The best bank accounts for freelancers are not what big-bank ads tell you. Four banking apps want your freelance business. One of them won’t even let a sole proprietor sign up. Here’s how to figure out which fits your income, in plain language.

You finished a project. Client paid $4,200 into your personal checking. Two weeks later you’re staring at the statement and you genuinely cannot tell which $1,800 of grocery, gas, and Spotify charges were “yours” and which were business. April rolls around. You guess at deductions. You owe more than you saved. Again.

Mixing personal and business money in one account is the most expensive habit in freelancing. The fix takes about 15 minutes and costs zero dollars at three of the four banks below. The fourth has a tax-savings feature so specific to Schedule C filers that it deserves its own section.

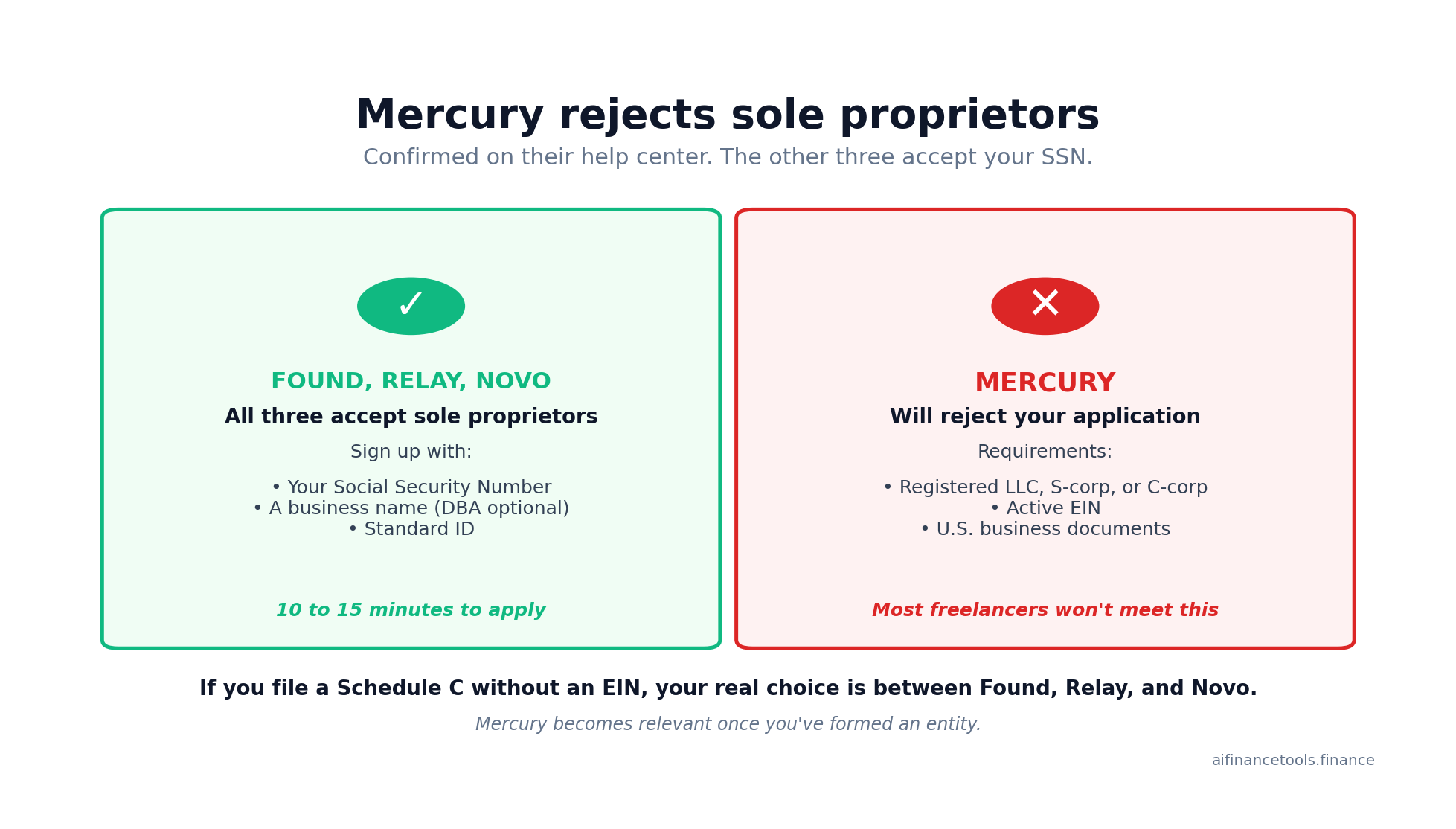

This is a side-by-side review of Found, Relay, Novo, and Mercury for US-based freelancers earning between $45,000 and $110,000 a year. All four are free to start. None of them are technically banks. They’re fintech platforms partnered with FDIC-insured institutions. Three will accept your sole proprietorship today. One won’t, and that single rule decides the answer for a lot of readers before any other feature matters.

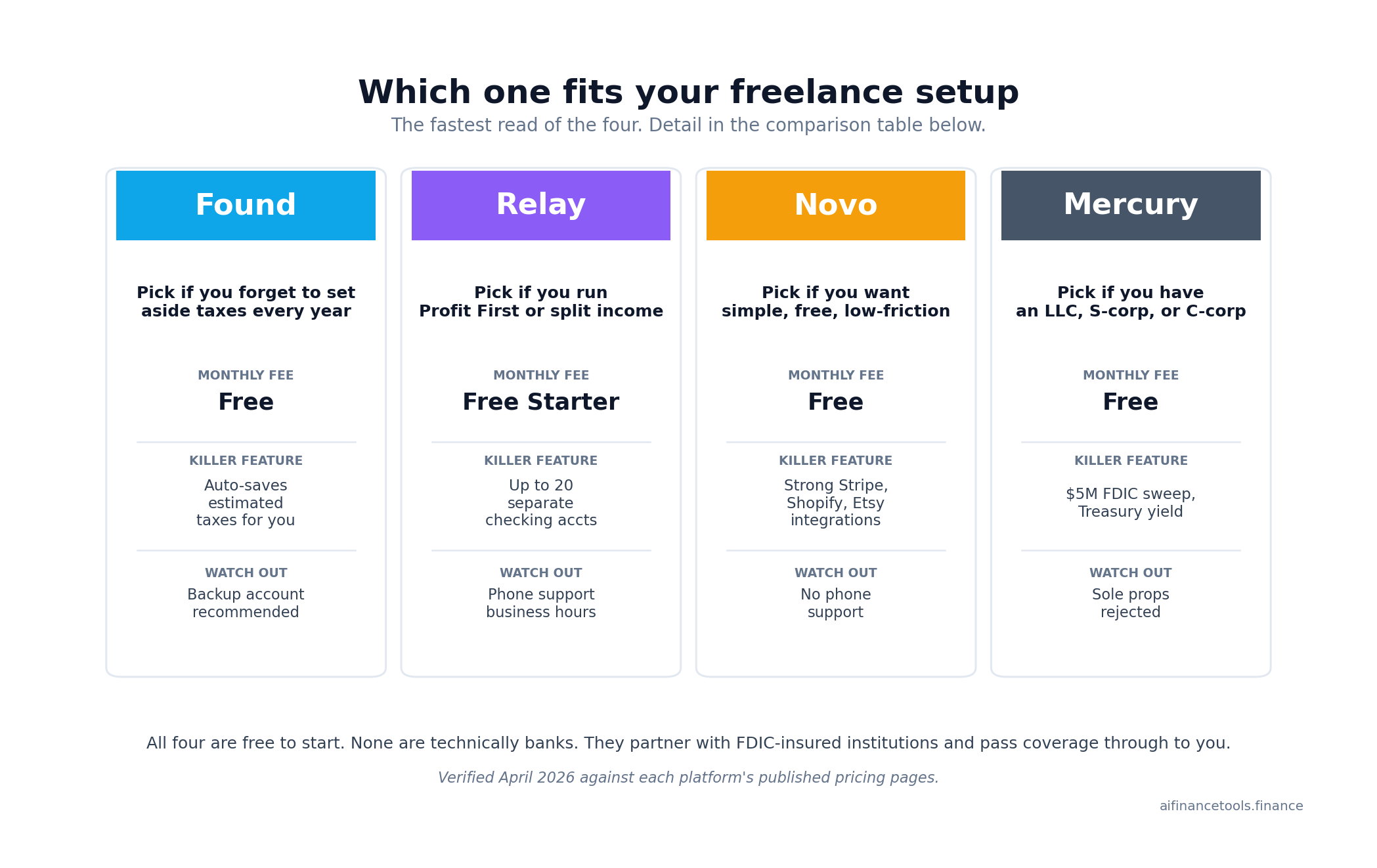

The fastest answer: best bank accounts for freelancers

If you file a Schedule C and don’t have an EIN, your real choice is between Found, Relay, and Novo. Mercury doesn’t accept sole proprietorships. They confirm this on their own help center.

- Pick Found if you want the bank to set aside your tax money for you and you’d rather skip a separate bookkeeping app.

- Pick Relay if you run Profit First or want separate sub-accounts for taxes, profit, owner’s pay, and operating costs, with FDIC coverage up to $3 million.

- Pick Novo if you want the simplest free checking account with strong app integrations (Stripe, Shopify, Etsy) and almost no fees.

- Pick Mercury only if you’ve formed an LLC, S-corp, or C-corp and you want $5M FDIC coverage plus a Treasury yield product.

The rest of this article is the work behind that summary, with the trade-offs nobody else seems to mention.

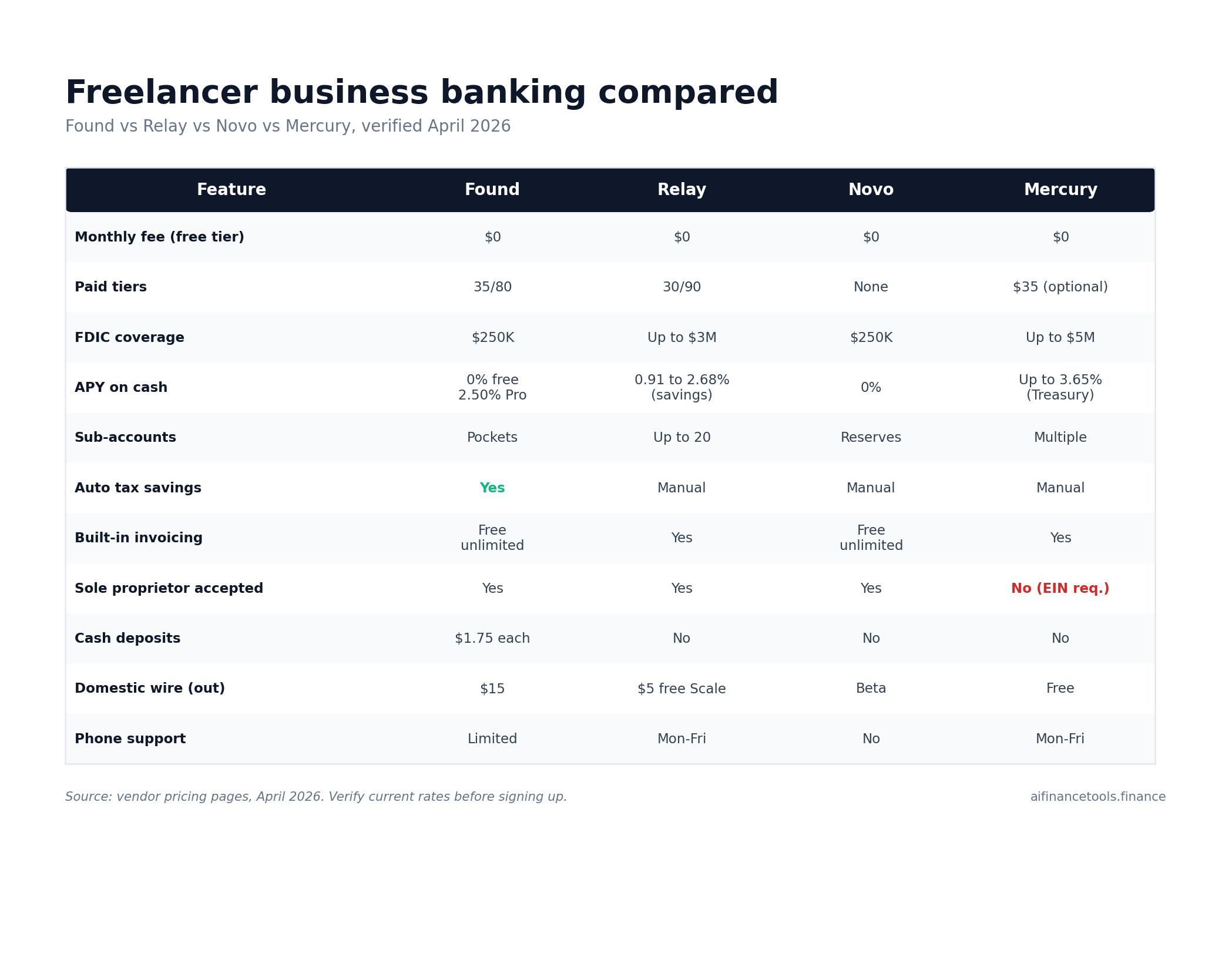

Side by side: what each account actually costs in 2026

Pricing pulled from each vendor’s official pricing or fee schedule page in April 2026. Verify before you sign up. Rates shift.

| Feature | Found | Relay | Novo | Mercury |

|---|---|---|---|---|

| Monthly fee (free tier) | $0 | $0 (Starter) | $0 | $0 |

| Paid tiers | Plus $35/mo, Pro $80/mo | Grow $30/mo, Scale $90/mo (regular $120) | None | Tea $35/mo (optional) |

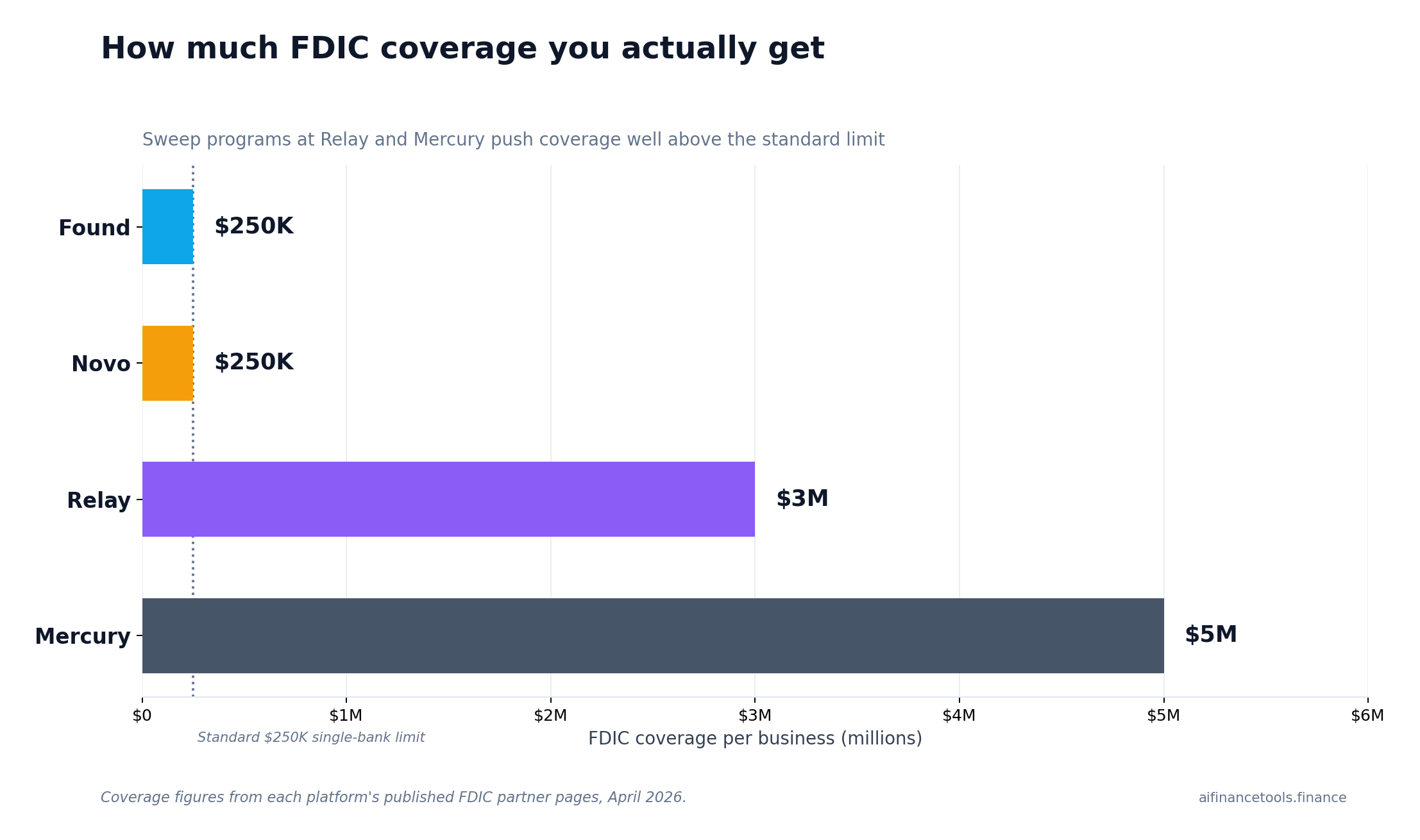

| FDIC coverage | $250,000 (Lead Bank) | Up to $3M (Thread Bank sweep) | $250,000 (Middlesex Federal) | Up to $5M (Choice/Column sweep) |

| APY on cash | 0% free; 1.50% Plus (cap $20K); 2.50% Pro | Savings only: 0.91% / 1.55% / 2.68% | 0% | 0% checking; up to ~3.65% Treasury (min $500K for best tier) |

| Sub-accounts | Pockets (sub-accounts with own routing) | Up to 20 separate checking accounts | “Reserves” within one account | Yes, multiple checking accounts |

| Auto tax savings | Yes, calculated from each deposit | Manual via separate “Taxes” account | Manual via Reserves | Manual |

| Built-in invoicing | Free, unlimited | Yes (improved on Scale) | Free, unlimited | Yes |

| Sole proprietor accepted? | Yes | Yes | Yes | No, EIN required |

| Cash deposits | Yes ($1.75 per deposit) | No | No (workaround: money order) | No |

| Outgoing domestic wire | $15 ($10 on Pro) | Free on Scale, otherwise $5 | Free (ACH); wires in beta | Free |

| QuickBooks / Xero sync | Yes (Plus tier for full sync) | Yes, all plans | Yes | Yes |

| Customer support | Phone (limited hours), in-app chat, email | Phone Mon-Fri 9-5 ET, email, chat | Email and in-app only | Phone Mon-Fri, email, chat |

One row in that table matters more than the rest: Sole proprietor accepted. If you read no further, read that line.

Found: the only one that does your tax math for you

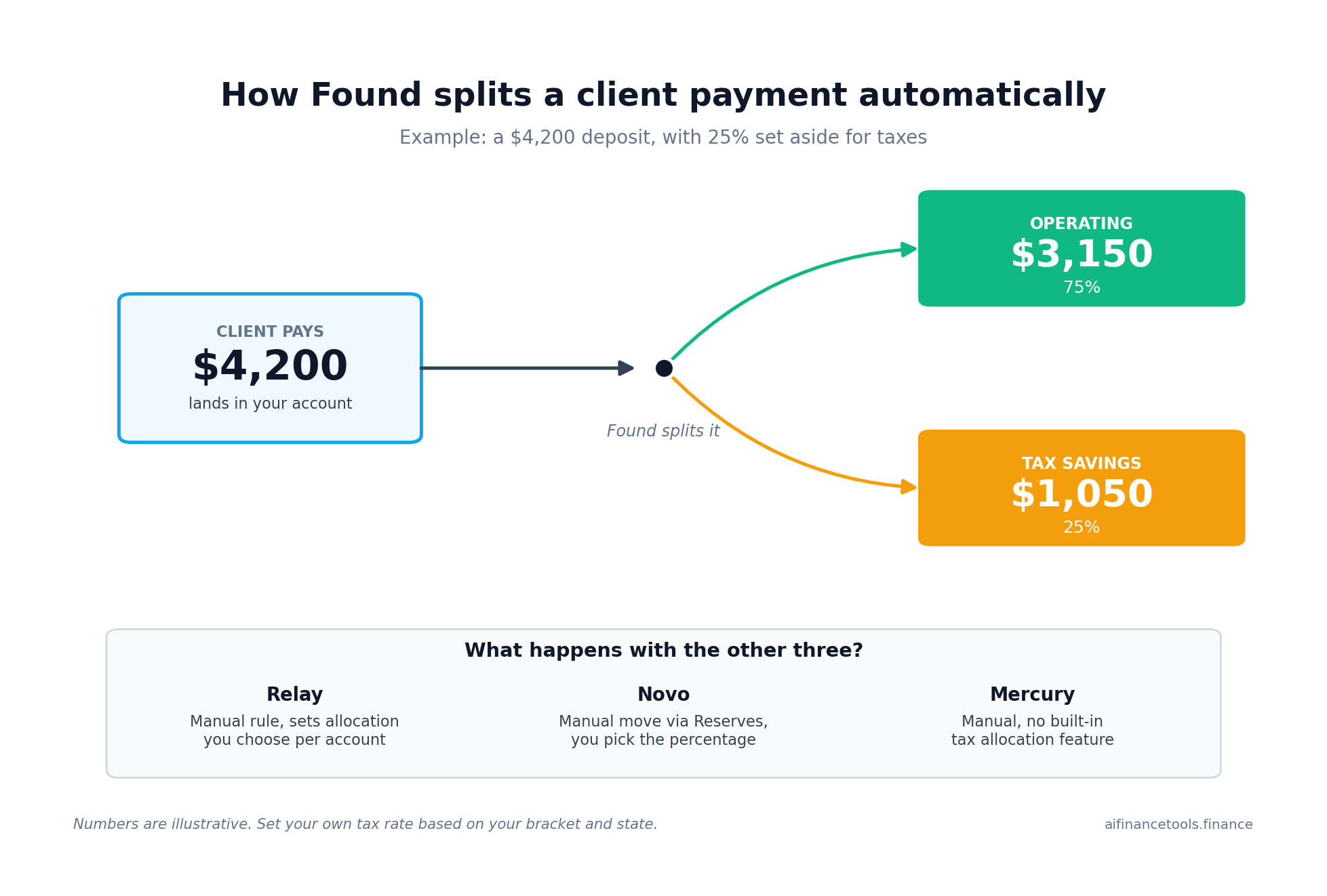

Found is built for one person. A solo writer, designer, photographer, developer, consultant. The kind of person filing a Schedule C and a Schedule SE every year. It pairs your business checking account with automatic expense categorization and a real-time tax estimate that updates every time money lands.

What you actually get on the free tier

The free Found account comes with a Mastercard business debit card, mobile check deposit, ACH transfers in and out, unlimited free invoicing with Stripe-powered card acceptance at 2.9% per transaction, expense categorization tagged to Schedule C lines, and an estimated tax bill that updates as you earn. You can collect W-9s from contractors and issue Form 1099-NEC at year-end inside the same app, with no per-contractor fee. Banking is through Lead Bank, Member FDIC, with $250,000 in coverage.

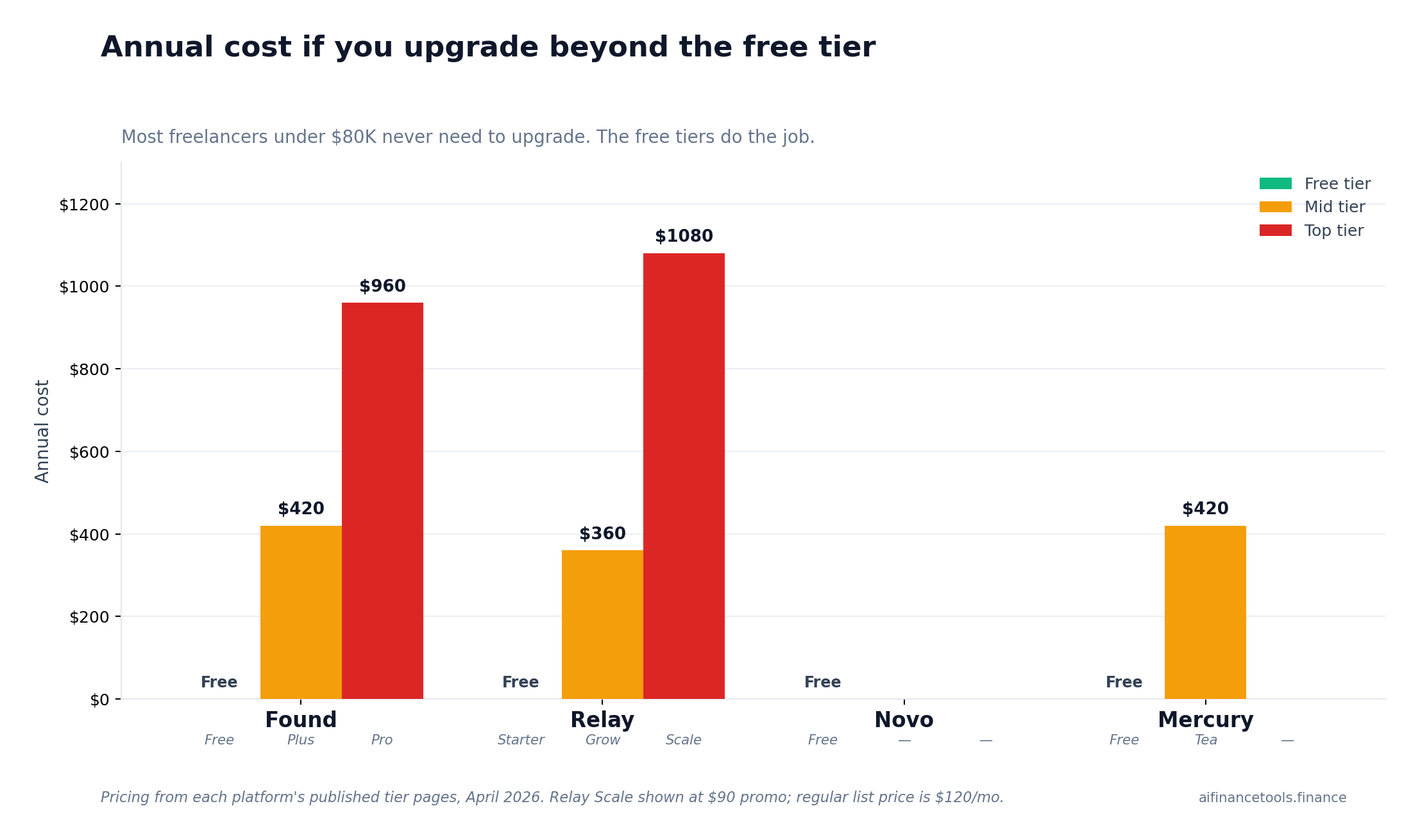

When Plus or Pro is worth paying for

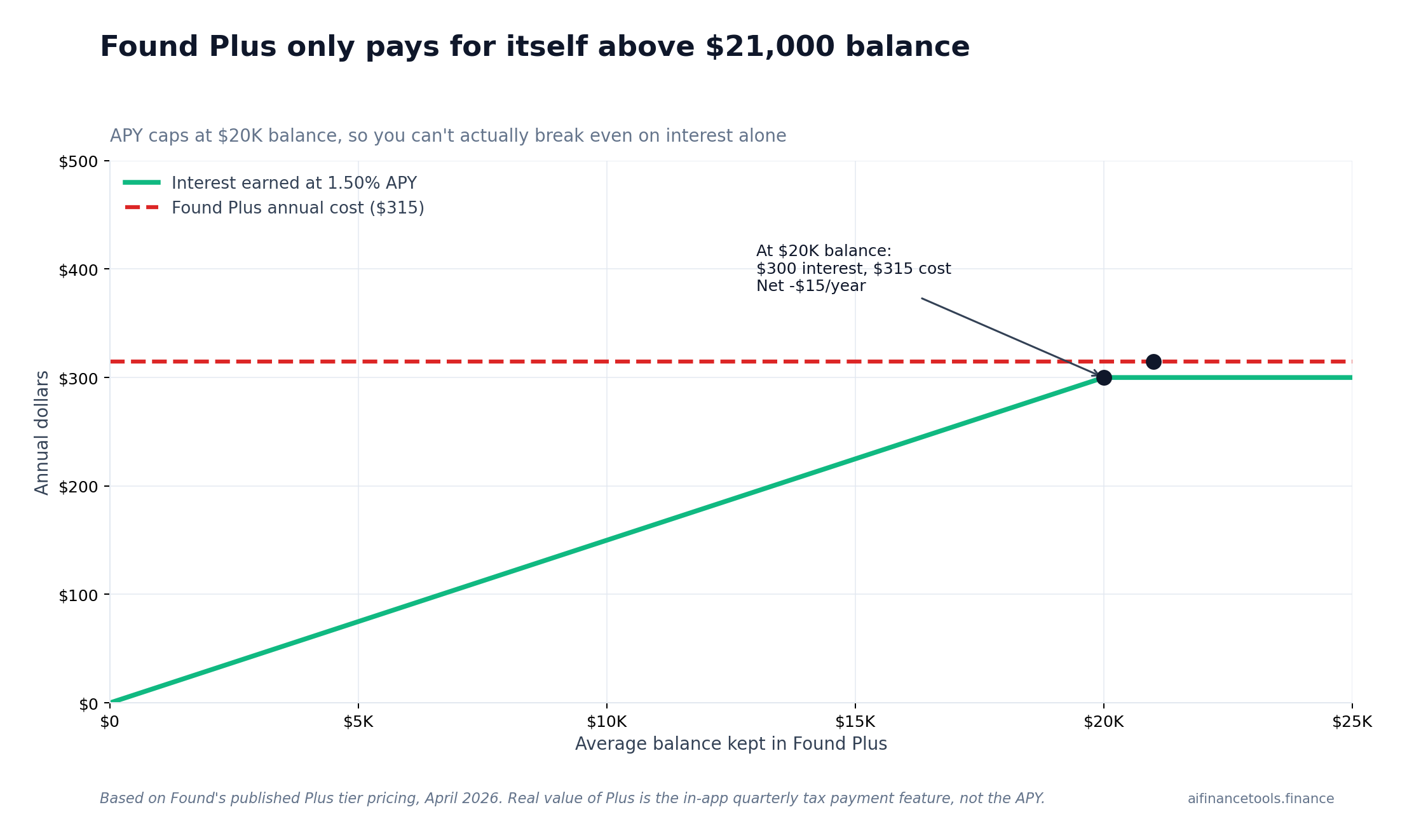

Found Plus costs $35 a month or $315 a year. It pays 1.50% APY on balances up to $20,000, lets you pay your federal quarterly estimated taxes from inside the app, and unlocks better expense reports. Found Pro is $80 a month or $720 a year with 2.50% APY on all balances and 1% cash back on debit purchases.

Run the math before you upgrade. At a $20,000 balance, Plus pays around $300 a year in interest. That’s roughly the cost of the subscription itself. The tax-payment feature is the real reason to upgrade, not the APY. If you regularly miss your quarterly estimated tax deadlines, the in-app payment is genuinely useful. If you don’t, stay on the free tier.

The risks Found’s marketing doesn’t mention

Trustpilot scores Found at 4.5 across 1,283+ reviews as of April 2026, but the negative pattern is consistent. Reviewers describe sudden account closures with funds returned by paper check weeks later. The Better Business Bureau has logged dozens of complaints about accounts frozen during compliance reviews with limited phone support during the freeze.

Found is not the wrong choice. But it is the wrong only choice. Keep a backup checking account at a separate institution so you’re not locked out of your own working capital if a review hits at the wrong moment.

Practical fees that add up: instant transfers cost 1.75%, outgoing domestic wires are $15, and there’s a $10 dormancy fee after 12 months of inactivity. Cash deposits run $1.75 each.

Relay: built for people who run Profit First or want real account separation

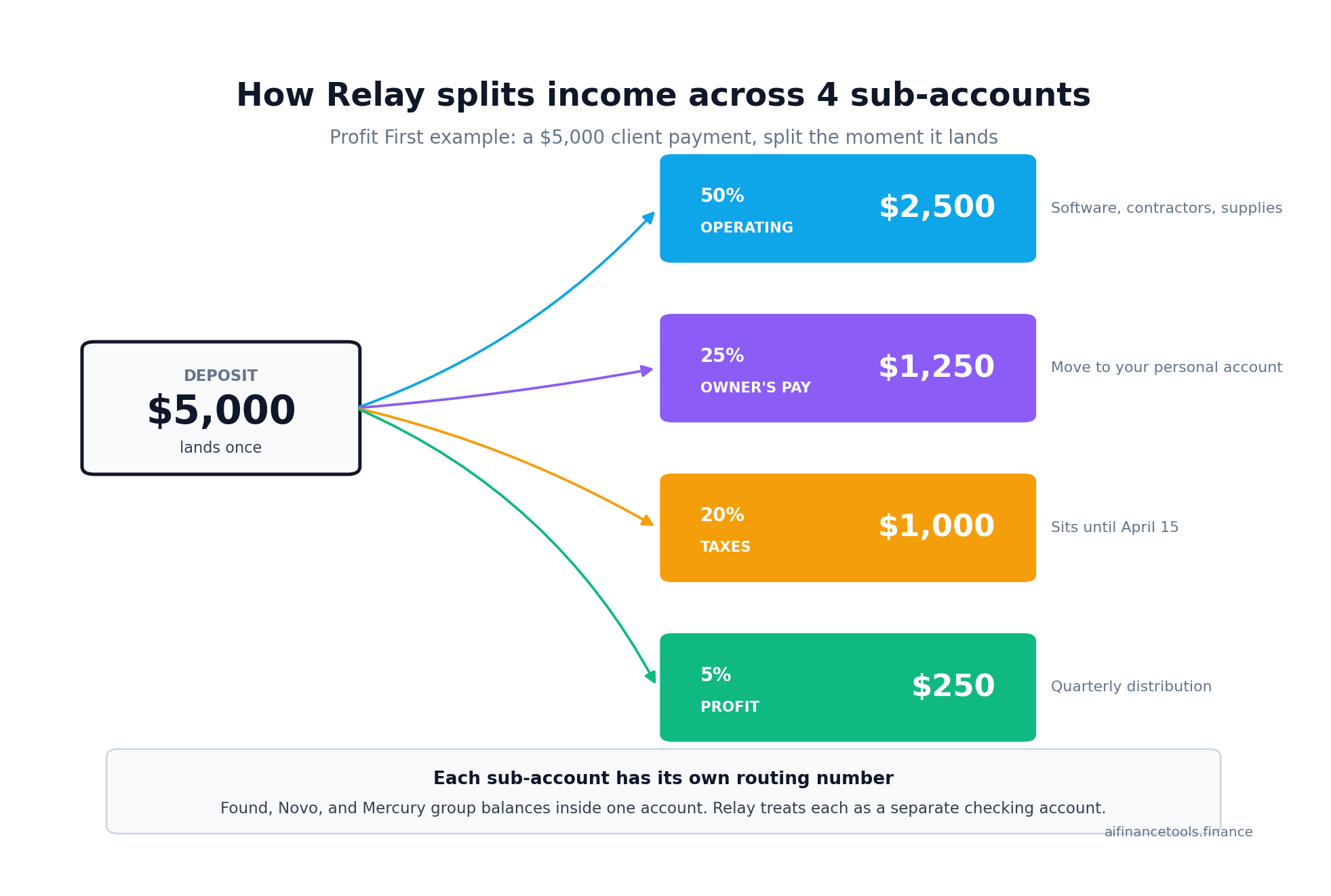

Relay’s pitch is structural. You don’t get one account with mental sub-buckets. You get up to 20 separate checking accounts under one login, each with its own account number and routing number. That distinction matters. You can set automated transfer rules so 25% of every incoming payment moves to a “Taxes” account, 10% to “Profit,” 50% to “Operating,” and so on, the moment money lands.

Pricing that’s honest about its tiers

Starter is genuinely free with no minimum balance, no overdraft fees, free incoming wires, and 0.91% APY on the savings account. Grow is $30 a month and bumps savings APY to 1.55%, adds bill pay automation, faster ACH transfers, and accounting integrations. Scale is $90 a month (promotional, listed at $120 regular) and pays 2.68% APY on savings plus free outgoing domestic wires and AI-powered cash flow tools. Banking is through Thread Bank, Member FDIC, with deposits insured up to $3 million through the partner sweep program.

The Thread Bank thing you should know about

In 2024 the FDIC issued a consent order against Thread Bank, Relay’s partner, requiring stronger fraud monitoring and customer due diligence in its Banking-as-a-Service program. The order was terminated in December 2025. Customer funds were never at risk and remain FDIC-insured. The practical effect during the order period was an uptick in compliance-related account freezes that some Reddit users on r/smallbusiness and r/freelance still describe in 2026 threads. Relay launched a dedicated Account Protection Team in 2026 to respond to these cases. The pattern is improving. Worth knowing about regardless.

Who Relay is genuinely the best fit for

You earn $80,000 or more a year, you’ve read Mike Michalowicz’s Profit First, and you want allocations to happen automatically. Or you handle multiple income streams (a retainer client, a few one-off projects, a digital product) and you want to see at a glance what’s funding what. Relay’s free tier alone outclasses most of what big banks call “business checking.” For a step-by-step on splitting your income across separate accounts the moment it lands, see our guide to managing freelance cash flow.

Novo: the simplest answer if you just want the basics done right

Novo isn’t trying to do tax automation or run your Profit First system. It’s free business checking with a clean app, strong third-party integrations, and almost no fees. That’s it. For a Schedule C filer who already uses Wave or QuickBooks for bookkeeping and just wants a place to keep business money separate, Novo is often the right call. Pair it with one of the tools from our best accounting software for freelancers roundup and you have a complete setup for under $30 a month.

What you get

No monthly fee. No minimum balance. No transaction fees. Free ACH in and out. Free incoming wires. Up to $7 a month in third-party ATM fee refunds. Free unlimited invoicing with ACH and PayPal acceptance built in. Direct integrations with Stripe, Shopify, Square, QuickBooks, Xero, and Wise. Banking is through Middlesex Federal Savings, Member FDIC, with the standard $250,000 in coverage.

Where Novo will frustrate you

Customer support is email and in-app chat only. No phone. NerdWallet’s review and multiple BBB complaints flag this as the most common pain point. If your card gets locked while you’re trying to pay a vendor, your fastest fix is in-app chat.

Novo also pays 0% on checking balances. At $30,000 average balance you’re leaving roughly $400 to $800 a year in interest on the table compared to Bluevine, American Express Business Checking, or even Found Plus. There are no cash deposits, and outbound wires are still in limited beta as of early 2026. If you take cash from clients regularly, Novo isn’t a fit.

Reddit threads on r/smallbusiness from late 2025 and early 2026 describe Novo as “boring in a good way” and “the bank that just works.” That’s a fair summary. It’s the option for the freelancer who wants to stop thinking about banking and get back to the work.

Mercury: powerful, but not for sole proprietors

Mercury’s own help center confirms it: Mercury does not open accounts for sole proprietorships. If you file a Schedule C as an unincorporated freelancer with no EIN, you cannot open a Mercury account. Stop reading this section and go back to Found, Relay, or Novo. If you’ve formed an LLC, S-corp, or C-corp and have an EIN, the rest of this section is for you.

Why entity-formed freelancers like Mercury

Mercury offers $0 monthly fees, $0 ACH and domestic wire fees, and FDIC coverage up to $5 million through its sweep program with Choice Financial Group and Column N.A. That’s the highest pass-through coverage in this comparison and roughly 20 times the standard $250,000 single-bank limit.

Mercury Treasury, available with larger balances (typically $500,000 and up), invests idle cash into government money market funds and Treasury bills with yields recently in the 3.5% to 3.65% range. The IO credit card pays 1.5% cash back on all spend with no personal guarantee.

The realistic warning

Mercury depends on partner banks, and two of those partners have been the subject of FDIC enforcement actions in recent years (Choice Financial Group in 2023 and Evolve Bank & Trust in 2024). Mercury ended its relationship with Evolve. Federal enforcement actions are rare, and they don’t mean a bank will fail. They do mean regulators have concerns about how a partner bank monitors fintech-driven accounts, which has historically translated into more compliance freezes for end users. Like any neobank, keep a backup account elsewhere.

If you’re not sure whether forming an LLC is worth it for your freelance income yet, that’s a separate calculation. Cost of formation, ongoing state fees, payroll headaches if you elect S-corp status, and the income level at which the tax savings actually exceed the admin cost are all worth working through. Most freelancers earning under $80,000 a year don’t need to bother. Above that, the math gets more interesting. If you’re weighing it up, our freelance tax deductions guide covers what changes when you make the switch.

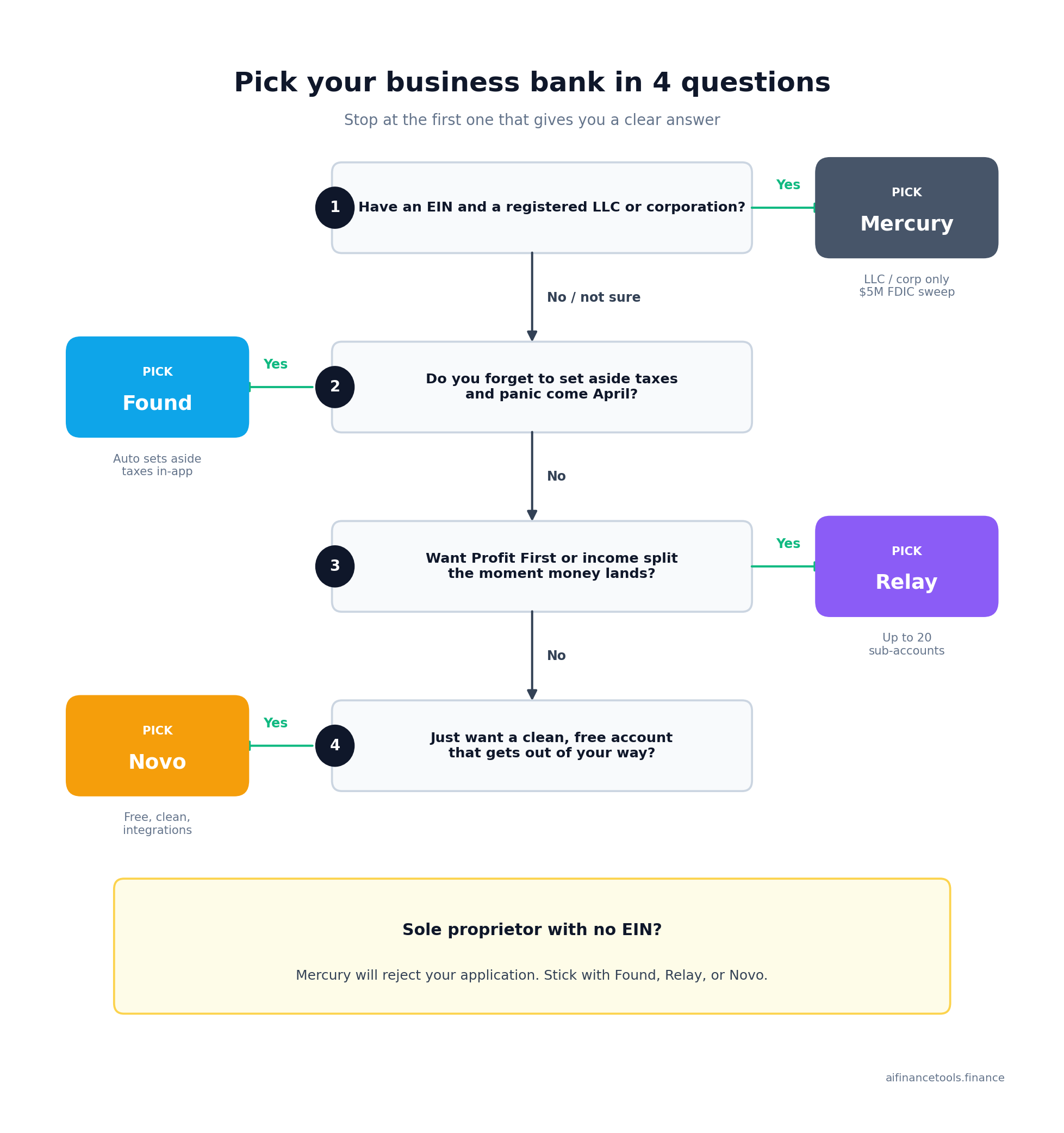

A 5-minute decision framework

Run through these four questions in order. Stop at the first one that gives you a clear answer.

- Do you have an EIN and a registered LLC or corporation? If no, drop Mercury from your list. Move on.

- Do you regularly forget to set aside taxes and panic in April? Found’s auto-set-aside feature is the only one that does this work for you inside the bank account itself. Pick Found.

- Do you want to run Profit First or split income across multiple buckets the second it arrives? Pick Relay. Nothing else matches its sub-account structure.

- Do you just want a clean free business checking account that gets out of your way? Pick Novo.

That’s the framework. Most freelancers spend three weeks comparing fintech features and end up with the wrong account because they never asked these four questions in this order.

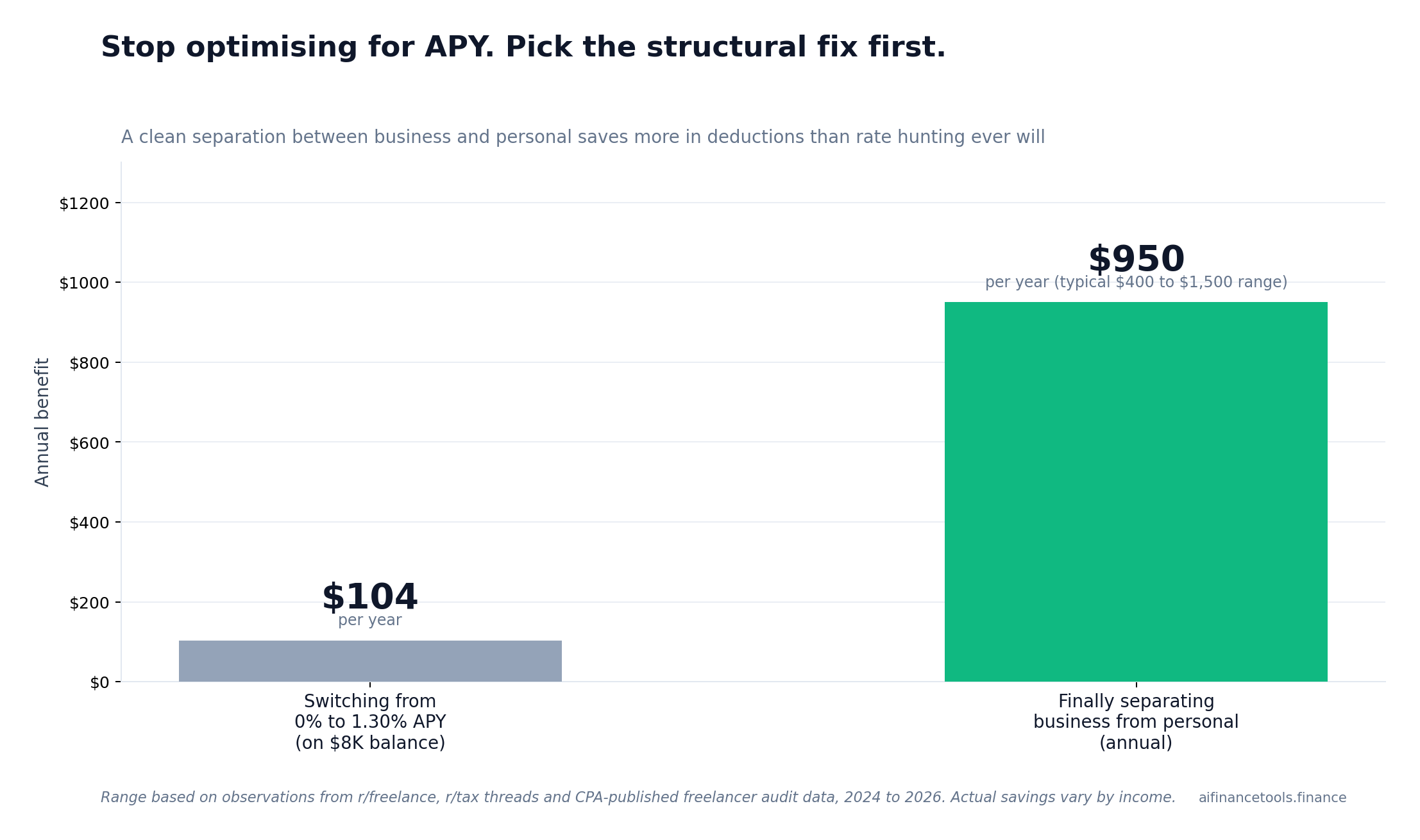

The mistake most freelancers make when picking

They optimize for APY. A freelancer keeping $8,000 average balance who switches from Novo (0% APY) to Bluevine (1.30% APY) earns about $104 a year. That’s real money, but it’s small money. The same freelancer who picks Relay or Found and finally separates business from personal cleanly will save $400 to $1,500 in missed deductions at tax time, every year.

Pick the structural fix first. Optimize for interest later, once you’re earning enough that the basis points actually matter. The same logic applies to wire fees, ATM rebates, and integration counts. Helpful, but secondary. The structural question (sole proprietor vs entity, single account vs sub-accounts, automatic tax savings vs manual) decides 90% of whether your banking will actually work for you 12 months from now. If you haven’t yet built a system for tracking business expenses end-to-end, sort that before you switch banks.

What real freelancers say in 2026

From recent threads on r/freelance, r/smallbusiness, and r/tax, plus Trustpilot pages for each platform:

- On Found: users praise the auto-tax-set-aside as the killer feature, especially first-year freelancers who got blindsided in April. The recurring complaint is sudden account closures with funds returned by check. That’s why “always have a backup account” comes up in nearly every Found thread.

- On Relay: Profit First adopters describe it as the only platform built for the system. The criticism is that the free Starter tier limits some advanced features that most paid competitors include for free.

- On Novo: the praise is consistent, “boring and reliable.” The criticism is consistent too, “support is email-only and that’s a problem when something breaks.”

- On Mercury: startup founders love the platform and the Treasury yield. Sole proprietors who got rejected at signup are often furious because nothing on the marketing pages flags the EIN-only requirement until you’re 8 minutes into the application.

The pattern that ties this all together

Every fintech in this comparison is a financial technology company, not a chartered bank. They partner with FDIC-insured institutions and pass that insurance through to you. That’s normal. The FDIC has clear guidance on it.

The practical implication: when something goes wrong, you’re navigating a fintech app’s support team and a partner bank’s compliance department at the same time. That’s why “keep a backup checking account at a separate institution” appears in every honest review of every neobank. Treat it as table stakes, not paranoia.

If you’re newer to freelance bookkeeping and want a complete starting system, our guide on tracking business expenses walks through how to set up categories that match Schedule C from day one. Our piece on avoiding tax liability shock covers the quarterly estimated payment math most freelancers get wrong in their first two years.

Free: the Freelancer Banking Switch Checklist

Switching business banks sounds annoying. It doesn’t have to be. The Freelancer Banking Switch Checklist is a one-page PDF that walks you through every step in order: which direct deposits to update, which subscriptions to redirect, how long to keep the old account open as a buffer, what records to download before you close it, and how to avoid the two-week gap that trips up most freelancers when they switch.

Frequently Asked Questions

Do I really need a separate business bank account if I’m a sole proprietor?

Legally, no. The IRS doesn’t require a sole proprietor to have a separate business account. Practically, yes. Mixing personal and business spending in one account is the single biggest reason freelancers underclaim deductions and overpay tax. A separate account also protects you if you ever choose to convert to an LLC, because lenders and the IRS treat commingled funds as evidence of a “non-business” operation. Spend 15 minutes opening one of the four accounts in this guide and you’ve solved one of the top three avoidable freelance tax mistakes.

Can I open Found, Relay, or Novo without an EIN?

Yes. All three accept sole proprietors using a Social Security Number instead of an EIN. Mercury is the exception, requiring an EIN tied to a registered entity. If you ever do form an LLC later, you can apply for an EIN free at IRS.gov in about 10 minutes, and you can update your existing Found, Relay, or Novo account rather than opening a new one.

What if my Found or Relay account gets frozen?

This is a real risk worth planning for, not a reason to avoid these platforms. Two practical defenses: keep a backup checking account at a different institution (a free credit union account works), and never let a single account hold more than 30 days of operating expenses if it’s a fintech platform. If a freeze happens, contact support immediately, document every interaction in writing, and ask for a written explanation of the review. Most freezes resolve within 7 to 21 days. The FDIC and CFPB have escalation paths if a freeze drags on longer.

Is the FDIC coverage on these accounts as safe as a regular bank?

Yes, with caveats. FDIC insurance protects you against the failure of an insured bank, up to coverage limits ($250,000 standard, higher with sweep programs). It does not protect you against the failure or fraud of the fintech middle layer. If a fintech goes bankrupt with your money inside but hasn’t lost the underlying bank deposits, recovery can take weeks or months even though your money is technically insured. The Synapse collapse in 2024 showed how this can play out, with more than 100,000 customers locked out of $265 million in deposits. The lesson isn’t to avoid fintechs. It’s to keep balances reasonable and a backup account active.

Which account is best for accepting client payments via Stripe or PayPal?

Novo and Found both have first-class Stripe integration. Novo Boost speeds Stripe payouts by up to 95% in many cases. Found’s invoice product uses Stripe under the hood and lets you accept card payments at 2.9% per transaction. Relay and Mercury both support Stripe and PayPal as payment processors but don’t have built-in invoicing as polished as Novo or Found. For more on standalone invoicing tools, see our best invoicing software for freelancers comparison.

Can I switch banks mid-year without messing up my taxes?

Yes. Download a CSV export of every transaction from your old account before you close it (all four platforms in this guide support this). Save it somewhere you’ll find it again next March. When you file taxes, you’ll combine the two accounts’ transactions in your bookkeeping software (or in a spreadsheet if you’re DIY-ing it). The IRS doesn’t care how many accounts you used during the year, only that you accurately report income and expenses. The Freelancer Banking Switch Checklist above covers this in more detail.

What about Bluevine, Lili, or Chase Business?

Bluevine is a strong fifth option with 1.30% APY on checking balances up to $250,000 (terms apply) and FDIC coverage up to $3 million through Coastal Community Bank. It didn’t make this comparison because it sits between Relay (cash flow control) and Mercury (high-balance treasury) without dominating either category for freelancers. Lili is closer to Found in design but has had more pricing changes than the others recently. Chase Business is the right answer if you take cash regularly and need branches, but Chase Business Complete carries a $15 monthly fee with several waiver paths (minimum balance, qualifying card spend, or eligible deposits), which most freelancers in the $45,000 to $80,000 income range will find easier to skip than to manage.

One thing to do this week

If you’re still running business income through your personal checking account, open one of the best bank accounts for freelancers in this guide today. The application takes 10 to 15 minutes. Update one client’s payment instructions to send to the new account. Move one recurring business subscription (your domain, Adobe, whatever) to the new debit card. That’s it. The full migration can wait. Starting the separation today means next April will be the first year you don’t dread reconciling 12 months of mixed transactions.

These are the best bank accounts for freelancers we could find in 2026 — but tax laws and fintech pricing change. The figures in this article were verified against vendor pricing pages and IRS guidance in April 2026. For your specific situation, verify current rates and confirm with a CPA before making decisions. This article is informational and not tax or legal advice.

About the author

Gareth is an entrepreneur based in Dubai and the founder of AI Finance Tools for Freelancers. He’s not a CPA or a bookkeeper. He built this site because he couldn’t find honest, thorough reviews of AI finance tools written for freelancers. Every guide is researched from real user reviews, official documentation, and expert sources.