A 2026 state-by-state look at what freelancers actually pay at $60,000, $90,000, and $120,000 of net income. Real dollars, not vibes.

11pm. Sunday. You just finished your taxes and owe $7,400 you weren’t expecting. You google “freelance taxes by state” and the first five articles tell you California has a 13.3% top rate and Florida has zero. None of them tell you what an $80,000-a-year freelance designer actually pays in either state, after self-employment tax, after the QBI deduction, after the standard deduction, after the federal brackets stack up.

This article does that math on freelance taxes by state. For 50 states. At three income levels real freelancers earn: $60,000, $90,000, and $120,000.

Before you scroll to the table, you need to know what stays the same wherever you live and what changes when you cross a state line. Most freelancers get this wrong by thousands of dollars a year.

The three taxes every US freelancer pays (and the one that does not change by state)

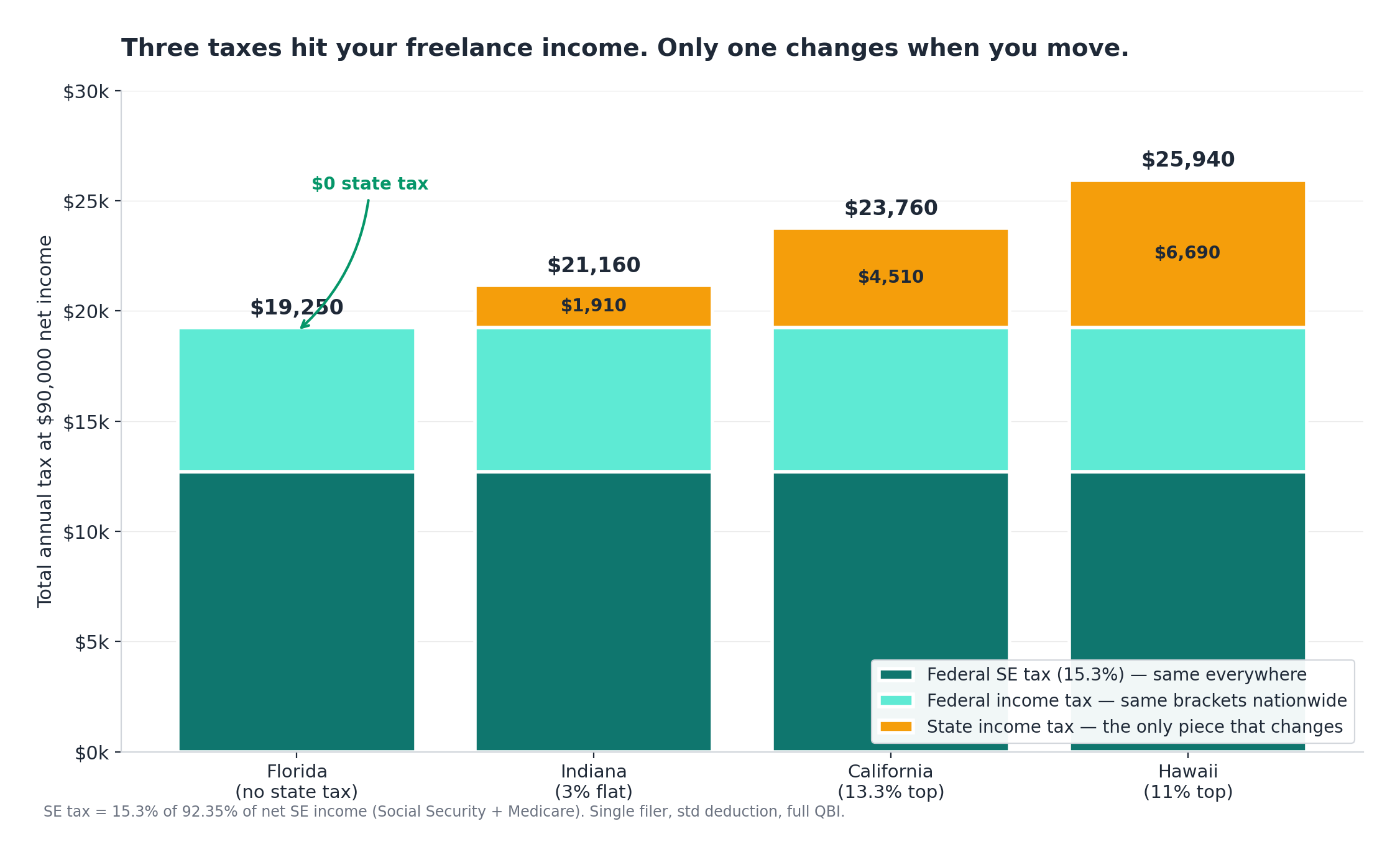

If you file a Schedule C, three taxes hit your net profit:

- Self-employment tax (federal, 15.3%). Social Security at 12.4% on the first $176,100 of net SE income in 2026, plus Medicare at 2.9% on all of it. The rate is identical in all 50 states. Wyoming gives you no discount. California charges no extra. Source: IRS.gov.

- Federal income tax (10% to 37% marginal rates) on your taxable income after deductions. Same brackets nationwide. Your effective rate is almost always lower than your top marginal bracket.

- State and local income tax (0% to 13.3%). The only piece that changes when you move.

Two federal mechanics shape every number in the table below. First, you deduct half of your self-employment tax from your taxable income before federal brackets apply. Second, the Qualified Business Income (QBI) deduction lets most freelancers deduct up to 20% of business income. The QBI phaseout starts at $383,900 single or $483,900 married filing jointly in 2026, so anyone in our income range gets the full deduction. Specified Service Trade or Business rules can limit it for consultants, accountants, lawyers and health professionals at higher incomes. At $120,000 you sit well below the threshold.

The 2026 standard deduction for a single filer is $15,750, per the One Big Beautiful Bill Act signed July 4, 2025 and confirmed in IRS Rev. Proc. 2025-32. For married filing jointly it’s $31,500. Most freelancers take the standard deduction because business expenses come off the top on Schedule C, separate from itemizing. If you want a line-by-line walkthrough of how Schedule C actually works, including how 1099-NEC income flows in, see our Schedule C line-by-line guide.

Freelance taxes by state: what you actually pay at $60,000, $90,000, and $120,000

How to read this table

The numbers below assume a single freelancer, no W-2 income, the standard deduction, full QBI deduction, and the 50% SE tax deduction applied. State numbers use 2026 brackets from each state’s Department of Revenue. Federal numbers use 2026 IRS brackets. Self-employment tax sits at 15.3% across the board.

The “Total Tax” column is what you actually owe across federal income, federal SE, and state income. It does not include property tax or sales tax. Both can swing your real cost of living more than the income tax in some states.

One thing to lock in before you read. The SE tax piece (~$8,478 at $60k, ~$12,716 at $90k, ~$16,955 at $120k) is identical wherever you live. The variance you see between states comes almost entirely from state income tax plus a small federal effect from the state tax deduction interaction.

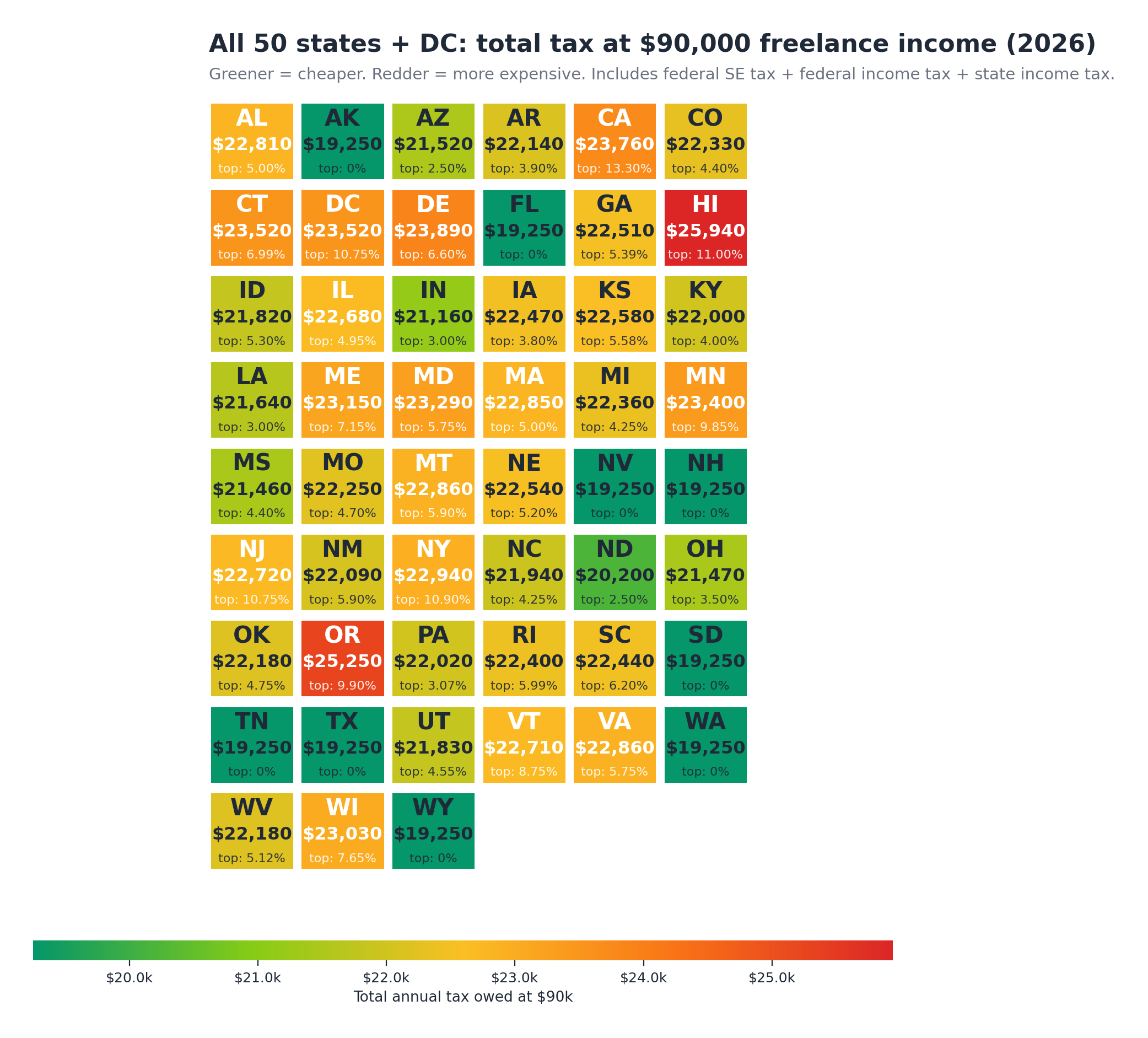

The full 50-state breakdown (2026)

| State | Total tax @ $60k | Total tax @ $90k | Total tax @ $120k | Top marginal state rate |

|---|---|---|---|---|

| Alabama | $13,940 | $22,810 | $32,650 | 5.00% |

| Alaska | $11,730 | $19,250 | $28,250 | 0.00% |

| Arizona | $13,250 | $21,520 | $30,910 | 2.50% flat |

| Arkansas | $13,560 | $22,140 | $31,650 | 3.90% |

| California | $13,910 | $23,760 | $34,420 | 13.30% |

| Colorado | $13,640 | $22,330 | $31,950 | 4.40% flat |

| Connecticut | $14,180 | $23,520 | $33,700 | 6.99% |

| Delaware | $14,420 | $23,890 | $34,180 | 6.60% |

| Florida | $11,730 | $19,250 | $28,250 | 0.00% |

| Georgia | $13,740 | $22,510 | $32,200 | 5.39% flat |

| Hawaii | $15,180 | $25,940 | $37,650 | 11.00% |

| Idaho | $13,360 | $21,820 | $31,290 | 5.30% flat |

| Illinois | $13,840 | $22,680 | $32,420 | 4.95% flat |

| Indiana | $13,000 | $21,160 | $30,440 | 3.00% flat |

| Iowa | $13,830 | $22,470 | $32,070 | 3.80% flat |

| Kansas | $13,800 | $22,580 | $32,260 | 5.58% |

| Kentucky | $13,490 | $22,000 | $31,460 | 4.00% flat |

| Louisiana | $13,180 | $21,640 | $31,030 | 3.00% flat |

| Maine | $13,830 | $23,150 | $33,290 | 7.15% |

| Maryland | $14,170 | $23,290 | $33,310 | 5.75% (plus county 2.25-3.20%) |

| Massachusetts | $13,930 | $22,850 | $32,750 | 5.00% flat (9% over $1M) |

| Michigan | $13,660 | $22,360 | $31,990 | 4.25% flat |

| Minnesota | $13,910 | $23,400 | $33,750 | 9.85% |

| Mississippi | $13,090 | $21,460 | $30,790 | 4.40% flat |

| Missouri | $13,610 | $22,250 | $31,840 | 4.70% |

| Montana | $13,790 | $22,860 | $32,720 | 5.90% |

| Nebraska | $13,710 | $22,540 | $32,250 | 5.20% |

| Nevada | $11,730 | $19,250 | $28,250 | 0.00% |

| New Hampshire | $11,730 | $19,250 | $28,250 | 0.00% on earned income |

| New Jersey | $13,540 | $22,720 | $32,800 | 10.75% |

| New Mexico | $13,420 | $22,090 | $31,820 | 5.90% |

| New York | $13,890 | $22,940 | $32,930 | 10.90% |

| North Carolina | $13,400 | $21,940 | $31,440 | 4.25% flat |

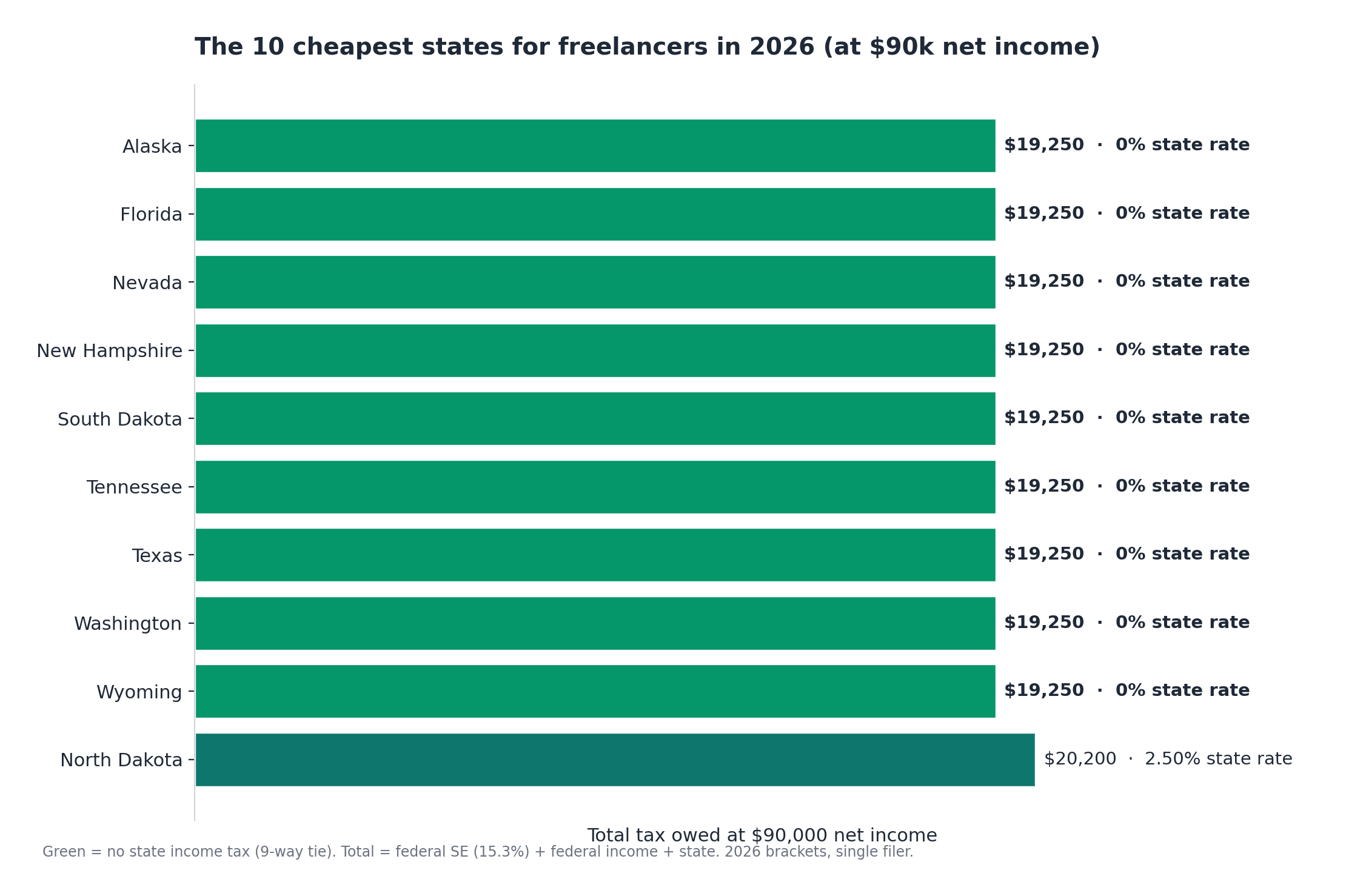

| North Dakota | $12,250 | $20,200 | $29,420 | 2.50% |

| Ohio | $13,150 | $21,470 | $30,800 | 3.50% |

| Oklahoma | $13,560 | $22,180 | $31,710 | 4.75% |

| Oregon | $14,950 | $25,250 | $36,420 | 9.90% |

| Pennsylvania | $13,570 | $22,020 | $31,420 | 3.07% flat |

| Rhode Island | $13,580 | $22,400 | $32,170 | 5.99% |

| South Carolina | $13,510 | $22,440 | $32,310 | 6.20% |

| South Dakota | $11,730 | $19,250 | $28,250 | 0.00% |

| Tennessee | $11,730 | $19,250 | $28,250 | 0.00% |

| Texas | $11,730 | $19,250 | $28,250 | 0.00% |

| Utah | $13,440 | $21,830 | $31,210 | 4.55% flat |

| Vermont | $13,750 | $22,710 | $32,650 | 8.75% |

| Virginia | $13,920 | $22,860 | $32,610 | 5.75% |

| Washington | $11,730 | $19,250 | $28,250 | 0.00% on earned income |

| West Virginia | $13,510 | $22,180 | $31,720 | 5.12% |

| Wisconsin | $13,830 | $23,030 | $33,000 | 7.65% |

| Wyoming | $11,730 | $19,250 | $28,250 | 0.00% |

| DC | $14,150 | $23,520 | $33,790 | 10.75% |

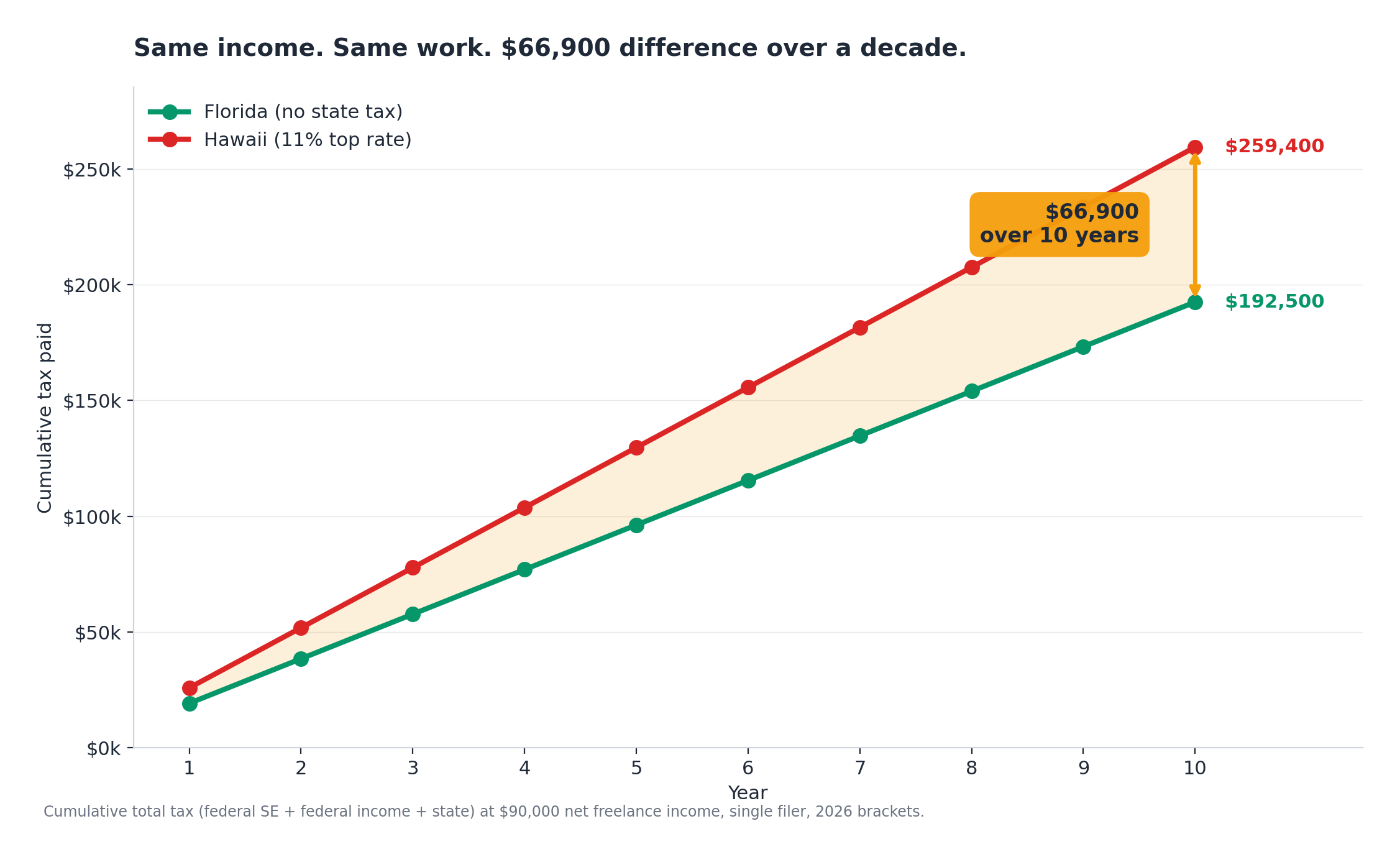

A few patterns jump out. The cheapest states (Wyoming, Florida, Texas, Nevada and the rest of the no-tax nine) cluster at $19,250 of total tax at $90k. Hawaii sits highest at $25,940. That’s a $6,690 spread on the same income. Over a decade? $66,900.

At $120,000 the gap widens. A Hawaii freelancer pays roughly $9,400 more per year than a Florida one. The cluster in the middle is tighter than most articles let on. Indiana (3% flat) and Massachusetts (5% flat) sit less than $1,700 apart at $90,000. Below the headlines, most US states tax freelancers within a few thousand dollars of each other.

If you want help turning these numbers into a monthly set-aside, our tax set-aside guide walks through the math at each income level.

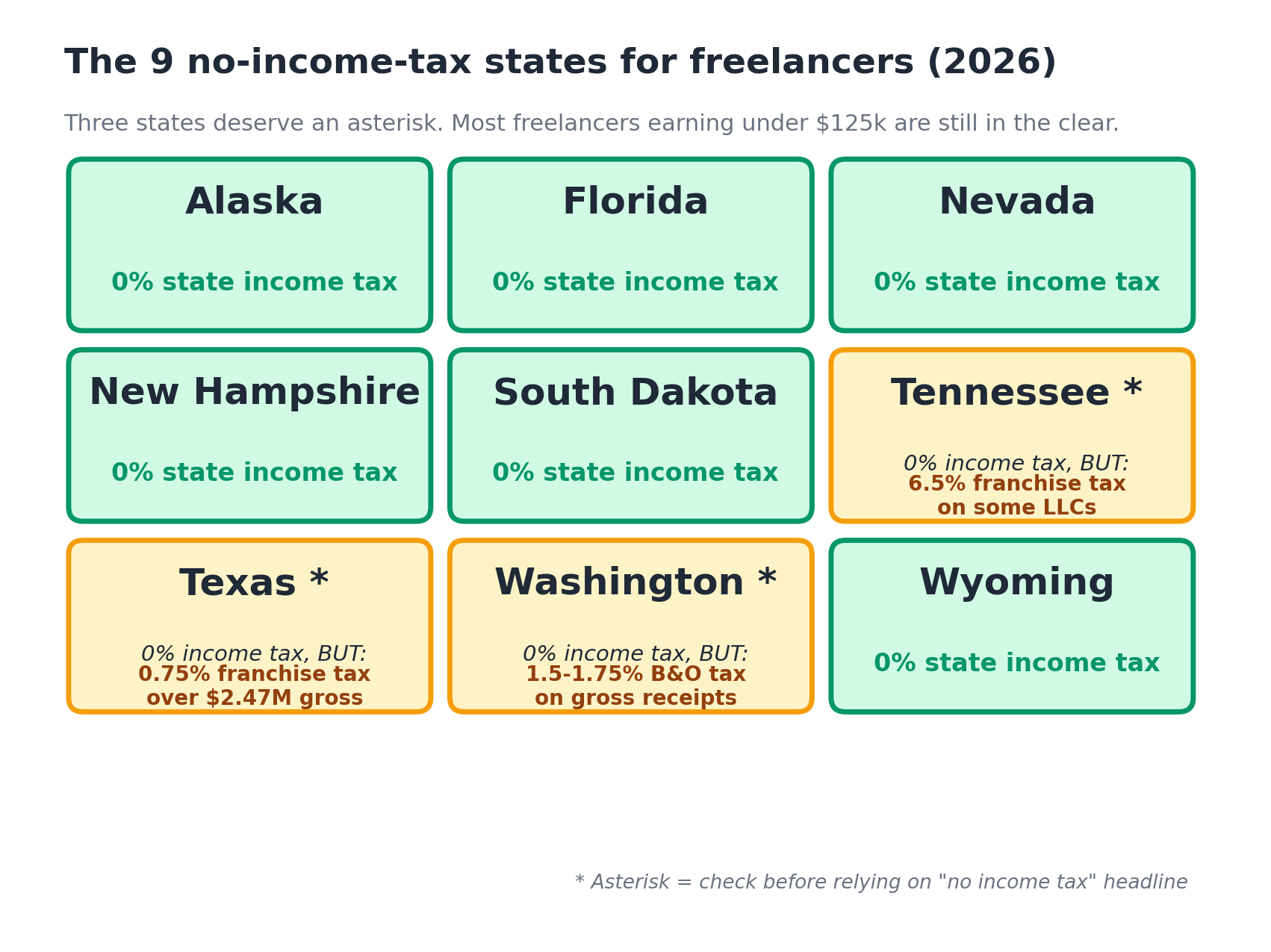

The nine no-income-tax states (and why three of them aren’t as cheap as they look)

Nine states charge zero state income tax on earned freelance income in 2026: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. New Hampshire repealed its tax on interest and dividend income for 2025, so it now joins the list cleanly for earned income. Source: Tax Foundation 2026 State Tax Competitiveness Index.

Three of those nine deserve an asterisk for freelancers:

- Washington charges a Business and Occupation tax on gross receipts (not net) once you cross the small business credit threshold. Service businesses pay 1.5% to 1.75% on gross receipts above the threshold, and Seattle adds its own B&O surtax. A Seattle freelancer grossing $200,000 can owe $3,000+ in B&O tax even with no state income tax.

- Texas has a 0.375% to 0.75% franchise tax on businesses, but most sole proprietors and single-member LLCs grossing under the $2.47 million threshold (2026) pay zero. Property tax averages 1.6% of home value, which lands harder than most expect.

- Tennessee repealed its Hall income tax on dividends in 2021 but kept high sales tax (9.55% combined average) and a 6.5% franchise/excise tax on certain pass-through entities. A sole prop is fine. An LLC electing corporate treatment is not.

Sole proprietor freelancer earning under $125,000 in Washington? The asterisk doesn’t apply to you. Single-member LLC grossing under $2.47 million in Texas? Same. Most freelancers in this guide’s income range are clear.

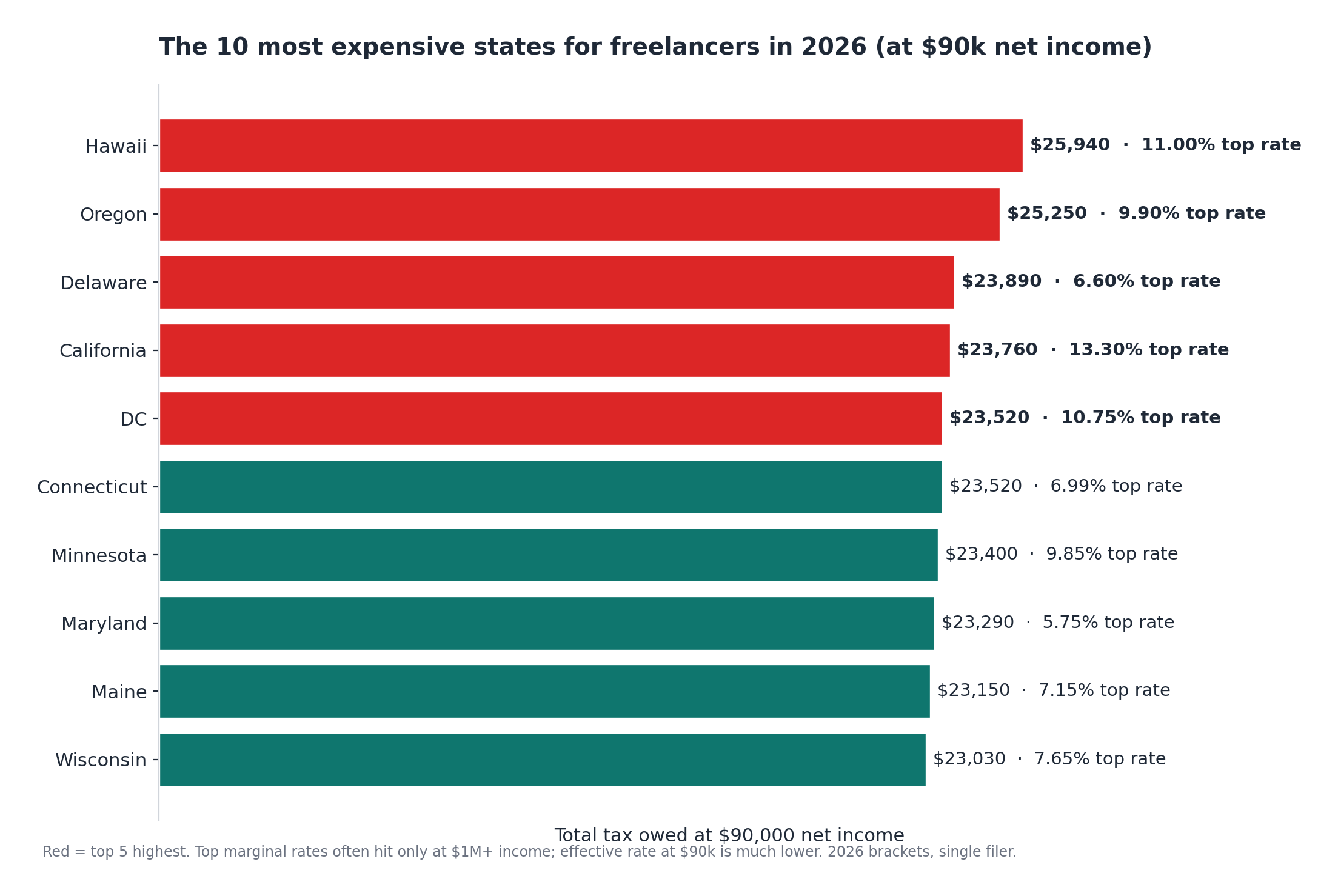

The five highest-tax states for freelancers in 2026

Ranked by total state-level tax bite on a $90,000 freelance income (state income tax only, before SE and federal):

- Hawaii ($6,690 state tax at $90k, 11% top marginal rate)

- Oregon ($6,000 state tax at $90k, 9.9% top marginal rate)

- California ($4,510 state tax at $90k, 13.3% top marginal rate, hits at $1M+)

- DC ($4,270 state-equivalent tax at $90k, 10.75% top rate)

- New York ($3,690 state tax at $90k, 10.9% top marginal rate, plus NYC city tax up to 3.876%)

New Jersey and Minnesota miss the top five but rank close behind. The New Jersey 10.75% top rate kicks in at $1 million. The Minnesota 9.85% rate kicks in around $217,000.

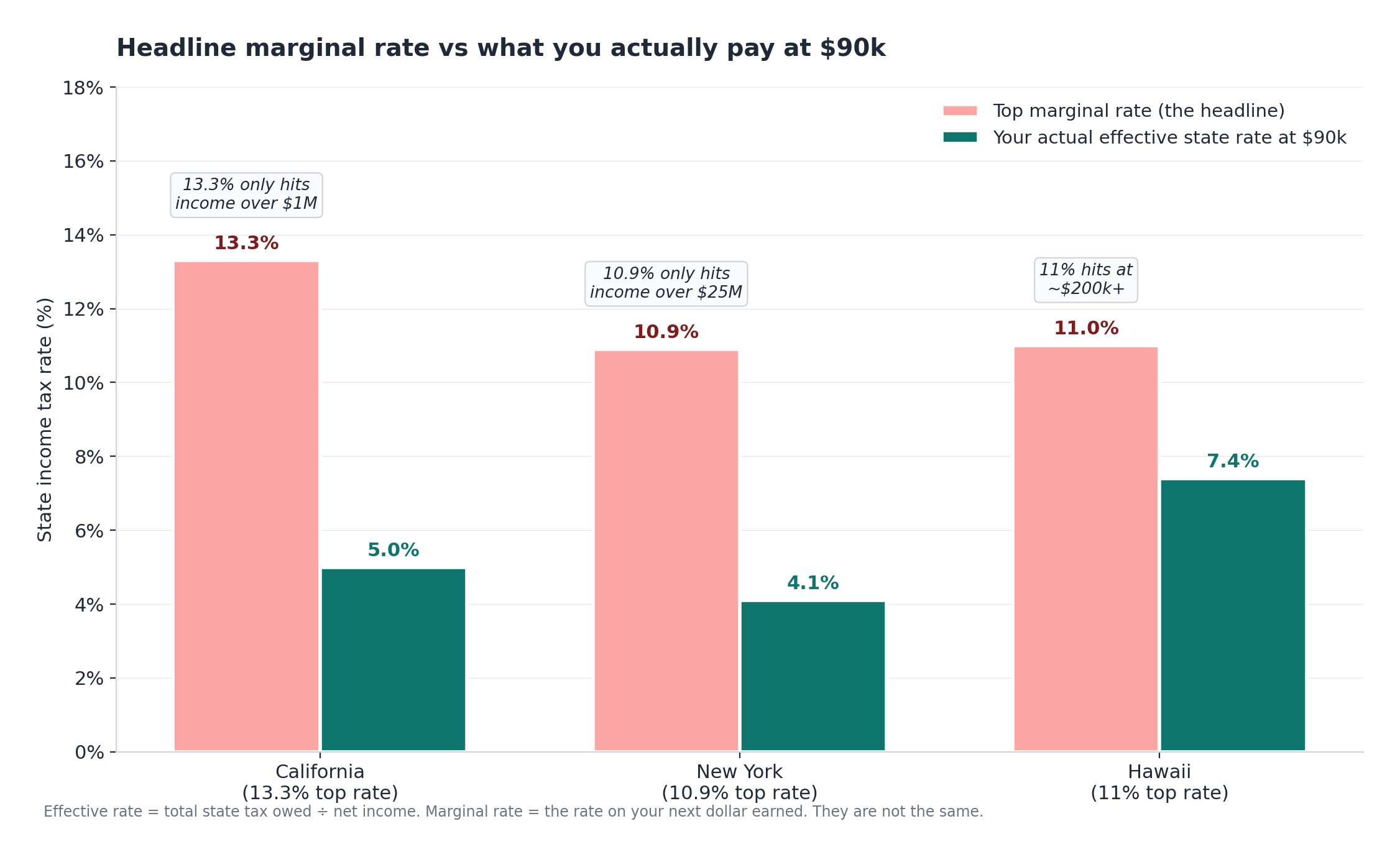

One nuance freelancers miss: there’s a wide gap between the top marginal rate and your effective rate. California’s 13.3% only hits income over $1 million. At $90,000, a California freelancer’s effective state rate sits closer to 5%. Same story with New York’s 10.9%, which kicks in at $25 million. Your actual rate depends on your bracket, not the cliff at the top.

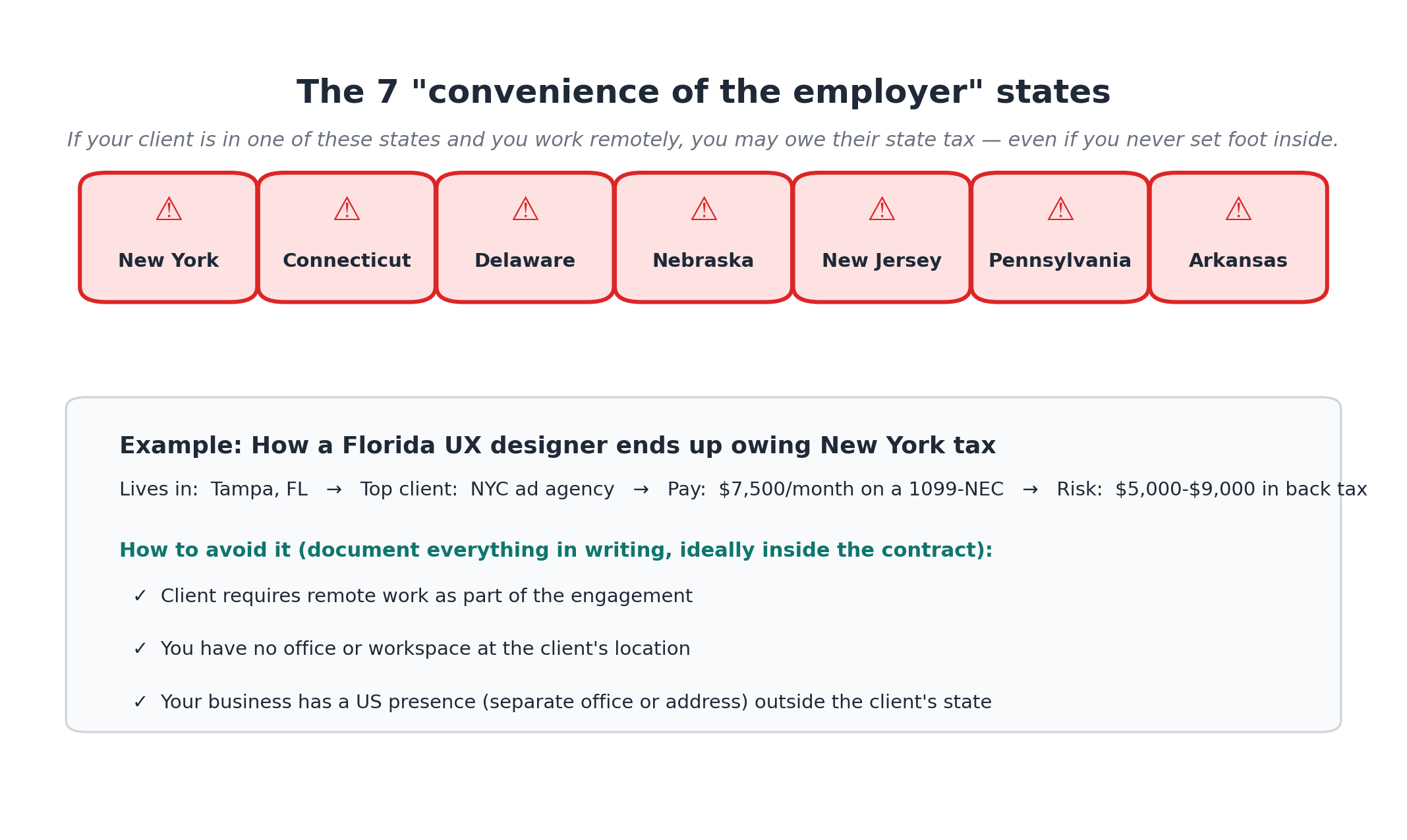

The convenience-of-the-employer trap

This is the rule that catches remote freelancers off guard. It costs them thousands of dollars they didn’t know they owed.

Seven states use a “convenience of the employer” rule to claim tax on remote workers earning income from a client based in that state, even if the worker never sets foot inside the state lines. The states: New York, Connecticut, Delaware, Nebraska, New Jersey (in reciprocal cases), Pennsylvania, and Arkansas.

Here’s how it plays out. A freelance UX designer lives in Florida. Her biggest client is a NYC ad agency that pays her $7,500 a month on a 1099-NEC. New York’s Department of Taxation and Finance can argue that because she chooses to work remotely “for her own convenience” (not because the client requires it), her income from that client is sourced to New York. She owes New York state and possibly NYC tax on it.

The workaround is documentation. The income avoids the rule when you can show:

- The client requires remote work as part of the engagement, in writing, ideally inside the contract.

- You have no physical office or workspace available at the client’s location.

- Your business has its own US presence (separate office, address, dedicated space) outside the client’s state.

For pure 1099 freelancers (versus W-2 remote employees), enforcement runs less aggressive than it is for salaried workers. It’s not zero. New York audits this. If you’re a Florida-based freelancer with a single $90,000-a-year New York client, talk to a CPA before you file. The downside risk on a missed sourcing call usually runs $5,000 to $9,000 in back tax, plus penalties and interest.

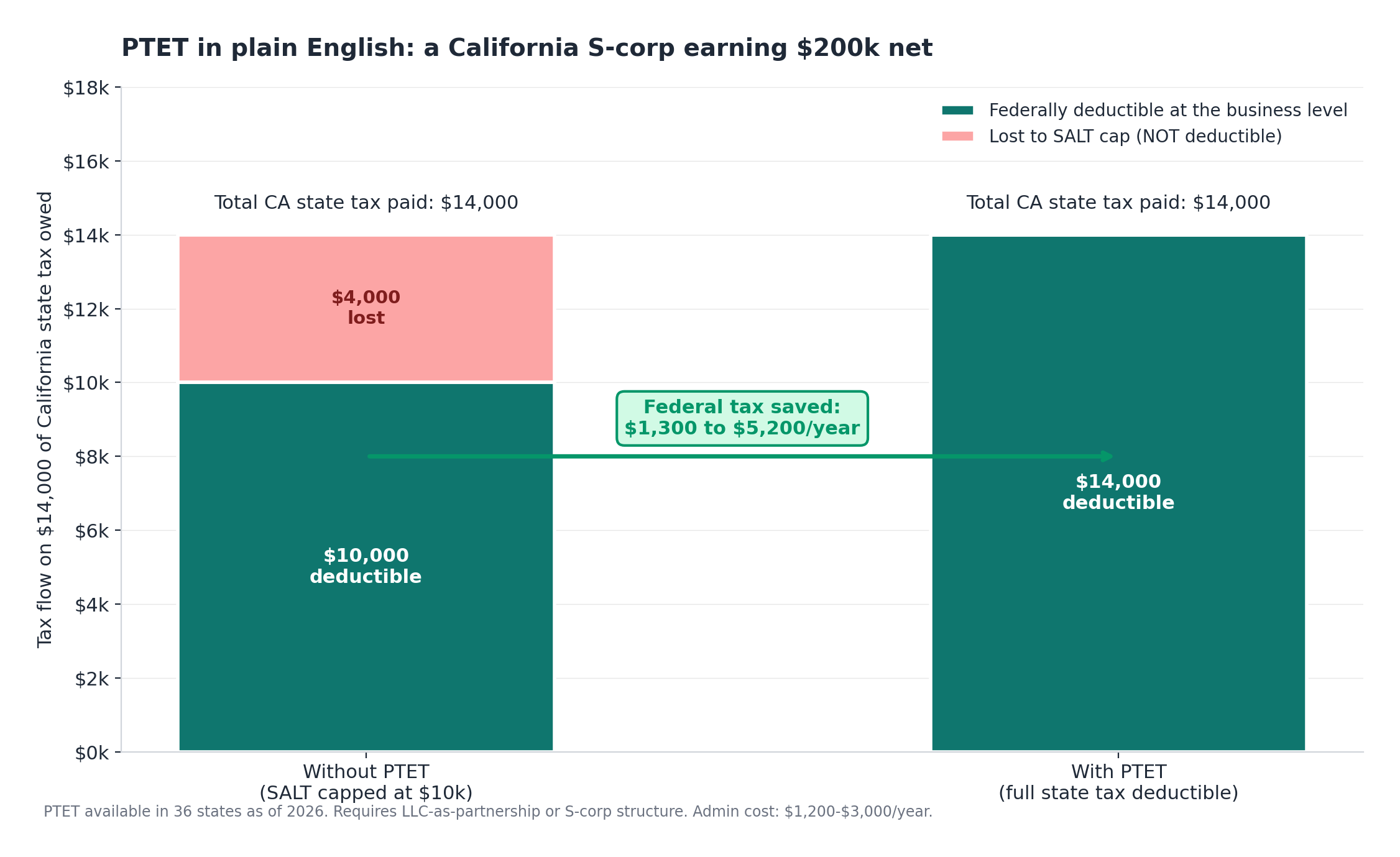

PTET: the legal workaround if you’re stuck in a high-tax state

If you live in California, New York, New Jersey or another high-tax state and you can’t move, the Pass-Through Entity Tax (PTET) is one of the most underused legal tax moves in the freelance world.

The 2017 Tax Cuts and Jobs Act capped the federal State and Local Tax (SALT) deduction at $10,000. That cap was raised by the One Big Beautiful Bill Act in 2025, but only temporarily and with phase-outs. PTET works around it. If you operate as an LLC taxed as a partnership or an S-corp, your business pays state income tax at the entity level, and that tax is fully deductible federally with no SALT cap.

A simplified example. A California freelance consultant operating as an S-corp earns $200,000 net. California state tax on that income runs roughly $14,000. Without PTET, only $10,000 is deductible federally under TCJA cap rules. With PTET, the full $14,000 flows through as a federal business deduction, saving roughly $1,300 to $5,200 in federal tax depending on the bracket.

PTET is available in 36 states as of 2026, including California, New York, New Jersey, Massachusetts, Maryland, Connecticut, Oregon, Minnesota, and Illinois. It’s not available in seven states that don’t tax pass-through entities at all, and not yet adopted in a handful of others.

The catch: PTET only works if your business is structured as a partnership or S-corp, not a sole proprietorship or single-member LLC taxed as a disregarded entity. Setting up an S-corp adds payroll, filing fees, and administrative cost, typically $1,200 to $3,000 a year. The math usually works at $80,000+ of net profit in a high-tax state. Below that, the admin cost eats the savings. If you’re considering structuring up, you’ll want clean accounting in place first. Our FreshBooks vs Xero comparison covers the two tools that handle S-corp accounting cleanly for solo operators.

Start Your Free Trial with [Tool Name]

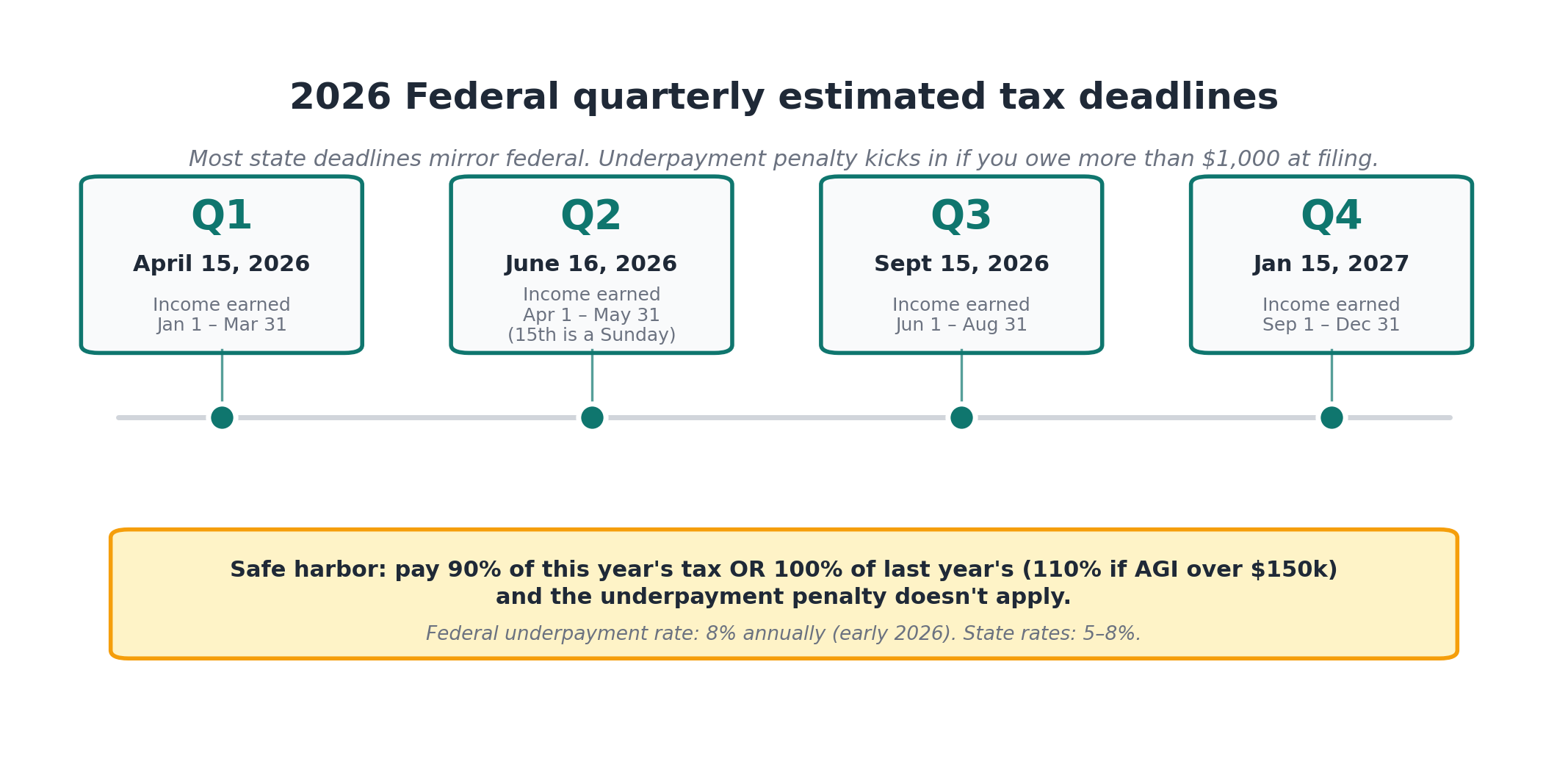

State quarterly tax deadlines and the estimated tax penalty

Federal estimated tax deadlines for 2026: April 15, June 16 (the 15th is a Sunday), September 15, and January 15, 2027.

Most states with income tax mirror the federal schedule. A few don’t. Arkansas runs a slightly different schedule for partnership and S-corp filers. Some states (Iowa, Virginia, others) shift the Q1 deadline by one to two weeks in specific years. Always check your state’s revenue department site directly. The mismatch list changes year to year and the penalty for missing isn’t worth saving the five minutes.

State portals to bookmark. California uses the Franchise Tax Board (ftb.ca.gov, Form 540-ES). New York uses the Department of Taxation and Finance (Form IT-2105). Illinois uses MyTax Illinois. State penalty rates vary, but most charge 5% to 8% annually for underpayment, similar to the federal 8% rate as of early 2026 per the IRS quarterly interest rate notice.

The estimated tax penalty kicks in if you owe more than $1,000 at filing and didn’t pay enough through quarterlies. The safe harbor: pay either 90% of this year’s tax or 100% of last year’s tax (110% if your AGI was over $150,000). Hit either number and the penalty doesn’t apply, even if you owe a balance.

If you’re in a no-income-tax state, ignore the state portion. You only owe federal quarterlies. Cross state lines mid-year and you may owe partial-year quarterlies in both. For step-by-step on actually making the payments, see our guide to filing quarterly estimated taxes and our guide to avoiding tax liability shock.

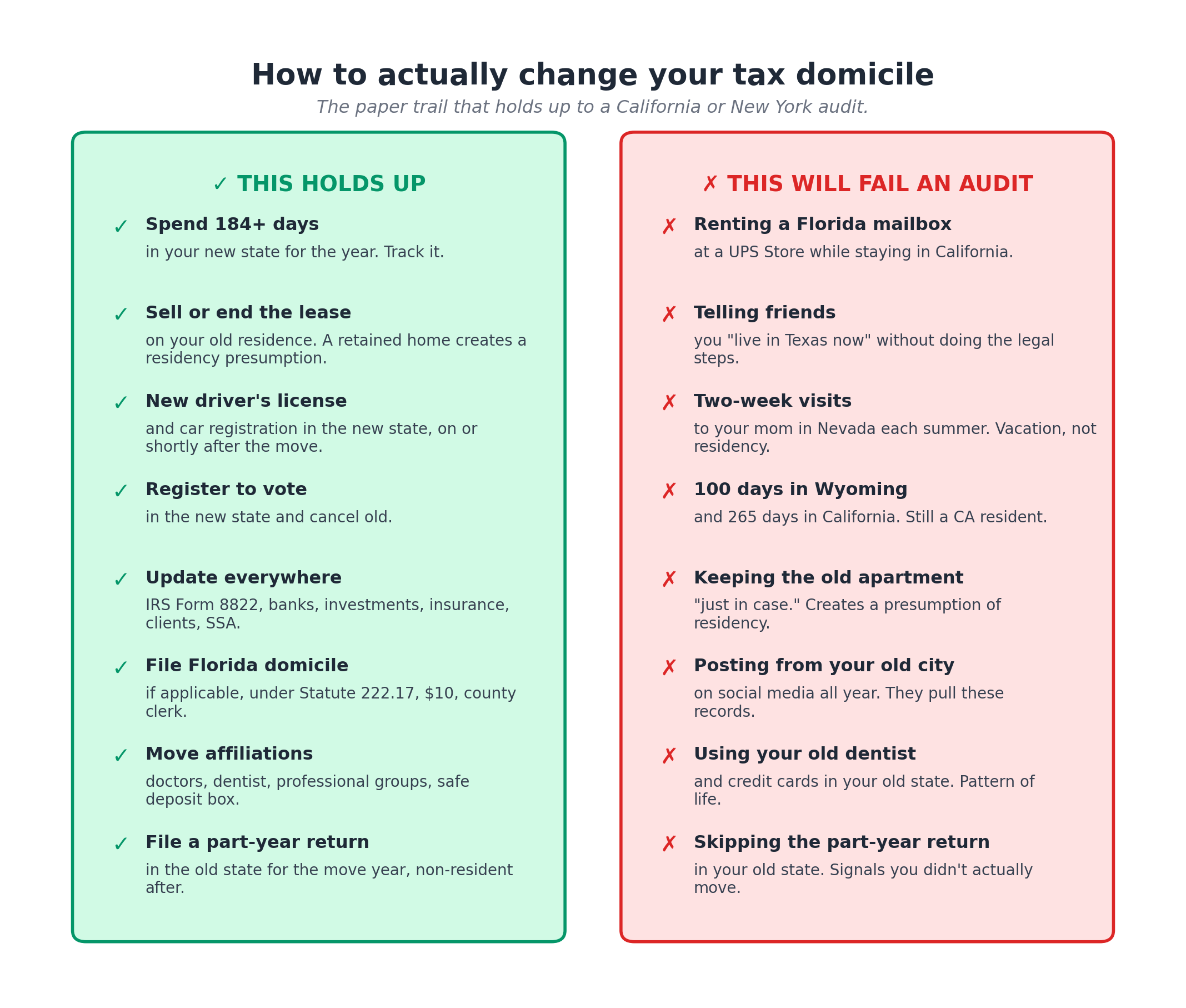

How to actually change your tax domicile (the paper trail that holds up)

What does not work

Renting a Florida mailbox at a UPS Store. Telling your friends you “live in Texas now.” Visiting your mom in Nevada for two weeks each summer. Spending 100 days in Wyoming and 265 days in California.

California, New York, Connecticut, and New Jersey audit aggressively. They will pull your credit card statements, your phone records, your social media posts, your dentist appointment dates, your kid’s school enrollment. Spend more days in California than in your “new” state and you’re still a California resident, no matter what your driver’s license says.

What does work

To establish domicile in a new state and end it in your old one, you need to do most or all of the following:

- Spend more than 183 days in the new state in the calendar year. Track it. Use a spreadsheet or an app like TaxBird.

- Sell or terminate your lease on your old residence. Keep a home in the old state and you create a presumption of continued residency.

- Get a new state driver’s license and register your car in the new state, on or shortly after the move.

- Register to vote in the new state, and cancel registration in the old one.

- Update your address with the IRS (Form 8822), your bank, your investment accounts, your insurance, your clients, and the Social Security Administration. Worth opening a fresh business bank account in your new state at the same time. Our freelancer bank account comparison covers Found, Relay, Novo, and Mercury, all of which let you open remotely with a new address.

- If moving to Florida, file a Declaration of Domicile under Florida Statute 222.17 with your new county clerk. One-page form, costs about $10, creates strong evidence of intent.

- Move your professional affiliations, your doctors, your dentist, and your safe deposit box.

- File a part-year resident return in the old state for the year of the move, and a non-resident return in subsequent years if you still earn income there.

Take a freelance writer moving from Brooklyn to Tampa in March 2026. New York State will probably accept the move if she signs a Tampa lease, gets a Florida license within 30 days, files her Declaration of Domicile, sells or terminates her Brooklyn lease, and spends fewer than 184 days in New York for the rest of the year. Keep the Brooklyn apartment “just in case” and the audit risk goes up significantly.

California has its own twist. A 546-day foreign-employment safe harbor (FTB Publication 1031) lets you be a non-resident if you’re abroad for 546 consecutive days under an employment contract. It does not apply if you’re a freelancer working for yourself with no employment contract. Most freelance digital nomads don’t qualify for this safe harbor and must end domicile the regular way.

The $3,200 mistake: multi-state freelancing and sourcing rules

You live in Pennsylvania. In 2026, you spend three months working from a co-working space in San Diego on a project for a Los Angeles-based startup. You earn $40,000 from that client over those three months.

Pennsylvania (your domicile state) wants tax on all your income, including that $40,000. California also wants tax on the $40,000, because the work was physically performed in California. You file a California non-resident return on the $40,000, pay roughly $2,200 in California state tax, and then claim a credit on your Pennsylvania return for taxes paid to California.

Skip the California non-resident return and California can find you. 1099 reporting, client records, electronic payment trails. Once they do, they assess back tax plus a 5% per month failure-to-file penalty up to 25% of the tax owed, plus interest. That $2,200 of original tax can become $3,200 within a year of penalties and interest.

Two practical rules:

- If you physically work in another state for more than a few weeks, check that state’s nonresident filing threshold. Most states require a return if you earn more than a small amount (often $1,000 to $5,000) while physically present.

- If your client is in a “convenience” state (NY, CT, DE, NE, NJ, PA, AR), document that remote work is a business necessity, not a preference. A clause in the contract is the cleanest evidence.

For tracking which expenses count as business in multi-state work, see our guide on tracking business expenses as a freelancer. If you’d rather offload expense categorization to AI rather than do it yourself, our Keeper Tax review and FlyFin review cover the two main contenders, and our FlyFin vs Keeper Tax comparison walks through which one fits which type of freelancer.

A 5-minute decision framework: should you move?

Run this in order. Answer “no” at any step and the move probably isn’t worth it.

- Annual state tax savings: Look up your current state and your target state in the table above. Subtract. If the difference at your income level is under $4,000/year, the move probably isn’t financially driven.

- Cost of living swing: Compare median rent or housing cost between your current city and the target city. A move from Brooklyn to Tampa saves ~$8,000/year in state tax at $90k of income. Tampa’s cost of living can shift housing costs by $0 to $1,500/month depending on neighborhood. The net effect can be positive or negative.

- Client risk: If your top three clients are in your current state and rely on in-person meetings, moving can cost you 10% to 30% of revenue in the first year. Model that.

- Convenience-of-employer exposure: If your top client is in NY, CT, DE, NE, NJ, PA, or AR, the move may not save you state tax. Read the section above and check with a CPA.

- Domicile difficulty: Moving away from California, New York, Connecticut, or New Jersey is harder and more audited than moving away from any other state. Budget $1,500 to $4,000 in legal/CPA fees for the move year.

Clear all five steps and the savings are real, the math usually favors moving. Earning $90,000 in California and considering Tampa? Income tax savings alone (~$4,500/year) plus likely lower housing cost in many parts of Tampa plus no commute friction can make the math work in 12 to 18 months. Earning $60,000 in Indiana and considering Texas? The savings (~$1,300/year) probably don’t justify the move on tax grounds alone.

Free 2026 Quarterly Tax Set-Aside Calculator

If you want a simple Google Sheet that calculates your quarterly set-aside based on your state, your filing status, and your projected net income (so you stop guessing 25% and getting hit with 32%), drop your email below. You’ll get the sheet, a one-page state quarterly deadline cheat sheet, and a short email series on the four most-missed deductions for freelancers.

Frequently Asked Questions

Does self-employment tax change by state?

No. The 15.3% self-employment tax (12.4% Social Security, 2.9% Medicare) is federal, set by the IRS, and the same in every state. It applies to net SE earnings up to the Social Security wage base of $176,100 in 2026. The Medicare portion has no cap, and an additional 0.9% Medicare tax kicks in over $200,000 single filer. Source: IRS Self-Employment Tax page.

If I move from California to Texas in June, what do I file?

You file a California part-year resident return (Form 540NR) reporting the income earned while a California resident. You file no Texas return because Texas has no state income tax. California will tax your income earned January through June, plus any California-sourced income earned after the move. Keep clients in California after the move and expect California to assert nexus over that revenue. Your federal return is filed normally as a full-year US resident.

Do I owe state tax in every state I have a client in?

Generally, no. State tax follows where the work is physically performed (with the exception of the seven “convenience of employer” states). If you’re in Florida and your client is in Ohio, and you work from Florida the whole time, you owe Florida tax (zero) and not Ohio tax. Spend three weeks working on-site in Ohio and you may owe an Ohio non-resident return for that portion. Sourcing rules vary by state, so check the specific state’s filing thresholds.

Is forming a Wyoming LLC actually saving me state tax?

Probably not, if you live somewhere else. A single-member LLC is a “disregarded entity” for federal tax purposes, meaning the income flows to your personal return regardless of where the LLC is formed. If you live in California and your Wyoming LLC earns $100,000, California taxes you on that $100,000 because you, the owner, are a California resident. The LLC’s state of formation doesn’t matter for state income tax. It can matter for liability protection, privacy, and certain registration costs.

What is the cheapest state for a freelancer making $80,000?

For pure income tax, any of the nine no-income-tax states (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming) ties at zero state income tax. For overall affordability (income tax plus property plus sales plus cost of living), Wyoming, Tennessee, and Florida tend to rank highest. Alaska is technically the cheapest tax-wise but has high cost of goods and limited cost-of-living advantages outside Anchorage.

Do I have to pay quarterly state taxes too?

Yes, in most states with income tax, if you expect to owe more than a state-specific threshold (typically $400 to $1,000) for the year. Most state quarterly deadlines mirror the federal April 15, June 15, September 15, and January 15 schedule. Underpayment penalties apply at the state level just like the federal level. State has no income tax? You only pay federal quarterlies. Our quarterly estimated taxes guide covers the actual mechanics of paying both.

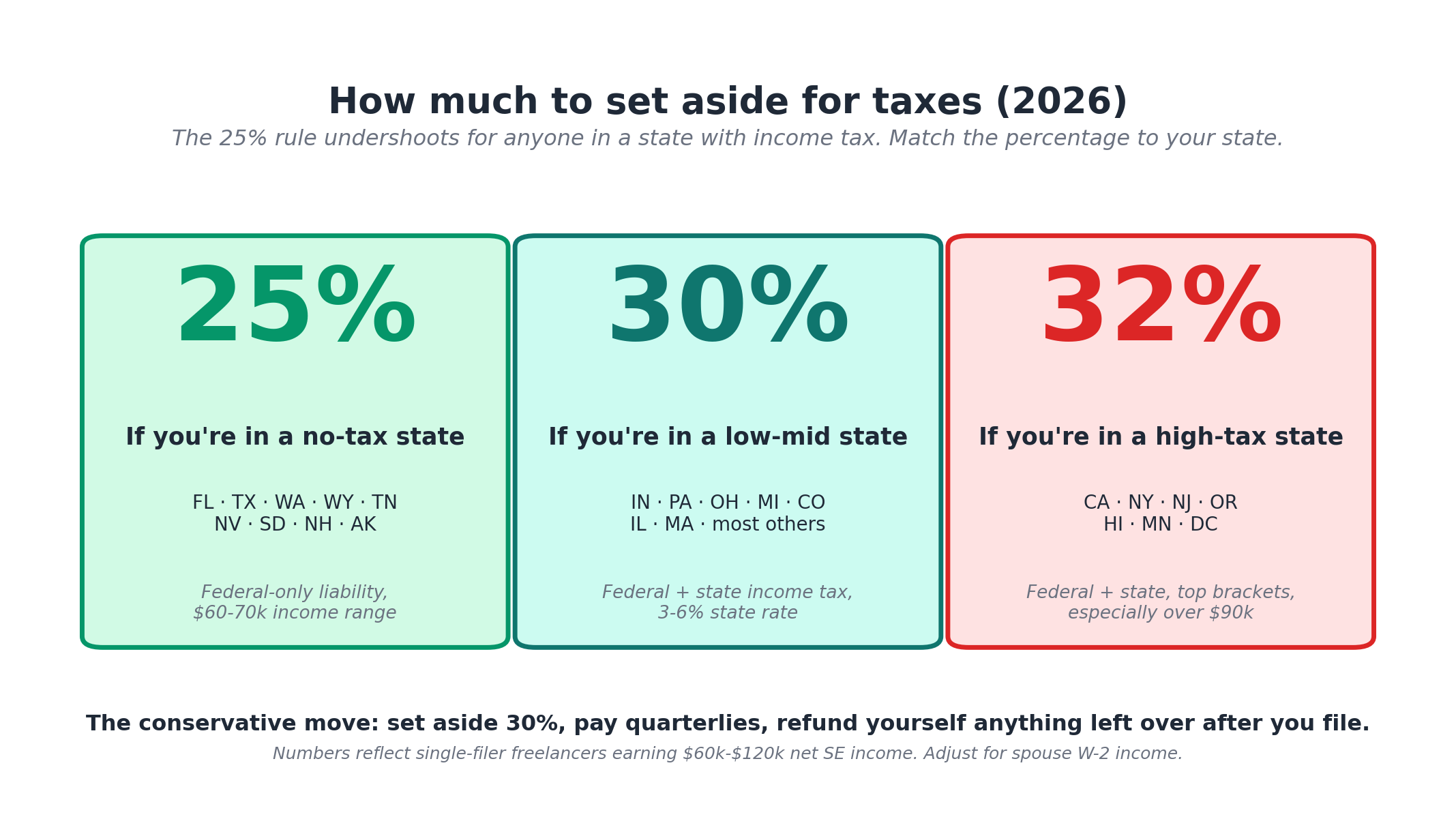

How much should I set aside for taxes as a freelancer in 2026?

For most freelancers earning $60,000 to $120,000, set aside 28% to 32% of every payment. The 25% rule undershoots for anyone in a state with income tax. In a no-income-tax state at $60,000, 25% works. In California at $90,000, you need closer to 30%. The conservative move: set aside 30%, pay your quarterlies, refund yourself anything left over after you file. For the full math at each income level, see how much freelancers should set aside for taxes. For broader cash flow strategy, see our guide on managing cash flow as a freelancer.

If I’m a digital nomad with no fixed home, where do I pay state tax?

You always have one tax domicile, even without a fixed physical home. It’s typically the state where you maintain your driver’s license, voter registration, mailing address, and where you intend to return. Many freelance digital nomads establish domicile in Florida, Texas, South Dakota, or Nevada before going abroad to avoid having a high-tax state assert continuing residency. Once domicile is established, you owe state tax to that state on income earned worldwide while a resident, until you formally change domicile to a different state.

That covers the core of freelance taxes by state for 2026. This article doesn’t cover the tools and software you use to track all of this. For a deeper look at our tested favorites, see our reviews of accounting software for freelancers and invoicing software for freelancers.

One thing to do this week

Open a spreadsheet. In one column, write your projected net income for 2026. In a second column, write your current state tax (from the table above). In a third column, write the same number for the cheapest state you’d actually consider living in. Subtract. Multiply by ten. That’s your decade-level decision, in real dollars, on one piece of paper.

Then check whether your top client is in a “convenience” state. If yes, schedule a 30-minute call with a CPA before you do anything. If no, you have a clean decision to make.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently. Verify current rates and rules at IRS.gov and your state’s Department of Revenue website, or consult a qualified CPA or Enrolled Agent for advice specific to your situation. State income tax rates, brackets, and rules cited are current as of April 2026 based on Tax Foundation, state revenue department, and IRS publications.

About the author

Gareth is an entrepreneur based in Dubai and the founder of AI Finance Tools for Freelancers. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide is researched from real user reviews, official documentation, and expert sources.