A working freelancer’s walkthrough of how to file quarterly estimated taxes as a freelancer in 2026 — real dollar math, the deadlines that actually matter, and the IRS payment screens you’ll click through.

It’s 11pm on a Sunday in mid-September. Q3 estimated taxes are due in two days. You log into your bank account, see $9,840 sitting in checking, and have no idea how much of it belongs to the IRS. If that scene rings a bell, this guide is for you.

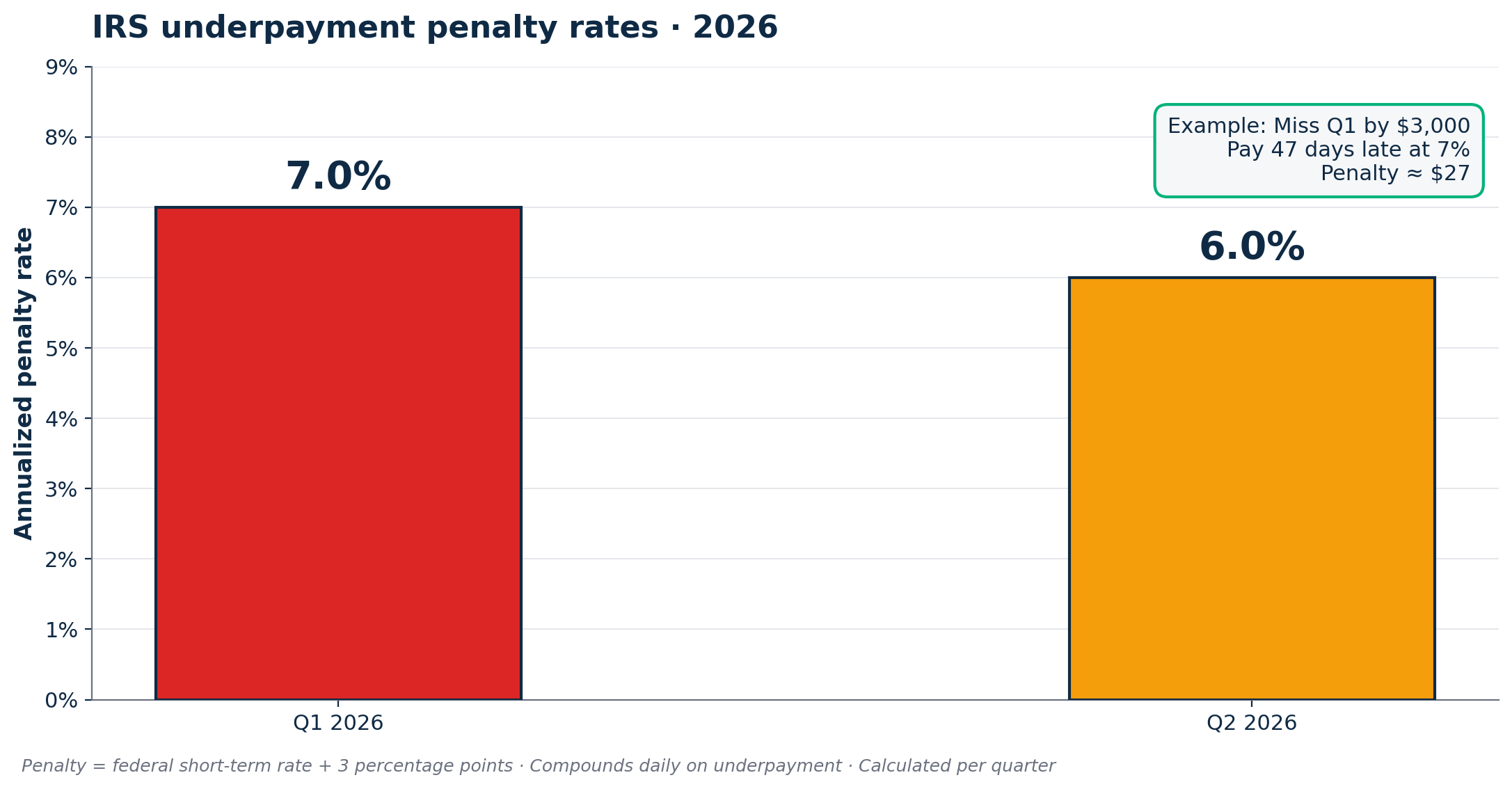

Here’s the deal. If you’re a Schedule C freelancer earning between $45,000 and $110,000 a year, you owe quarterly estimated taxes. Four payments. Four deadlines. Miss enough of them, or pay too little, and you get hit with a separate underpayment penalty on top of your tax bill. For Q1 2026, that penalty rate ran at 7% annualized. The IRS dropped it to 6% for Q2 2026. Both rates compound daily on your underpayment, per IRS Quarterly Interest Rates.

Most guides stop at the deadlines and a vague “set aside 25 to 30 percent” rule. I’m going further. You’ll get the full calculation, the exact IRS payment screens, the safe harbor numbers that keep you penalty-proof, what to do when your income jumps mid-year, and the specific 2026 changes from the One Big Beautiful Bill Act (OBBBA) that affect what you owe. If you want a deeper percentage breakdown for your specific income before getting into the quarterly mechanics, my companion guide on how much freelancers should set aside for taxes walks through the calculator and the math.

Do you actually need to file quarterly estimated taxes as a freelancer?

The threshold is simple. If you expect to owe $1,000 or more in federal tax for 2026 after subtracting any withholding and refundable credits, the IRS requires quarterly payments. That rule lives in IRC Section 6654. For most freelancers earning above roughly $5,000 in net profit with no W-2 withholding, you’re over the line.

Two situations let you skip quarterly payments. First, if your prior tax year showed zero total tax and you were a US citizen or resident for all 12 months. Second, if you have a W-2 job alongside your freelance work and you bump up your employer withholding using a fresh Form W-4 to cover both incomes. The second option is genuinely useful and the IRS specifically recommends it. Why? Because employer withholding gets treated as paid evenly across the year, regardless of when it actually happens. That’s a real loophole if you have W-2 income.

The penalty for skipping when you shouldn’t won’t ruin you. It’s just annoying. It compounds daily at the federal short-term rate plus three percentage points, and it gets calculated per quarter. Missing Q1 and overpaying in Q2 doesn’t erase the Q1 penalty. Per IRS estimated tax guidance, the agency assesses the penalty even when you pay the full balance with your annual return.

2026 quarterly tax deadlines

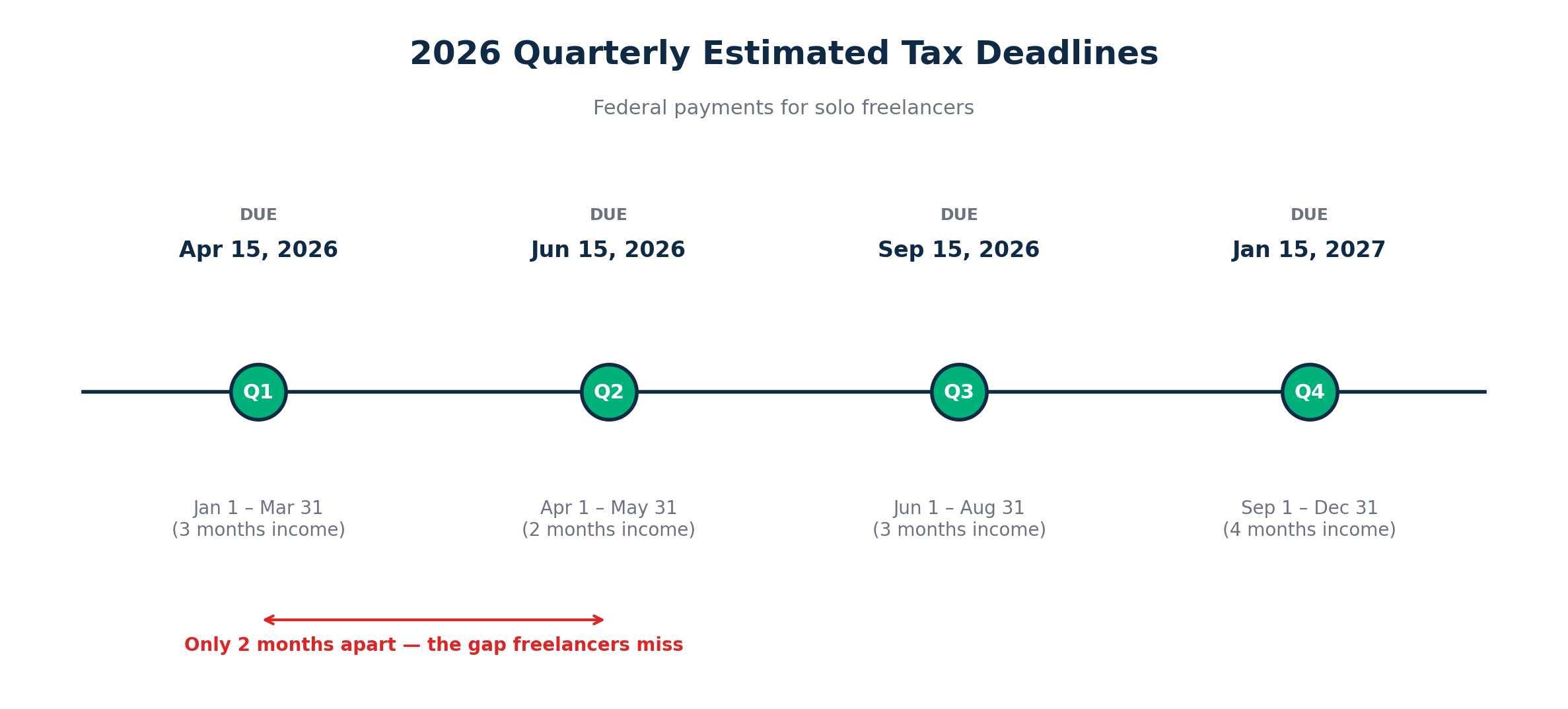

Despite the word “quarterly,” the IRS schedule is uneven. Q2 covers two months. Q3 covers three. Q4 stretches across four. Mark these now:

- Q1 2026 (income from January 1 to March 31): due April 15, 2026.

- Q2 2026 (income from April 1 to May 31): due June 15, 2026.

- Q3 2026 (income from June 1 to August 31): due September 15, 2026.

- Q4 2026 (income from September 1 to December 31): due January 15, 2027.

Here’s the trap. Q1 and Q2 sit only two months apart. You pay April 15, then again June 15. New freelancers regularly assume the next payment is three months out, plan their cash flow around that, and end up short. Put both dates in your calendar today. Set a one-week reminder before each.

If a deadline falls on a weekend or federal holiday, the payment is due the next business day. There’s also a useful exception for Q4. If you file your full 2026 Form 1040 by February 1, 2027, and pay your entire remaining balance with that filing, you can skip the January 15 Q4 payment entirely. This only works if you actually file and pay by February 1. Filing an extension doesn’t count.

The full math: what you actually owe each quarter

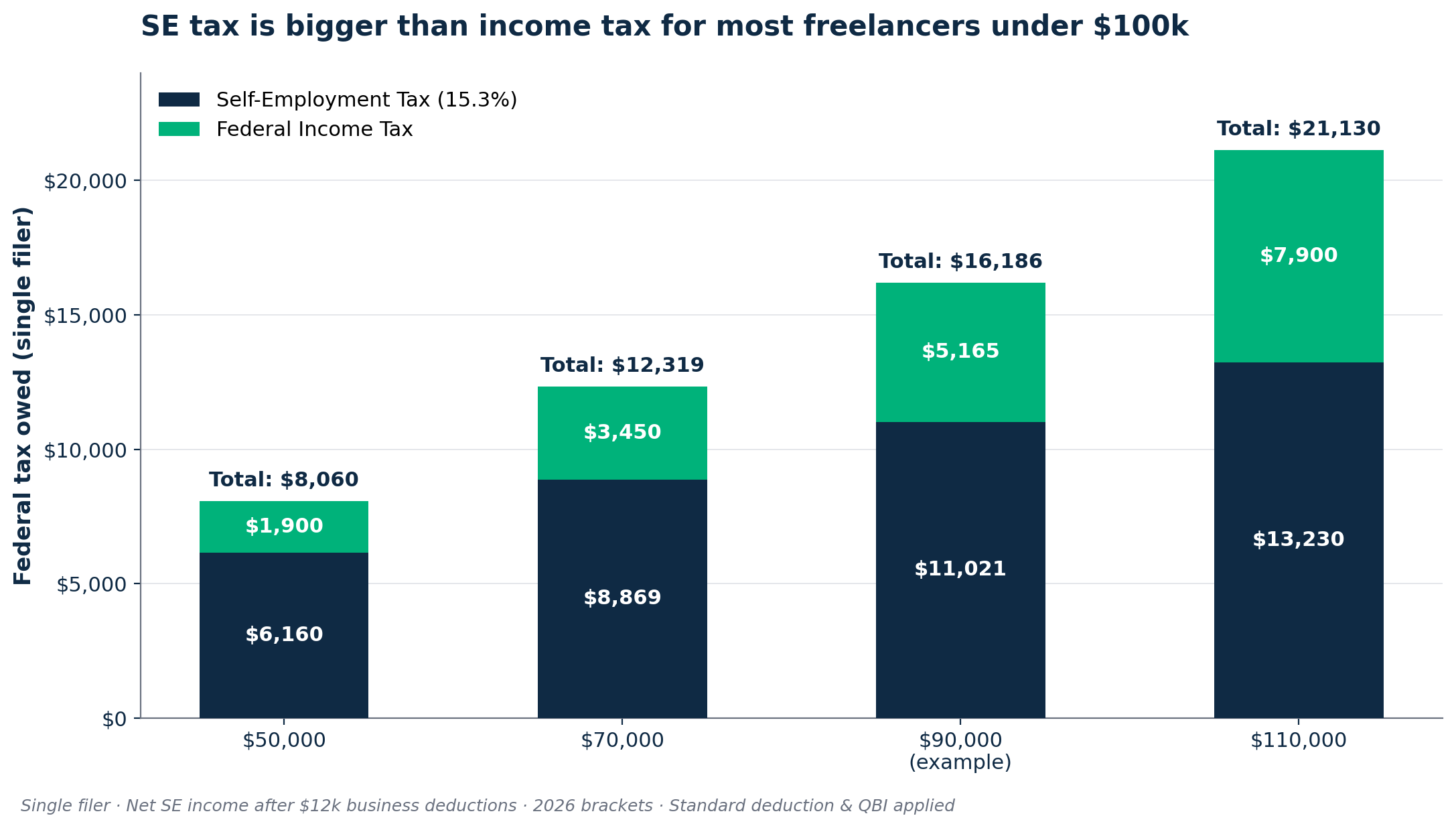

Most freelancers calculate their income tax, divide by four, and forget the 15.3% self-employment (SE) tax sitting on top. That mistake adds up to a five-figure surprise at filing time on a $90,000 income. It happens every April in the r/tax and r/freelance threads.

Here’s the real stack of taxes you owe:

- Federal income tax on your taxable income, using the 2026 brackets (10%, 12%, 22%, 24%, 32%, 35%, 37%) per IRS Revenue Procedure 2025-32.

- Self-employment tax at 15.3% on 92.35% of your net SE income, computed on Schedule SE. That breaks into 12.4% Social Security on the first $184,500 (the 2026 wage base per the SSA) plus 2.9% Medicare with no cap.

- Additional Medicare tax of 0.9% on SE income over $200,000 (single) or $250,000 (married filing jointly).

- State income tax, if you live in a state that has one. Nine states don’t. The other 41 vary widely.

Two tax breaks reduce the sting. You deduct half of your SE tax (the employer-equivalent portion) above the line, which lowers your AGI. You also deduct 20% of your Qualified Business Income (QBI) under Section 199A, which the OBBBA made permanent in July 2025. For 2026, there’s also a new minimum $400 QBI deduction if you have at least $1,000 of QBI and materially participate in the business. The full chain of where these numbers land on your tax return is covered in my Schedule C line-by-line guide for freelancers.

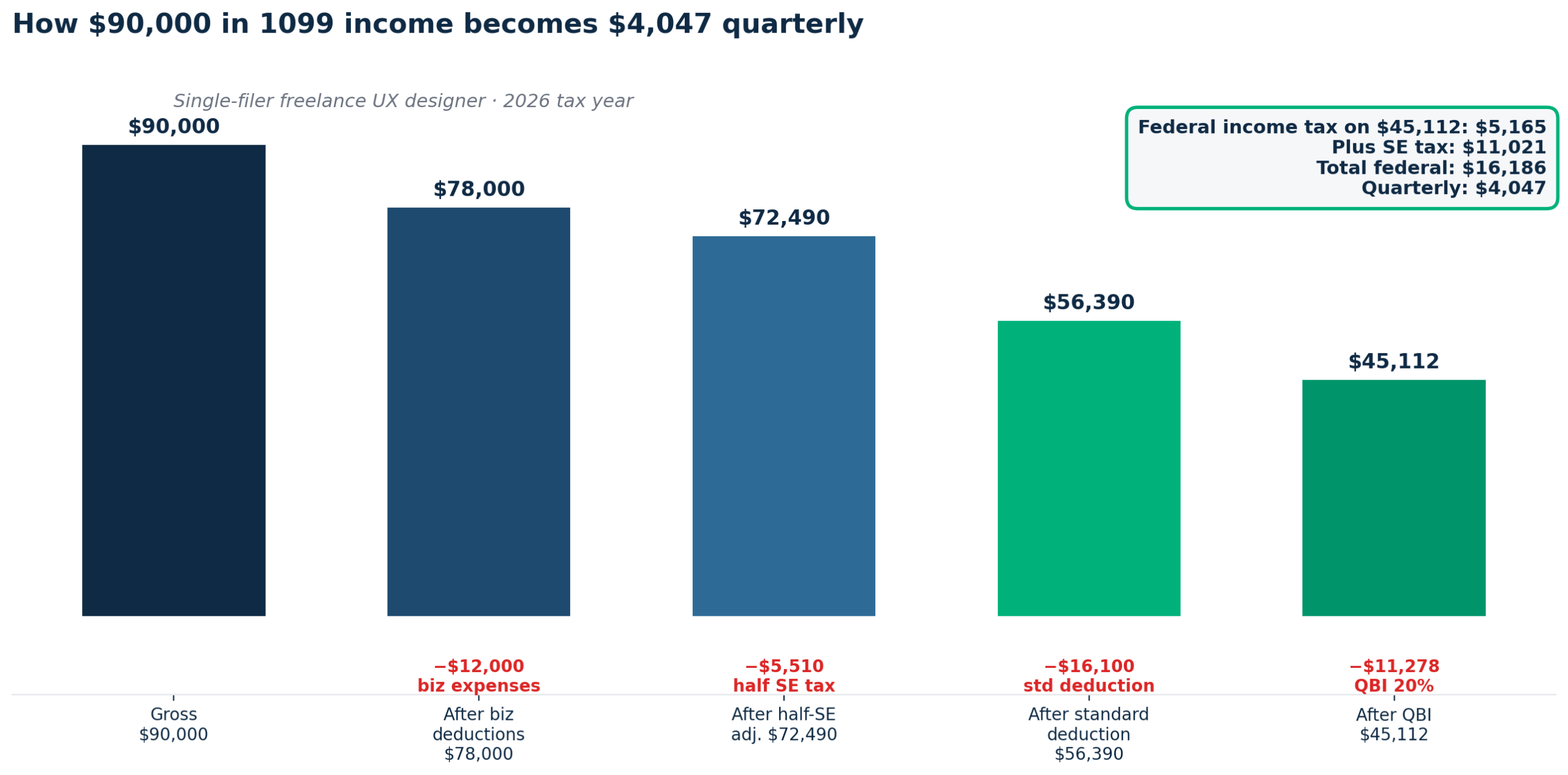

A worked example: a freelance UX designer earning $90,000

Take a single-filer freelance UX designer who expects $90,000 in gross 1099 income for 2026, with $12,000 in legitimate business deductions (software, home office, equipment, health insurance premiums). Net SE income comes to $78,000. Here’s the full calculation:

- SE tax base: $78,000 × 0.9235 = $72,033.

- SE tax owed: $72,033 × 0.153 = $11,021.

- Half of SE tax (above-line deduction): $5,510.

- AGI: $78,000 − $5,510 = $72,490.

- Standard deduction (single, 2026): $16,100.

- Taxable income before QBI: $56,390.

- QBI deduction (lesser of 20% of QBI or 20% of taxable income before QBI): $11,278.

- Taxable income: approximately $45,112.

- Federal income tax (2026 brackets): approximately $5,165.

- Total federal tax (income + SE): approximately $16,186.

- Quarterly payment: approximately $4,047.

Look at those two numbers. SE tax ($11,021) is more than double the income tax ($5,165). For most freelancers under $100,000, that ratio holds. If you size your tax savings off income tax alone, you’ll be short by thousands every year. Add state estimated tax separately. In California at roughly 6% effective on this income, that’s another $400 to $600 per quarter on top of federal.

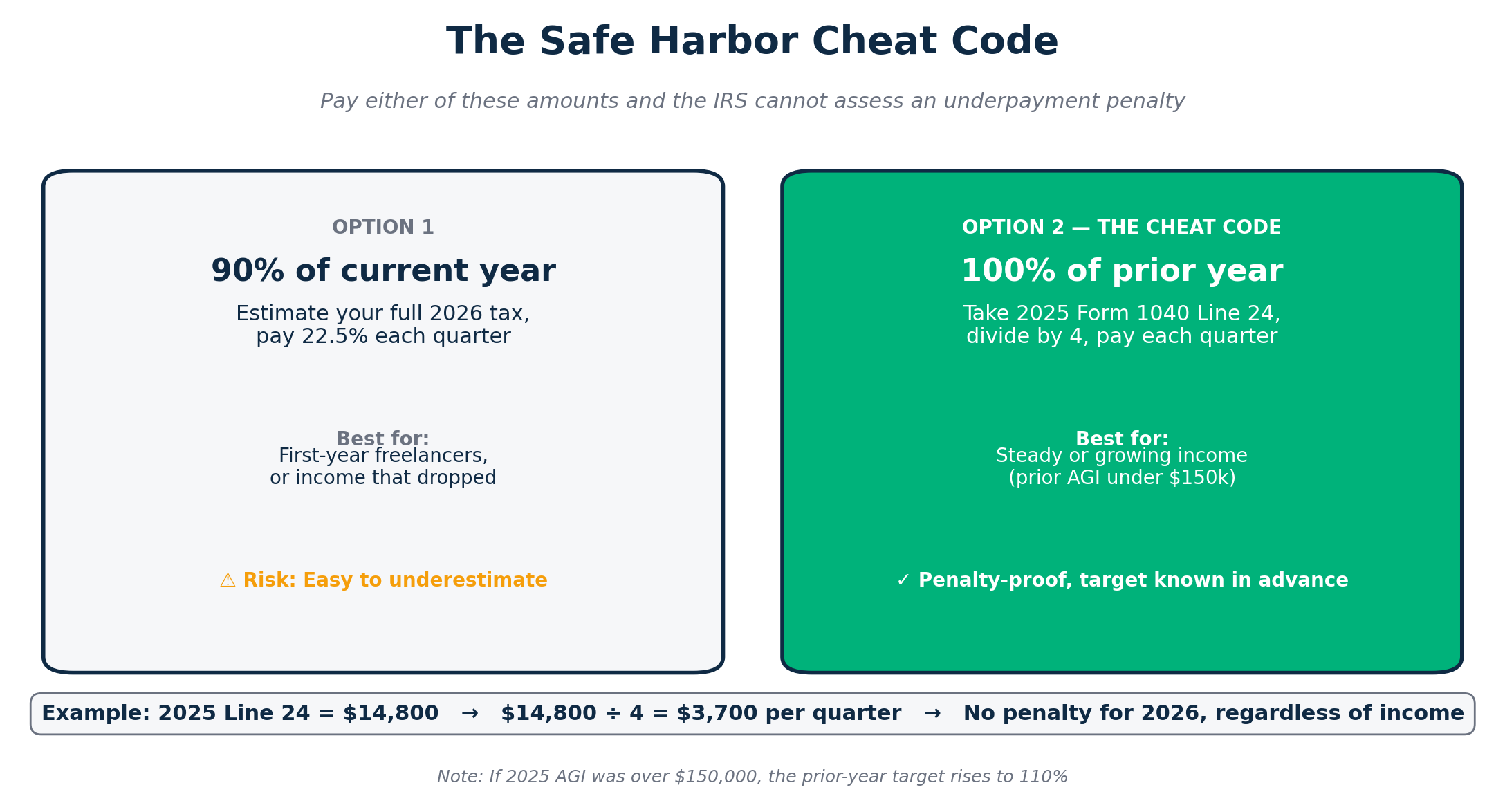

Safe harbor: how to never owe a penalty (the freelancer cheat code)

The IRS doesn’t penalize you for underestimating, as long as you hit one of two safe harbor thresholds. This is the most useful rule in the entire estimated tax system. Most freelancer guides bury it.

- Safe harbor option 1: Pay 90% of your current year (2026) total tax across the four quarters.

- Safe harbor option 2: Pay 100% of your prior year (2025) total tax. If your 2025 AGI was over $150,000, this becomes 110%.

Option 2 is the cheat code. Pull up your 2025 Form 1040, find Line 24 (Total Tax), divide by four, and pay that amount on each quarterly deadline. You’re now penalty-proof for 2026, no matter what happens to your income. If you tripled your income this year, you’ll owe a big balance in April 2027. But you won’t owe a penalty on top of it. That’s the difference safe harbor makes.

Worked example. Your 2025 Form 1040 Line 24 shows $14,800 in total tax, and your 2025 AGI was $87,000 (under the $150K threshold). Your safe harbor target is $14,800 ÷ 4 = $3,700 per quarter. Pay that on April 15, June 15, September 15, and January 15. Done. The IRS cannot assess an underpayment penalty against you.

Two important caveats. Safe harbor protects you from the underpayment penalty. It does not protect your cash flow. If your income jumps from $60,000 to $130,000, you owe the full new tax bill at filing time, just without the penalty. Set aside extra in a tax savings account regardless. And safe harbor only works if you actually pay each quarter. Skipping Q1 and Q2 to catch up in Q3 doesn’t qualify.

The two payment methods worth using in 2026

The IRS offers seven ways to pay quarterly. Six of them are obsolete. Use one of these two:

IRS Direct Pay (best for most freelancers)

Go to irs.gov/payments/direct-pay. Click “Make a Payment.” Select reason “Estimated Tax.” Choose Form 1040-ES. Pick the tax year (2026). Verify your identity using a prior tax return. Enter your bank account and routing numbers. Pay. You get an email confirmation and a confirmation number. Save both. Keep them. The IRS occasionally claims people missed payments, and that confirmation number is your proof.

Direct Pay is free. It takes about three minutes once your bank info is saved. It processes same-day if you submit by 8pm Eastern. No login required.

EFTPS (best if you want to schedule all four quarters in January)

The Electronic Federal Tax Payment System lets you schedule payments up to 365 days in advance. Sign up at eftps.gov. The IRS mails you an enrollment PIN within five to seven business days. After that, you can log in and queue all four 2026 estimated payments in one sitting in January. Then forget them until they auto-debit on the deadlines.

Most freelancers I talk to do this in early January for the year ahead, using their prior-year safe harbor amount. It removes the deadline anxiety and the “did I forget?” question entirely. The signup friction is real (the mailed PIN takes a week), but the time saved across the year is worth it.

Skip these payment methods. Paying by mail with a 1040-ES voucher is slow, gives no confirmation, and is easy to lose. Paying by credit card charges a 1.75% to 1.85% processing fee, which on a $4,000 quarterly payment is $70 to $74 you don’t need to spend. Paying through tax software often layers an extra fee on top of what’s free directly through the IRS.

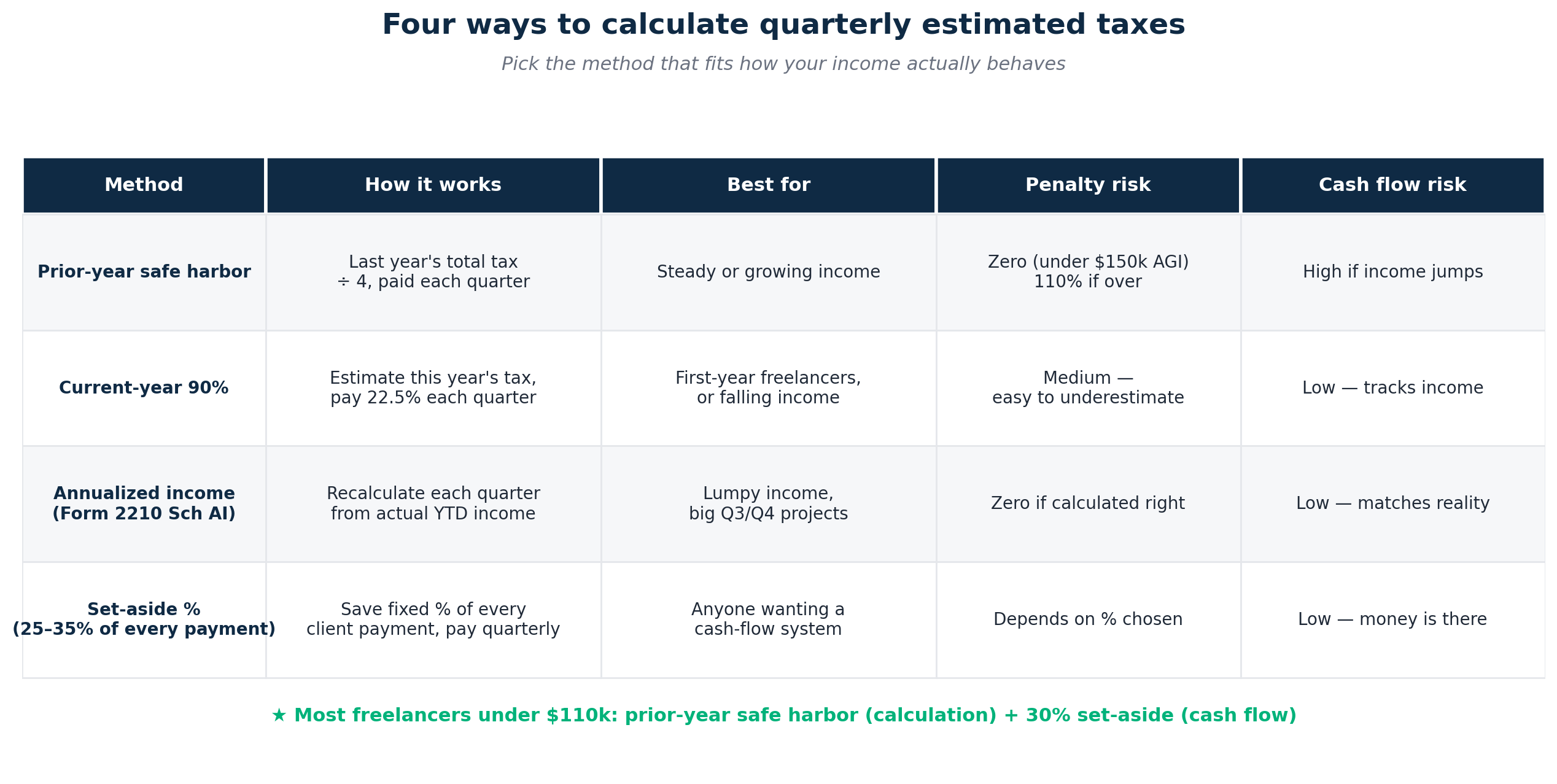

A side-by-side comparison of the four quarterly methods

Most articles tell you to “pick a method and stick with it” without showing what the methods actually do to your bill. Here’s the comparison freelancer guides skip:

| Method | How it works | Best for | Penalty risk | Cash flow risk |

|---|---|---|---|---|

| Prior-year safe harbor | Take last year’s total tax, divide by 4, pay that each quarter. | Steady or growing income, where last year is a fair baseline. | Zero, if AGI was under $150K (110% if over). | High if income jumps. Big balance due in April. |

| Current-year 90% | Estimate this year’s full tax, pay 22.5% each quarter. | First-year freelancers with no prior return to use, or those whose income dropped sharply. | Medium. Easy to underestimate. | Low. Tracks current income. |

| Quarter-by-quarter (annualized income) | Recalculate each quarter based on actual YTD income using Form 2210 Schedule AI. | Highly uneven income. Big projects in Q3 or Q4. | Zero if calculated correctly. | Low. Matches actual cash flow. |

| Set-aside percentage | Save 25% to 35% of every payment received, pay quarterly from that account. | Anyone who wants a system, regardless of which calculation method they use. | Depends on percentage chosen. | Low. Money is always there. |

The combination most freelancers under $110,000 actually want: prior-year safe harbor for the calculation, plus a 30% set-aside system for the cash flow. You stay penalty-proof and you have the money when each deadline hits.

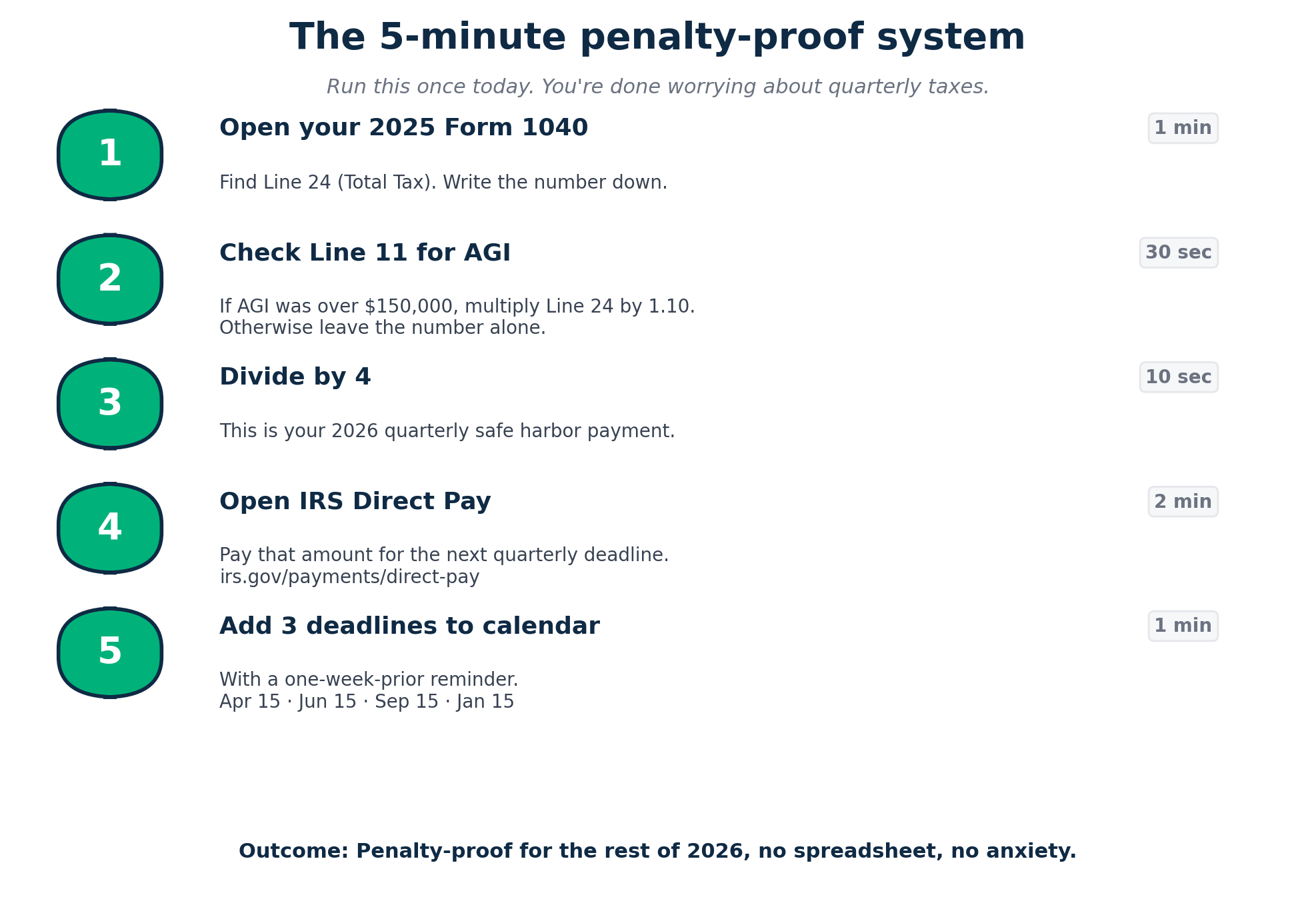

How to file quarterly estimated taxes as a freelancer: a 5-minute decision framework

If you only have five minutes, here’s what to do right now:

- Step 1. Open your 2025 Form 1040. Find Line 24 (Total Tax). Write the number down.

- Step 2. Check Line 11 of that same return for AGI. If it was over $150,000, multiply Line 24 by 1.10. Otherwise leave it.

- Step 3. Divide that number by 4. This is your 2026 quarterly safe harbor payment.

- Step 4. Open IRS Direct Pay. Pay that amount for the next upcoming quarterly deadline.

- Step 5. Add the next three deadlines to your calendar with a one-week-prior reminder.

That’s the complete system. Five minutes, penalty-proof, no spreadsheet. The optimization comes later, once you have a baseline running.

The mistake that costs freelancers thousands: forgetting SE tax

This is the single biggest error in first-year freelance tax planning. It shows up in every Reddit thread on r/freelance and r/tax around April. A freelancer earns $80,000, sees they’re in the 12% federal bracket, sets aside roughly $9,600, and panics in April when the actual bill is closer to $20,000.

The missing piece is the 15.3% SE tax, which is a separate tax from federal income tax. As a W-2 employee, your employer paid half of FICA (7.65%) and you paid the other half through payroll deductions you barely noticed. As a freelancer, you pay both halves on Schedule SE. On $80,000 of net SE income, that’s roughly $11,304 in SE tax alone, before a single dollar of income tax.

The fix. When you estimate your tax burden, always start with SE tax (15.3% of 92.35% of net SE income), then add income tax on top. For most freelancers between $45,000 and $110,000, total federal effective rate lands between 22% and 28% of gross 1099 income, which is why the “set aside 25 to 30 percent” rule lands roughly right. It’s not magic. It’s the math.

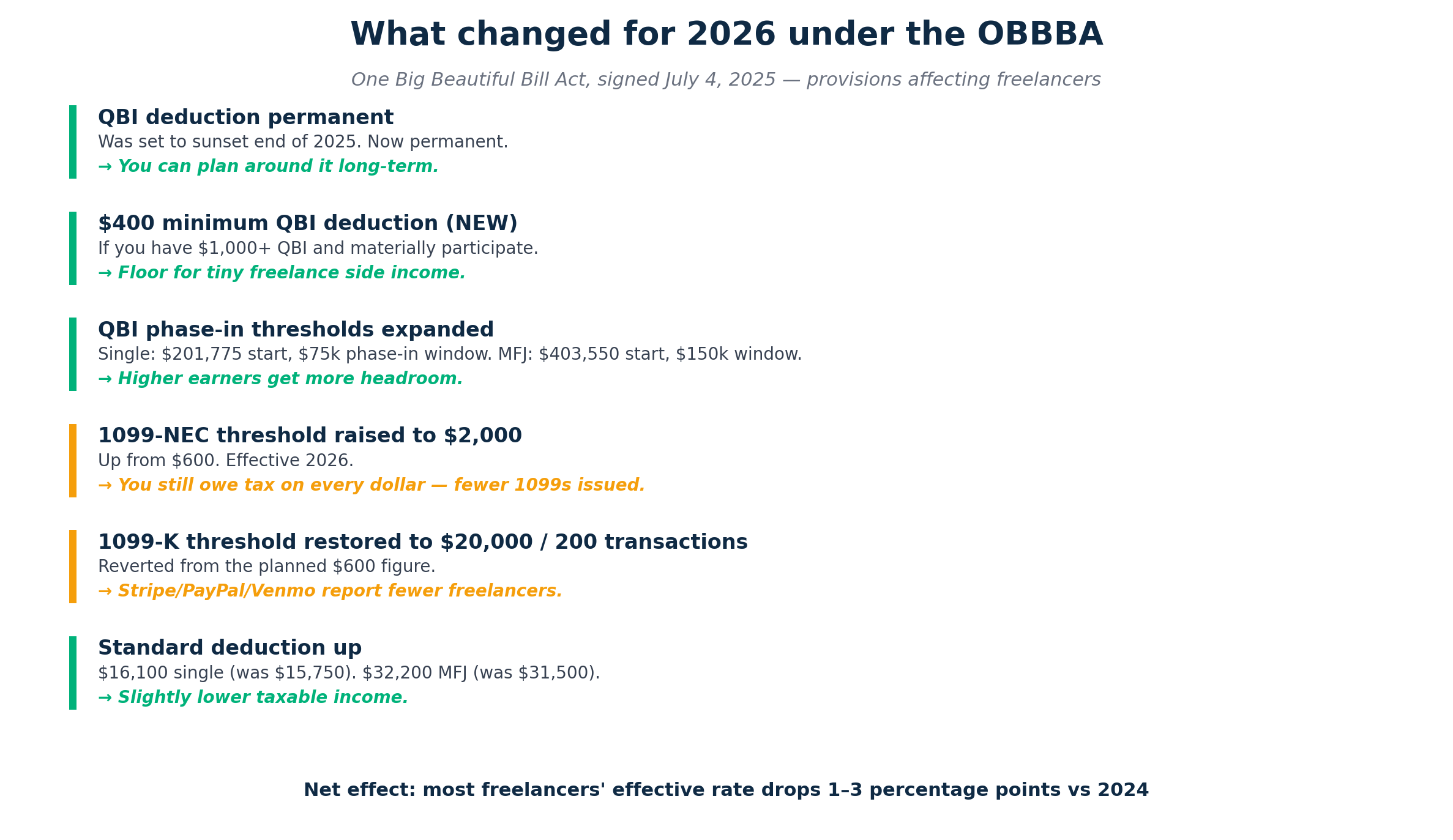

What changed for 2026 under the OBBBA

The One Big Beautiful Bill Act was signed July 4, 2025. Several provisions affect what you owe and how you plan estimated taxes for 2026.

- QBI deduction is permanent. The 20% Section 199A deduction was scheduled to sunset at the end of 2025. OBBBA made it permanent. You can build long-term planning around it.

- $400 minimum QBI deduction (new for 2026). If you have at least $1,000 of QBI and materially participate, you get at least $400, regardless of the standard 20% calculation.

- Phase-in thresholds expanded. The QBI phase-in range now starts at $201,775 (single) and $403,550 (married filing jointly) for 2026, with a wider phase-in window of $75,000 (single) and $150,000 (MFJ).

- 1099-NEC reporting threshold raised. Starting in 2026, clients only have to issue you a 1099-NEC for payments of $2,000 or more in a year, up from $600. You still owe tax on every dollar regardless of whether a 1099 shows up. The change matters because freelancers sometimes used 1099 receipt as a memory trigger for income they had forgotten to record.

- 1099-K threshold restored. The reporting threshold for third-party payment platforms (Stripe, PayPal, Venmo for business) reverted to $20,000 and 200 transactions, up from the $600 figure that was scheduled to take effect.

- Standard deduction increased. 2026 standard deduction is $16,100 (single) and $32,200 (married filing jointly), up from $15,750 and $31,500 in 2025.

None of these changes flip the basic system. You still owe quarterly estimates. The deadlines are still uneven. SE tax is still 15.3%. But the QBI permanence and the higher standard deduction together reduce most freelancers’ effective rate by 1 to 3 percentage points compared to 2024 calculations. Worth recalibrating any old “set aside 30%” rule you’ve been running.

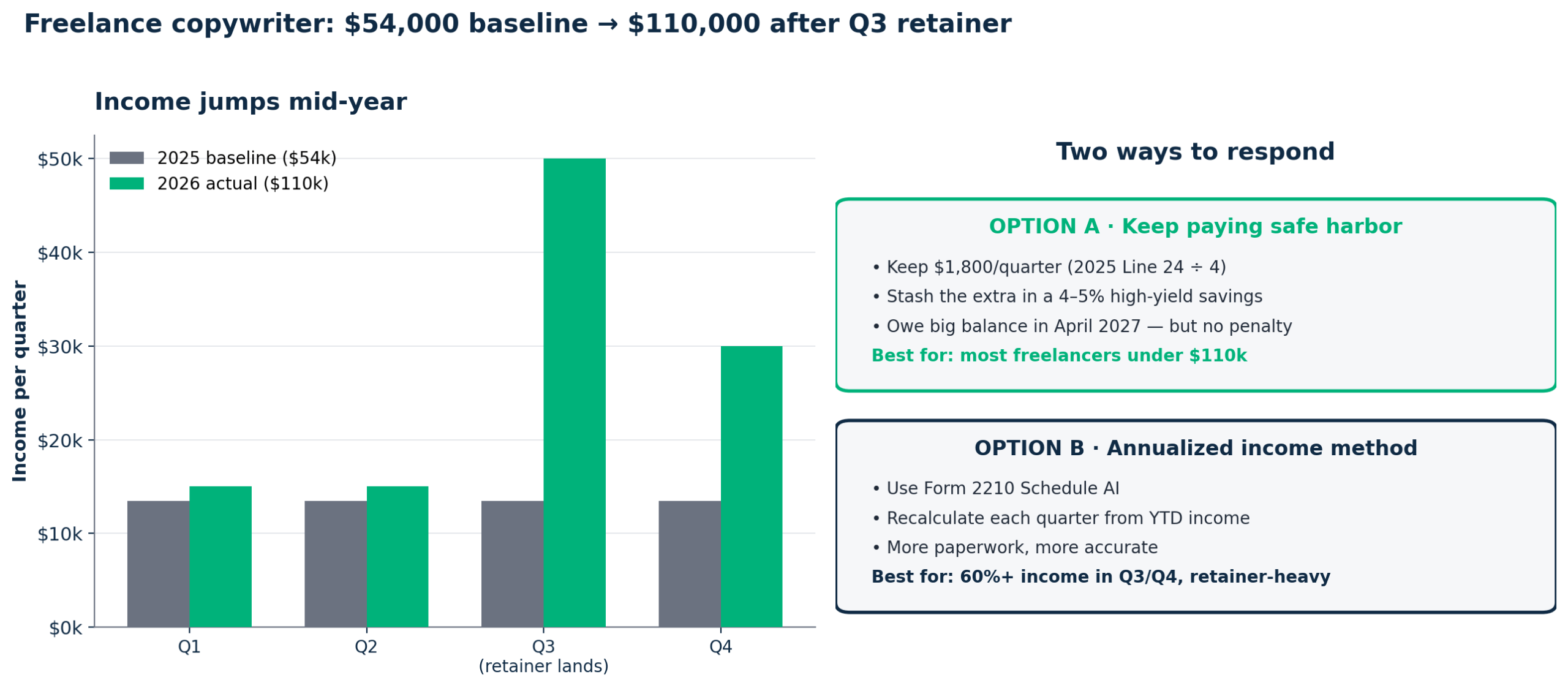

What to do when your income jumps mid-year

Picture a freelance copywriter making $54,000 in 2025. They land a $40,000 retainer in Q3 of 2026, pushing projected income to $110,000. Their prior-year safe harbor target was $1,800 per quarter. They’re now drastically underpaying for the actual tax owed, even though they’re penalty-proof.

Two options. First (simpler): keep paying the safe harbor amount. Accept that you’ll owe a large balance in April 2027. Stash the difference in a high-yield savings account earning interest until then. This is fine. You have no penalty and you keep your cash working until tax day.

Second (more accurate): switch to the annualized income installment method using Form 2210 Schedule AI. This lets you recalculate each quarter based on actual year-to-date income. If you earned $20,000 in Q1 and $50,000 in Q3, you pay tax on each quarter’s actual share rather than four equal installments. Annoying paperwork. Useful when income is genuinely lumpy.

For most freelancers under $110,000 with a steady client base, option one is enough. The annualized method is mostly worth it for retainer-heavy or seasonal businesses where Q3 or Q4 carries 60% or more of the year’s income.

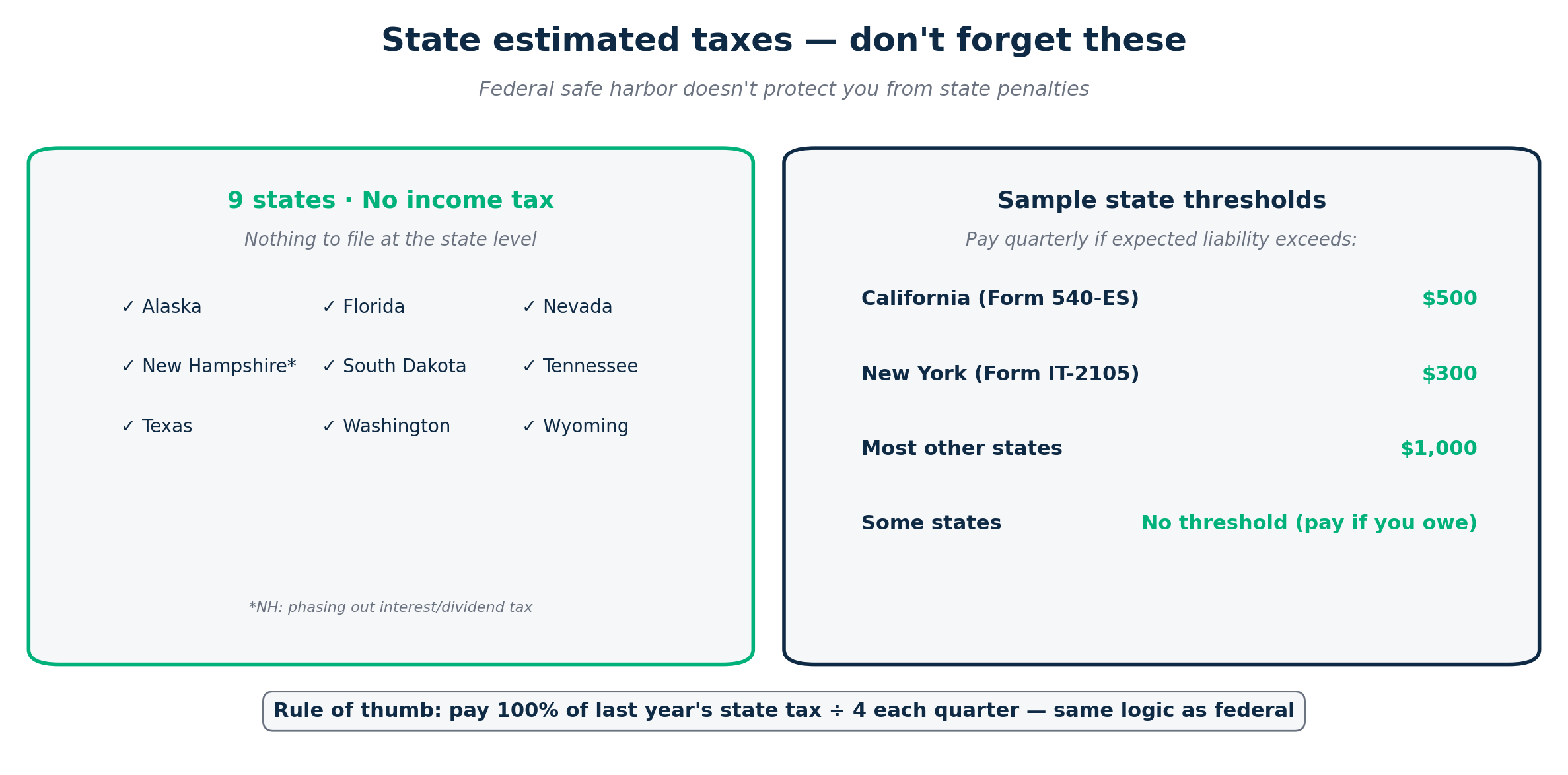

State estimated taxes (do not forget these)

Federal estimated taxes are only half the picture. If you live in one of the 41 states with an income tax, you owe state estimated taxes too. Usually on a similar quarterly schedule, but with different forms, different thresholds, and different payment portals. California’s threshold is $500 in expected liability. New York’s is $300. Most other states peg theirs at $1,000 or have no separate threshold (you pay if you owe).

State tax surprises are common because freelancers focus on the IRS, hit safe harbor at the federal level, then get hit with a state penalty in April. Check your state revenue department’s website for the exact form (in California, it’s Form 540-ES; in New York, IT-2105) and the same-quarter deadlines. State payments can usually be made online through the state’s portal, with the same logic as federal: pay 100% of last year’s state tax divided by four, and you’re penalty-proof.

Nine states have no income tax and so no state estimated payments to worry about: Alaska, Florida, Nevada, New Hampshire (interest and dividends only, and even that is being phased out), South Dakota, Tennessee, Texas, Washington, and Wyoming.

Tools to file quarterly estimated taxes as a freelancer (and skip the math)

If you want a tool to estimate quarterly payments and track the deductions that feed into them, you have two flavors of options. Accounting software like FreshBooks or Xero gives you a clean profit-and-loss view but doesn’t auto-calculate estimated taxes. You still need a separate calculator or a CPA to translate that profit number into a quarterly payment. My FreshBooks vs Xero comparison for 2026 covers which one fits a solo freelancer better.

The other flavor is AI-driven tax tools that promise to track deductions and surface a quarterly number for you. Two come up most often: Keeper Tax and FlyFin. Both work better in theory than in practice for many freelancers. The user reviews tell a more honest story than the marketing pages. If you’re weighing them, my Keeper Tax review and FlyFin review walk through what each tool actually does (and doesn’t do). The FlyFin vs Keeper Tax comparison sets them side by side based on real user feedback.

Honest take. For quarterly estimated taxes specifically, none of these tools beats the five-minute prior-year safe harbor method. Where they earn their fee is on the deduction-tracking side, not the quarterly calculation side.

Get the free quarterly tax checklist (with safe harbor calculator)

Drop your email below and you’ll get the same one-page checklist I use every quarter. It includes the four 2026 deadlines, a fillable safe harbor calculator (just enter your prior year’s Line 24), the Direct Pay step-by-step, and a 30% set-aside tracker that fits on a single page. No fluff, no upsell, no spam.

Frequently Asked Questions

How much should I set aside for taxes as a freelancer in 2026?

For most freelancers earning between $45,000 and $110,000 with no other income, set aside 25% to 30% of every client payment in a separate tax savings account. That covers federal income tax, the 15.3% self-employment tax, and a buffer. If you have sizeable business deductions or qualify for a full QBI deduction, the lower end (25%) is often enough. If you live in a state with income tax, add another 4% to 6%. The most accurate way to set the percentage is to look at your prior year’s total federal tax (Form 1040, Line 24) divided by your gross 1099 income for that year. My 2026 set-aside calculator and math walkthrough goes deeper on this.

What happens if I miss a quarterly estimated tax payment?

You owe an underpayment penalty for that quarter, calculated daily at the federal short-term rate plus three percentage points. For Q1 2026 the rate was 7% annualized. Q2 dropped to 6%. The penalty applies even if you pay the missed amount later or if you pay your full balance with your annual return. Good news: missing a payment doesn’t stack into a worse penalty. Each quarter is calculated separately. If you missed Q1 by $3,000 and paid that on June 1 instead of April 15, the penalty would land at roughly $25 to $30. Annoying for sure. Not the kind of thing that ruins your year.

Can I pay all my estimated taxes in one lump sum at the start of the year?

Yes. The IRS lets you pay your full annual estimate by April 15 if you want to. This works well if your income is predictable and you have the cash. It also avoids any deadline risk for the rest of the year. The downside is opportunity cost. That money sits with the IRS instead of in your high-yield savings account or business operating account earning 4% to 5% interest. For most freelancers, paying quarterly is better. For those who genuinely cannot trust themselves to remember deadlines, the front-loaded option is a reasonable trade.

Do I need to pay quarterly estimated taxes in my first year of freelancing?

Maybe. If your prior year tax return showed zero total tax (because you were a student, a dependent, or had no income), you can skip estimated payments entirely for your first freelance year and pay everything with your annual return without penalty. If you had a W-2 job with withholding the prior year and now you’re freelance, you owe quarterly payments once your expected federal tax exceeds $1,000. The simplest route: estimate your full 2026 tax, divide by the remaining quarters in the year, and start paying from the next deadline.

What is the difference between Form 1040-ES and Form 1040?

Form 1040-ES is the IRS worksheet and payment voucher for estimated taxes. You use it during the year to calculate quarterly payments and submit them. You don’t file Form 1040-ES with your annual return. Form 1040 is your annual federal income tax return, due April 15 of the following year. It reports your full year’s income, deductions, and tax owed, and reconciles against the estimated payments you made during the year. If you used a safe harbor and overpaid, you get a refund or apply the overpayment to next year’s Q1 estimate. The full reconciliation lives on Schedule C, where your business income and deductions feed back into Form 1040.

Do I have to use IRS Form 1040-ES vouchers, or can I just pay online?

You don’t need to mail vouchers. Pay online through IRS Direct Pay or EFTPS and the IRS automatically credits the payment to your account. The Form 1040-ES vouchers exist for the small number of people who still mail checks. If you pay online, keep your confirmation number or screenshot the confirmation page. That’s your proof of payment if there’s ever a dispute.

If I have a W-2 job and freelance income, do I still owe quarterly taxes?

Maybe not. The IRS treats employer withholding as paid evenly across the year, regardless of when in the year it was actually withheld. So you can increase your W-2 withholding using a fresh Form W-4 to cover both your salary tax and your freelance tax, eliminating the need for separate quarterly payments. Use the IRS Tax Withholding Estimator to figure out the additional amount to withhold. Often easier than juggling quarterly deadlines, especially if your freelance income is unpredictable.

What is “safe harbor” and how does it work for freelancers?

Safe harbor is an IRS rule that protects you from the underpayment penalty if you pay enough estimated tax during the year, regardless of what you ultimately owe at filing. You meet safe harbor by paying either 90% of your current-year tax liability, or 100% of your prior-year tax (110% if your prior-year AGI exceeded $150,000), spread across the four quarterly deadlines. The prior-year option is simpler because you know the target amount in advance: just pull your last Form 1040, Line 24, and divide by four. Most freelancers use this method and never worry about the penalty.

The next concrete step: open your 2025 Form 1040, find Line 24, divide by four, and schedule that payment in EFTPS for the next quarterly deadline. Five minutes from now, you’ll be penalty-proof for the rest of 2026.

Start Your Free Trial with [Tool Name]

This article is for general informational purposes only and does not constitute tax or legal advice. Tax laws change frequently and individual situations vary. Verify current rules at IRS.gov and consult a qualified CPA or enrolled agent before making decisions based on this content. Figures cited reflect 2026 tax year provisions as of April 2026.

About the author

Gareth is an entrepreneur based in Dubai and the founder of AI Finance Tools for Freelancers. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide is researched from real user reviews, official documentation, and expert sources.