy CPA before the end of the quarter. If you’re between $50,000 and $80,000, form an LLC if you haven’t already, and revisit the S-corp question after this year’s books close.

This article is informational and not tax or legal advice. Tax laws change. Numbers cited reflect 2026 IRS, SSA, and OBBBA figures verified against IRS.gov, SSA.gov, and Revenue Procedure 2025-32. Verify current rules with a qualified CPA or tax attorney before making entity decisions.

About the author

Gareth is an entrepreneur based in Dubai and the founder of AI Finance Tools for Freelancers. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide is researched from real user reviews, official documentation, and expert sources.